Trading, luxury and short reports

Rheinmetall, Flow Traders, 2CRSi, RELX, HBX Group, Pierre & Vacances, Teleperformance, Siegfried, Brenntag, Eurofins Scientific, Afyren, Brunello Cucinelli, DIA

At Lux Opes, we break down companies into quick takes that get straight to the point - what is happening, why it matters, and what to watch next. We publish 2-4 times per week, depending on the news flow.

For the best reading experience, we recommend reading at Lux Opes

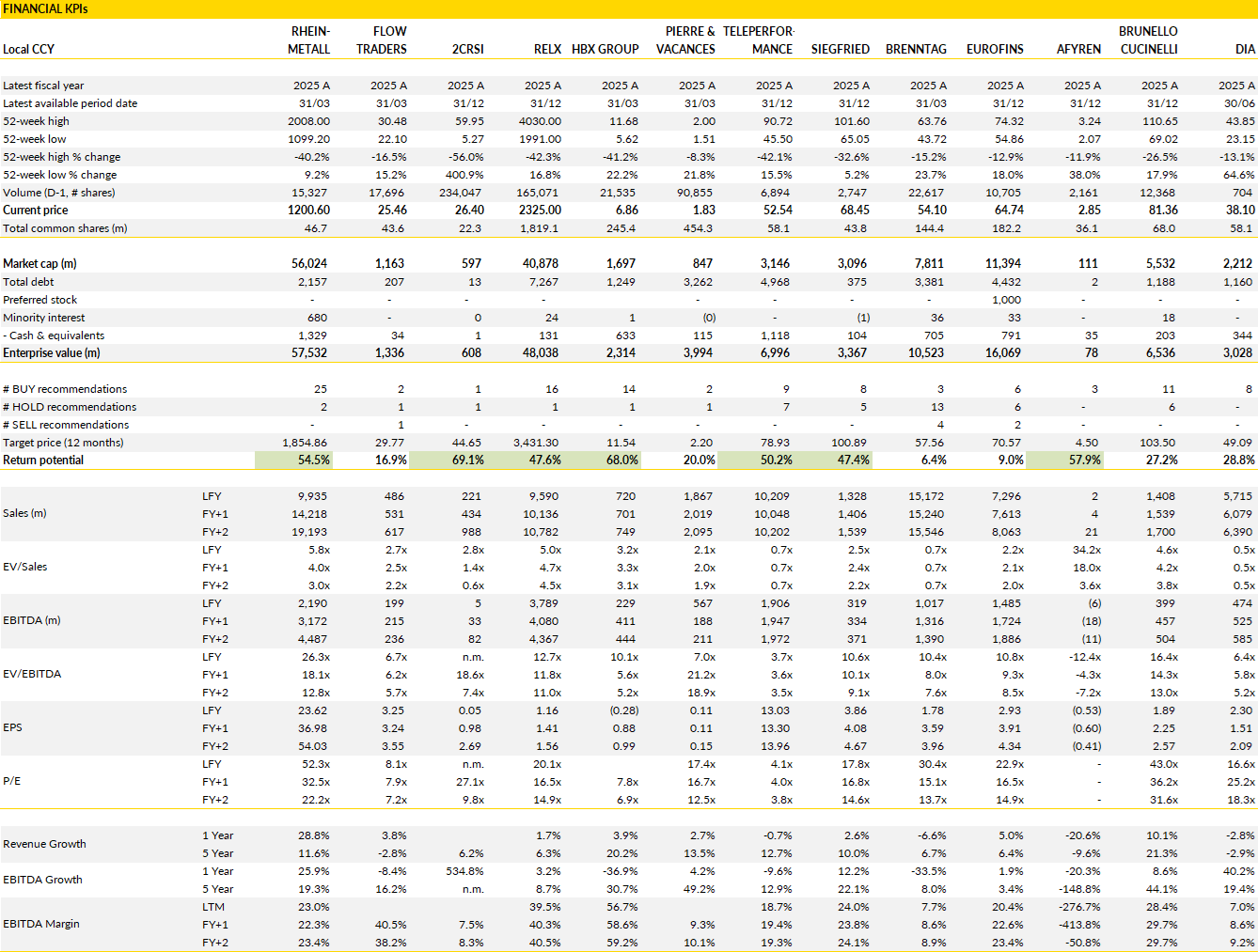

Financial KPIs

Companies covered in this edition: Rheinmetall, Flow Traders, 2CRSi, RELX, HBX Group, Pierre & Vacances, Teleperformance, Siegfried, Brenntag, Eurofins Scientific, Afyren, Brunello Cucinelli, DIA

Rheinmetall (RHM Germany): Execution concerns create an opening

Tough times for Rheinmetall. In just a few months, the discussion moved from whether defence spending will grow towards whether Rheinmetall can execute against the extraordinary demand now sitting in front of it.

