Acquisitions, digital ecosystems and big rerating potential

Prosus, Novem, Abivax, Richemont, Knorr-Bremse, Merck, Burberry, DIA, SPIE, Nagarro, Safran

At Lux Opes, we break down companies into quick takes that get straight to the point - what is happening, why it matters, and what to watch next. We publish 2-3 times per week, depending on the news flow.

For the best reading experience, we recommend reading at Lux Opes

Important note: With the summer holidays coming up, we will take a break for a few weeks as of next week. Lux Opes will return just in time for earnings season.