Interestingly, the company's growth opportunity has not deteriorated. If anything, European rearmament has accelerated. What changed is investor confidence in the timing of revenue recognition, contract awards and production ramp-ups. The result is a share price that now trades much closer to the broader European defence sector despite earnings growth that remains well above peer levels. Consensus expectations have already come down materially, reducing the hurdle for future results. This reset creates a different setup than existed earlier this year when expectations appeared almost impossible to satisfy.

Near-term trading appears to be moving in the right direction. Management continues to signal confidence in a much stronger second quarter after a relatively slow start to the year. Production bottlenecks that affected several programs have largely been addressed, while delayed deliveries are beginning to convert into revenue.

The bigger issue remains order intake. Several major German defence programmes have taken longer than expected to reach final approval, pushing some anticipated awards into the second half of the year. The timing frustration is understandable, but the underlying contracts have not disappeared. Programs such as F126 and Boxer remain central components of Germany’s long-term defence strategy and would add substantial visibility to Rheinmetall’s already sizeable backlog. The Boxer program is particularly notable given its scale and duration, potentially extending well into the next decade while also carrying meaningful upfront payments that could strengthen cash generation beyond current guidance.

The longer-term opportunity extends beyond traditional land systems. Rheinmetall is gradually assembling a broader defence technology portfolio with a growing presence in missiles, air defence and autonomous systems. Partnerships with international players and recent joint ventures expand the company’s addressable market and reduce dependence on any single platform. Management continues to discuss acquisitions as a core part of its strategy, targeting technologies and capabilities that support its ambition to become a broader defence systems provider rather than simply a manufacturer of vehicles and ammunition. The balance sheet gives the company significant flexibility to pursue that goal.

Investors remain focused on the next contract announcement and the next quarterly result, but the more important question is what Rheinmetall looks like at the end of the decade. If current defence spending plans across Europe translate into sustained procurement activity, the company could emerge with a substantially larger and more diversified earnings base than the one reflected in current sector valuations.

Flow Traders (FLOW Netherlands): A clearer path ahead

Flow Traders investors often had the smae issue: they understood how the company generated money during periods of elevated volatility, but had little visibility into what management was trying to build over the longer term. The capital markets day addressed that issue more directly than previous strategic updates.

For the first time, management provided explicit 2030 financial objectives, including more than €1bn of net trading income, a return on trading capital above 50% and an EBITDA margin above 45%. The profitability targets are not particularly controversial given current performance. Flow already generated approximately 53% return on trading capital and a 45% EBITDA margin during the first quarter of 2026. The more important thing is the attempt to establish a framework that extends beyond short-term market volatility. Historically, the company has often been viewed as a cyclical beneficiary of market dislocations. Management is increasingly presenting Flow as a business capable of generating structural growth through expanding market participation, broader asset coverage and new trading capabilities.

The central challenge remains net trading income growth. Doubling NTI from the €486m generated in 2025 to more than €1bn by 2030 is an ambitious objective for a company whose earnings have historically been driven by external market conditions as much as internal execution. Management's strategy relies on several growth vectors. Digital assets remain a major area of investment, alongside tokenisation initiatives and the continued expansion of quantitative trading capabilities. These activities are intended to diversify revenue streams and reduce dependence on traditional exchange-traded fund market making.

The logic is understandable. Capital markets are becoming increasingly fragmented across asset classes, trading venues and digital infrastructures. Firms with technological expertise and deep liquidity provision capabilities have opportunities to participate in that evolution. The question is whether these opportunities can generate the scale required to materially change Flow's earnings profile. Management has articulated the opportunity more clearly than in the past, but evidence of sustainable revenue growth from these newer activities is still limited. As a result, investor attention is likely to remain focused on execution instead of the attractiveness of the strategy itself.

Capital allocation is of course another important part of the plan. Management continues to emphasise growth in trading capital as a key driver of future earnings capacity. If the company achieves its profitability targets while delivering the planned NTI expansion, the balance sheet will likely need to support a significantly larger trading operation by the end of the decade. Retained earnings will contribute, but additional debt appears increasingly likely as Flow scales its activities.

At the same time, management has acknowledged that 2026 and the first half of 2027 will be investment-heavy periods. Operating expense guidance has increased as the company hires talent and builds infrastructure around quant trading, digital assets and tokenisation. Those investments should weigh on operating leverage before contributing meaningfully to earnings.

The result is a strategy that appears coherent but back-end loaded. Flow has provided a clearer picture of where it wants to be by 2030. The next phase is demonstrating that these newer business lines can move to material contributors to revenue and profitability.

2CRSi (AL2SI France): Credibility becomes the key after the short seller attack

The story at 2CRSi shifted VERY rapidly from servers and AI infrastructure demand to trust.

Following the allegations raised by Grizzly Research, management has aggressively, addressing individual claims through a detailed statement and investor webcast. The company (obviously) rejects the suggestion that revenues were fabricated and points to audited accounts, manufacturing facilities and customer deliveries as evidence supporting its position. Several of the accusations appear to stem from inconsistencies between invoicing locations, delivery destinations and the complexity of the group's international structure. Management also provided additional detail on major contracts, customer relationships and project timelines.

Overall, the company seems to at least have succeeded in presenting counterarguments rather than remaining silent.

This however does not automatically solve the problem. The market's concern extends beyond whether historical revenues existed. Investors are trying to assess the probability that the ambitious US growth story ultimately converts into the numbers management has outlined. The company continues to target more than €400m of revenue for the current year and maintains its ambition of exceeding €1bn in the following year. Those figures depend heavily on the successful execution of large contracts and customer deployments that remain in relatively early stages.

Management acknowledged that several projects are progressing gradually and that ultimate success depends on the financial strength and deployment schedules of end customers. The issue therefore shifts from allegations about past activity to uncertainty regarding future activity. Investors who were already sceptical about the pace and scale of the US expansion are unlikely to become fully convinced after a single webcast.

The next phase will be determined by evidence. Revenue recognition, cash collection and project execution over the coming quarters will matter far more than further rebuttals. The first-half results will likely become the critical checkpoint because they should provide the first meaningful indication of whether the large US contracts are translating into tangible revenue. Until then, the shares may remain highly volatile.

Management has hinted at personal share purchases and has not completely ruled out additional external verification measures, although no formal independent review appears to be planned. The company may ultimately prove that the market reaction was excessive.

The problem is that credibility, once questioned, typically takes much longer to rebuild than it takes to lose.

RELX (REL UK): AI an accelerator (rather than a threat)?

RELX enters the second half of 2026 with stronger operating momentum than many would have expected a year ago when generative AI first emerged as a perceived threat to information providers.

Instead of seeing customers bypass proprietary databases, the company is finding that AI functionality is increasing the value of its content, analytics and workflow products. The legal segment has become the clearest example. Lexis+ AI adoption has been rapid, with more than half of new and renewing U.S. customers now taking the product, helping sustain growth rates that are far above the historical trend. Legal revenue growth spent much of the previous decade running at low single digits, yet the business delivered 9% organic growth last year and appears capable of maintaining elevated levels for several years. The combination of proprietary legal content, embedded workflows and AI-enabled productivity tools gives RELX a strong competitive position at a time when law firms and corporate legal departments are actively seeking efficiency gains. The company’s alliance with Harvey adds another layer to its product ecosystem and expands its reach across AI-driven legal workflows.

Scientific, Technical & Medical is following a similar path. STM represents a larger portion of group revenue than Legal and has historically been a dependable but relatively moderate grower. That profile is changing as customers adopt higher-value analytics products, digital tools and specialised data solutions. Management recently upgraded its qualitative outlook for the division, and market expectations now call for higher organic growth in 2026. New product launches have increased, customer uptake of additional modules continues to rise and demand for specialised analytics remains healthy.

Across the group, these trends support expectations for 6-8% organic revenue growth this year alongside further margin expansion.

RELX's operating model continues to benefit from substantial scale advantages, with more than $2bn invested annually in technology and a workforce that includes over 12,000 technical specialists. Few competitors possess comparable proprietary datasets, engineering resources or customer integration. As AI adoption broadens, those assets appear increasingly valuable rather than less relevant.

The debate around AI has nevertheless weighed heavily on the shares. Despite improving fundamentals, the valuation has compressed significantly over the past year as investors continue to question whether large language models will eventually weaken information providers. Quarterly results have so far suggested the opposite. Revenue growth is accelerating, margins continue to move higher and RELX is extracting additional value from AI-enhanced products through both pricing and customer adoption. Currency movements have obscured part of that strength in reported figures during the first half, particularly given the company's large North American exposure, although that pressure is expected to fade as the year progresses.

Looking ahead to the July interim results, the key issue is whether management can continue demonstrating that AI enhances the economics of the business. Current evidence suggests RELX is successfully moving further up the value chain, transforming raw information into workflow, analytics and decision-support tools that customers increasingly rely upon. That evolution helps explain why growth rates in both Legal and STM are now running materially above their historical averages and why operational performance remains exceptionally strong.

HBX Group (HBX Spain): Easier comparisons ahead (after a pretty tough year)

HBX has spent much of its time dealing with forces largely outside its control.

The company entered the (fiscal) year expecting a more normal travel environment and instead faced geopolitical disruption, higher fuel prices, inflation concerns and changing booking behaviour. The Middle East conflict has been particularly painful because the impact extends beyond the company’s direct exposure in the region. Travellers have become more cautious, booking windows have shortened and competition across distribution channels has intensified. Those pressures have translated into weaker transaction volumes and a sharper decline in take rates than management originally anticipated. Several temporary factors have compounded the problem, including mix shifts towards lower-yield distribution channels and softer non-transactional revenue streams. The result is a year that looks set to fall well short of the ambitions presented around the IPO.

Despite the difficult backdrop, the company continues to invest in expanding content and strengthening relationships with both hotels and distributors. The acquisition of Bridgify fits directly into that strategy by increasing access to hotel inventory and experiences while making the platform more valuable to distribution partners. The competitive environment has become more aggressive, but HBX still appears willing to trade some short-term take rate pressure for market share gains. That approach can be frustrating during weak markets, but it may prove valuable once travel demand normalises. The company continues to believe that long-term take rate erosion should return to the much more moderate levels outlined at the time of listing.

That said, timing is the challenge here. Management expects another difficult quarter, and there is little evidence that growth will suddenly rebound in the immediate future. The more relevant discussion revolves around fiscal 2027. Comparisons become easier, geopolitical headwinds should begin to fade if tensions continue to ease, and some of the one-off factors weighing on profitability start to disappear. Even modest improvements could have a significant impact on sentiment given how depressed expectations have become.

The valuation already reflects considerable scepticism. The shares trade on multiples more commonly associated with structurally challenged businesses despite the fact that the underlying hotel distribution market continues to expand. If revenue growth turns positive again and take-rate pressure moderates toward historical levels, investors may begin to reassess whether the current valuation properly reflects the quality of the platform.

Pierre & Vacances (VAC France): A welcomed binding offer

Pierre & Vacances' strategic review launched in 2025 now appears close to reaching its conclusion with Mubadala Capital proposing to acquire the company through a voluntary takeover offer.

The proposal (€1.90 p/s including a €0.11 special dividend, but with potentially another €0.10 p/s of 80% of shares are pledged) effectively validates the restructuring work completed since the balance sheet crisis. Mubadala is not an opportunistic financial buyer entering an unfamiliar sector. The group has previous investments in leisure and hospitality, including Aman and Looping, and has the financial resources to support longer-term development initiatives.

Management and the board have publicly endorsed the transaction, and support from key shareholders already covers a significant majority of the register. The remaining hurdle is the requirement to secure commitments representing at least 80% of the share capital before mid-July. Based on shareholder indications disclosed by the company, that threshold appears achievable.

The proposed valuation reflects a business that has largely completed its repair phase but has not yet fully demonstrated its long-term earnings potential (meaning, cheap). On an enterprise value basis, the offer implies a multiple below historical sector averages and below levels often associated with high-quality leisure and hospitality assets. That partly reflects the company's history and partly reflects the cyclical nature of the holiday accommodation market. Pierre & Vacances has nevertheless made considerable progress operationally. Booking trends remain encouraging, summer reservations are running ahead of the prior year and management reports increasing levels of last-minute demand. These indicators suggest consumer appetite for leisure travel remains healthy despite a more uncertain economic backdrop across parts of Europe. The company has also benefited from a stronger financial structure, allowing management to focus increasingly on commercial execution instead of balance-sheet repair. For a buyer with a longer investment horizon, there may be opportunities to accelerate development, optimise the portfolio and improve profitability beyond what public markets currently recognise.

The offer creates an interesting situation for minority shareholders. The headline premium to the latest share price appears relatively modest, but the relevant comparison is arguably the valuation before the strategic review process began. Measured against those levels, the premium becomes far more substantial. At the same time, the share price had already incorporated expectations that some form of transaction would emerge, limiting the apparent upside when viewed against recent trading levels.

The key issue is whether another bidder is likely to emerge with a superior proposal. Current information suggests Mubadala has established a strong position, enjoys board support and has already secured backing from major shareholders. Unless a competing bidder appears, the transaction looks like the final stage of a multi-year turnaround.

The company that Mubadala is seeking to acquire is fundamentally different from the one that required rescue financing only a few years ago. Shareholders are therefore being offered a liquidity event at a moment when operational performance has improved materially but before the next phase of growth has fully played out.

Teleperformance (TEP France): No respite, yet.

Téléperformance is in the middle of a(nother) transition year. Revenue trends remain weak, with organic growth declining in the first quarter and management indicating that the second quarter is unlikely to look much better. The more encouraging recent message is that recent contract wins, implementation schedules and market share gains are expected to contribute more meaningfully during the second half. Management continues to guide for 0% to 2% organic growth in 2026, suggesting that conditions have not deteriorated despite ongoing uncertainty across customer service outsourcing markets.

The company has also seen some stabilisation within specialised services after a difficult period that included contract losses and softer demand. The core business remains under pressure, but the gap between current performance and management's medium-term ambitions leaves room for improvement if execution remains solid and recently won business ramps as expected.

But of course the larger issue for Téléperformance is not the next quarter but how artificial intelligence reshapes customer experience outsourcing. Management's position remains that AI represents an opportunity to expand the addressable market rather than a threat to its existence. That argument increasingly centres on the evolution of business process outsourcing from labour-intensive call handling towards more complex customer management, content moderation, trust and safety services, multilingual support and AI-enabled workflows. Scale remains an advantage. Large multinational clients still require global delivery capabilities, regulatory compliance, security standards and operational reliability that are difficult to replicate.

The company also appears willing to reshape its portfolio as industry conditions evolve. Management confirmed that a strategic review remains underway, including potential divestments and acquisitions. By year-end, investors should have greater clarity on which activities are considered core and which assets could be monetised. Given the fragmented nature of the sector and the rapid pace of technological change, portfolio optimisation may ultimately become as important to shareholder returns as organic growth.

Financial flexibility gives Téléperformance options. Free cash flow generation is expected to remain substantial at roughly €800-850m before non-recurring items, while leverage is projected to decline towards approximately 1.2x EBITDA over the coming years. This also creates room for acquisitions, portfolio restructuring or shareholder returns. Management has indicated that proceeds from potential disposals could be returned to shareholders, including through share buybacks. The dividend remains intact, but the bigger attraction may be the company's ability to generate cash while navigating a period of technological disruption.

The market continues to value Téléperformance as though AI will structurally impair the business. Management continues to argue that AI will instead change the mix of services, customer requirements and revenue opportunities. The next six to twelve months should provide a clearer indication of which interpretation is closer to reality.

Siegfried (SFZN Switzerland): Acquisitions are setting up a stronger second half

Siegfried's 2026 is shaping up as a year of two very different halves. The first six months are likely to look underwhelming, with reported sales held back by currency effects and a temporary gap in orders from a major customer. Drug Substances, which remains the largest division, is carrying most of that pressure, while Drug Products continues to deliver healthier growth supported by steady customer demand.

The important point is that management has not changed its outlook despite the softer first-half profile. Growth was always expected to be concentrated in the second half, and that remains the case today. Currency-adjusted revenue growth is still expected to accelerate materially as the year progresses, helped by improving activity levels, contributions from recently acquired assets and the potential for delayed customer orders to return. For a contract development and manufacturing organisation, quarterly timing effects can often create a distorted picture of underlying demand, particularly when a small number of large projects influence reported figures.

The strategic significance of the recent API acquisition is arguably greater than its immediate financial contribution. The addition of Noramco, Purisys and Extractas expands Siegfried's presence across several attractive parts of the pharmaceutical outsourcing value chain. The acquired assets provide manufacturing capacity, development capabilities and specialised purification expertise that complement the company's existing network. Scale remains one of the most valuable assets in pharmaceutical manufacturing, particularly as customers seek partners capable of supporting projects from early development through commercial production. Large pharmaceutical companies continue to rationalise internal manufacturing footprints and rely more heavily on external partners, creating opportunities for established CDMOs with global reach. Siegfried has historically built its business through a combination of operational execution and selective acquisitions, and these latest additions fit that approach. The acquired facilities should contribute meaningfully to revenue growth over the coming years while strengthening the company's position in small-molecule manufacturing, an area that remains highly relevant despite the industry's increasing focus on biologics.

The recent weakness in the share price thus appears disconnected from the operational outlook. Investor concerns have centred on management changes, particularly the CFO transition, alongside concerns that a softer first half could signal broader weakness. Current guidance does not suggest that conclusion. Management continues to target approximately 8% revenue growth at constant exchange rates for 2026 when acquisitions are included, alongside modest margin expansion and earnings growth. The balance between organic growth and acquisition-driven expansion is shifting somewhat this year, but the overall trajectory remains intact.

The enlarged manufacturing footprint gives Siegfried additional opportunities to win new programs and deepen relationships with existing pharmaceutical customers. Margin assumptions may have become slightly more conservative, reflecting integration costs and a prudent stance on profitability, yet earnings expectations continue to move higher as revenue opportunities expand. If the anticipated second-half acceleration materialises, attention is likely to shift away from short-term execution concerns and back towards the company's ability to compound growth through a combination of capacity expansion, customer wins and disciplined acquisitions.

Brenntag (BNR Germany): Earnings power emerges when markets become volatile

Brenntag's preliminary second-quarter update provides a useful reminder of what the company can earn when market conditions become more favourable.

The chemicals distributor delivered operating EBITDA of approximately €450m, comfortably ahead of market expectations and nearly 50% higher than the first quarter. The magnitude of the surprise suggests that pricing and margin dynamics improved much faster than investors anticipated, particularly within the Essentials division where exposure to petrochemicals and industrial chemicals creates significant leverage during periods of supply disruption and market volatility. Management pointed to strong demand and improved margins, although fuller details will not arrive until the August results.

Brenntag's earnings profile remains considerably more sensitive to market conditions than recent trading multiples imply. The first half of 2026 demonstrates that even modest changes in industry conditions can have a meaningful impact on profitability given the scale of the company's distribution network and its central role within global chemical supply chains.

The update also highlights the dual nature of Brenntag's business model. During periods of weak industrial activity, investors tend to focus on volume pressure, cautious customer behaviour and concerns about manufacturing demand. When supply chains tighten and pricing becomes more dynamic, the company's value proposition becomes far more visible. Brenntag sits between producers and end customers across thousands of products and markets, giving it substantial flexibility to manage inventories, pricing and logistics. Recent geopolitical tensions, particularly around energy and petrochemical markets, appear to have contributed to that environment. While some of these factors may moderate if supply routes normalise, the quarter reinforces the importance of scale within chemical distribution.

At the same time, management continues to execute on internal efficiency measures. The company remains on track towards a targeted €150m annualised cost-saving run rate by the end of 2026, with only a fraction of those benefits reflected in reported numbers so far. That leaves an additional earnings lever that is largely independent of market conditions.

Management's decision to raise full-year guidance is significant (op. EBITDA +6% on the mid-point of the new range of €1,250-1,400m (previously €1,150m-1,350m)), although the revised outlook remains conservative. The new range implies a meaningful increase versus prior expectations, yet still assumes a relatively subdued second half despite the strong first-half performance. This caution reflects ongoing concerns around industrial demand and macroeconomic uncertainty, particularly across Europe.

The market has become familiar with that message over the past two years, and current valuation multiples suggest investors are already discounting a challenging environment. What makes the situation interesting is the combination of improving operational execution, visible cost savings and evidence that earnings can rebound sharply when conditions become more supportive. Brenntag is not being valued as a business capable of delivering sustained earnings growth; it is still being valued as a cyclical distributor facing persistent pressure.

The latest quarter demonstrates that this may be more balanced. If industrial demand stabilises and margin conditions remain constructive, the earnings potential embedded within the business appears materially higher than current expectations imply.

Eurofins Scientific (ERF France): Waiting for biopharma

Eurofins enters the second half of 2026 in a familiar position. The company continues to guide confidently for the full year, margins are moving in the right direction and several business lines remain healthy, but the market is still waiting for a more convincing acceleration in organic growth.

Recent trading has arguably been affected by a collection of temporary factors. Weather-related disruptions weighed on parts of the Life business during the first quarter, while Clinical Diagnostics continues to face headwinds in the United States following the suspension of reimbursement discussions for TruGraf testing. The integration of acquired assets has also created some short-term revenue friction in Europe as management optimises the portfolio following the addition of Synlab assets and operations in the Netherlands. None of these issues appear structural, but collectively they have limited top-line momentum at a time when the market was hoping to see a stronger recovery emerge. Management continues to target mid-single-digit organic growth for the year, suggesting confidence that current pressures will ease as 2026 progresses.

The central question remains Biopharma, which has become increasingly important to the long-term growth profile of the group. Management continues to describe commercial activity as encouraging, particularly in central laboratories, and maintains a constructive view on demand trends. The challenge is that a meaningful acceleration has been anticipated for several quarters without yet translating into a decisive improvement in reported growth. Biopharma accounts for more than a quarter of group revenues and has historically been one of the most attractive areas of the portfolio due to its exposure to pharmaceutical research, clinical trials and outsourced laboratory services. The broader outsourcing trend within the pharmaceutical industry remains intact, and there is little indication that Eurofins has lost competitive relevance. Instead, project timing and funding patterns across the sector have created a slower recovery than many expected. If commercial momentum eventually converts into stronger revenue growth, Biopharma could once again become a significant contributor to group expansion. Until that happens, investors are likely to remain cautious despite management's optimistic commentary.

Profitability is providing a degree of support during this period of slower growth. Eurofins continues to expect margin improvement in 2026, building on the 22.5% margin achieved last year. Historically, the company has delivered stronger profitability in the second half, and management expects the same pattern to repeat this year. The operating model benefits from scale, a broad laboratory network and a highly diversified customer base across food testing, environmental services, pharmaceuticals, diagnostics and consumer products. Organic growth may currently sit below the company's long-term historical average of around 6.5%, but margin expansion and cash flow improvement remain important parts of the investment case.

The complication is that Eurofins remains a capital-intensive business. Laboratory expansion, acquisitions, property investments and share repurchases all compete for capital, limiting the pace at which leverage can decline. As a result, the next stage of share price performance will likely depend on whether Biopharma (finally) delivers the growth recovery that management has been discussing for some time.

Afyren (ALAFY France): The technology story is becoming an industrial story

So far, Afyren was primarily viewed (and valued) on the promise that its fermentation technology could produce bio-based acids at commercial scale, with the focus on whether the company could manufacture it reliably and economically. Now is the time to move further.

The NEOXY facility has moved beyond commissioning and is producing commercial volumes, with several hundred tons delivered during the first half of 2026 and revenue already exceeding the whole of 2025. Production capacity has reached roughly 20% of the plant's nameplate capacity of 16,000 tons, providing the first tangible evidence that industrial scaling is progressing. So the next challenge is execution. Management plans additional investments to improve reliability and operational performance, alongside maintenance shutdowns designed to optimise the production process. The objective: move from hundreds of tons today to several thousand tons over the next two years before reaching full utilisation in 2028. The pace of that ramp-up will likely determine the company's value over the remainder of the decade.

Commercially, demand is not the constraint. Every ton produced is currently being sold, approximately fifteen customers are already supplied and the company reports €165m of secured multi-year contracts. That commercial traction provides important validation for both the product and the underlying market opportunity. Customers across food, nutrition, flavours, fragrances and specialty chemicals continue searching for sustainable alternatives to petrochemical-based ingredients, creating a favourable backdrop for bio-based solutions. The recent B Corp certification and additional international approvals further strengthen Afyren's commercial credentials as it expands internationally. The arrival of Kemin Industries as a shareholder may also prove equally important. Beyond providing financial backing, Kemin brings industrial expertise, customer relationships and external validation from a strategic industry participant. For a company moving from pilot scale to industrial manufacturing, that endorsement carries significant weight.

The acquisition of the remaining 49% stake in NEOXY simplifies the equity story considerably. Investors will now see the full economics of the plant flow directly through the group accounts, improving transparency at a critical stage of the ramp-up. The trade-off is that debt previously housed at the project level now sits on the group balance sheet, increasing future financing requirements. This remains one of the central risks.

The company is targeting group breakeven around 2028, but achieving that objective requires continued operational progress and sufficient capital to complete the industrial rollout. Looking beyond the first facility, management continues to discuss a second plant that could be developed either in France or Thailand and potentially enter service around 2030. That decision remains dependent on the success of NEOXY.

For now, the investment case rests on three pillars: demonstrated customer demand, a production ramp that is finally underway and a business structure that has become easier to analyse following full consolidation.

Brunello Cucinelli (BC Italy): Luxury demand remains strong but valuation leaves little room for surprises

Brunello Cucinelli remains one of the few European luxury groups delivering consistent double-digit growth without relying on aggressive pricing or major shifts in product strategy. Demand for ultra-premium apparel remains healthy across most key markets, supporting management's objective of approximately 10% annual growth.

Recent trading suggests little has changed fundamentally. The Americas remain the main growth engine, Europe is benefiting from strong tourism flows and domestic demand, and Asia continues to expand despite a softer contribution from the Middle East. The brand occupies a particularly attractive niche within luxury, serving affluent customers who prioritise craftsmanship, quality and understated positioning over logo-driven consumption. That segment has held up better than many parts of the luxury sector during recent periods of macroeconomic uncertainty. Continued retail expansion also provides a clear pathway for growth, with additional selling space contributing alongside existing store productivity gains.

The geographic mix is evolving somewhat. Growth in Asia and the Middle East is expected to moderate after an exceptionally strong start to the year, partly reflecting the disruption caused by geopolitical tensions in the region. Europe has absorbed some of that demand as international luxury customers shifted spending patterns towards major European shopping destinations. Meanwhile, management continues to report healthy trends in China, Japan and South Korea, although growth rates are becoming more normalised after a particularly strong period.

Retail remains the primary driver of expansion and continues to increase as a percentage of revenue, helping profitability through a more favourable sales mix. That shift is especially important because Brunello Cucinelli's model relies on gradual margin progression instead of large efficiency programs. The company expects another modest improvement in operating margins this year, continuing a pattern that has characterised the business for many years. Growth is therefore being achieved without sacrificing brand positioning, product quality or exclusivity, an important distinction in the luxury industry.

The challenge is that much of this quality is already reflected in the valuation. Brunello trades closer to the highest-quality luxury names than to the broader sector despite operating with lower margins and a more concentrated brand portfolio. Comparisons with Hermès illustrate the issue. Brunello may currently be growing slightly faster, but Hermès retains structural advantages through its superior profitability, lower capital requirements and broader global brand strength.

This does not diminish the quality of Brunello's business. The company continues to gain market share, expand internationally and generate steady margin improvement. However, future returns increasingly depend on continued flawless execution because expectations are already high. The key variables remain retail expansion, sustained demand from high-net-worth consumers and the group's ability to maintain double-digit growth as it becomes larger.

DIA (DIA Spain): Execution is taking over

DIA's investment case has changed substantially in recent years. The company is no longer primarily a restructuring story centred on survival, balance-sheet repair and operational stabilisation. Those issues have largely been addressed. The next chapter is about execution, growth and proving that the business can consistently generate attractive returns from the foundation that has been rebuilt.

The annual meeting reinforced this transition. Governance changes were approved without controversy, leadership continuity remains intact and management reiterated the objectives of the 2025-2029 strategic plan. Spain remains at the centre of everything. DIA is focusing on improving an existing position in neighbourhood grocery retailing. This approach reduces execution risk because it builds upon established customer relationships, a dense store network and a format that is already well understood by consumers. The targets are ambitious but not unrealistic, calling for annual gross sales growth of 4-6%, continued margin expansion and a significant increase in store numbers through the end of the decade.

The strategy itself is relatively straightforward. Management intends to deepen DIA's position in convenience-oriented grocery retailing while expanding the network largely through franchise partners. This model allows the company to grow selling space and market coverage without requiring the same level of capital investment as a wholly owned expansion strategy. At the same time, management is investing in digital capabilities, customer loyalty and data analytics through Club DIA, which has become an increasingly important tool for customer retention and personalisation. These initiatives are particularly relevant in a grocery sector where competition remains intense and differentiation can be difficult. Scale, convenience and customer engagement often determine market share gains.

The combination of franchise-led expansion, increasing sales density and omnichannel development creates several avenues for growth without requiring a fundamental change in the business model. This is one reason why the plan appears credible. DIA is 'just' attempting to improve an operating model that is already producing better results than it did during the restructuring years.

Capital allocation remains disciplined and reflects management's priorities. The company is not yet signalling a near-term return of excess capital to shareholders, which appears sensible given the opportunities available within the business. Cash generation is being directed towards expansion, operational improvements and continued deleveraging. As profitability improves and investment requirements become more predictable, the discussion around dividends and share buybacks is likely to become more relevant.

Management clearly recognises that possibility, although execution remains the immediate priority. The medium-term targets imply a business with higher margins, stronger cash generation and a larger store base than today. If those objectives are achieved, DIA could emerge as a structurally stronger retailer than many investors currently appreciate.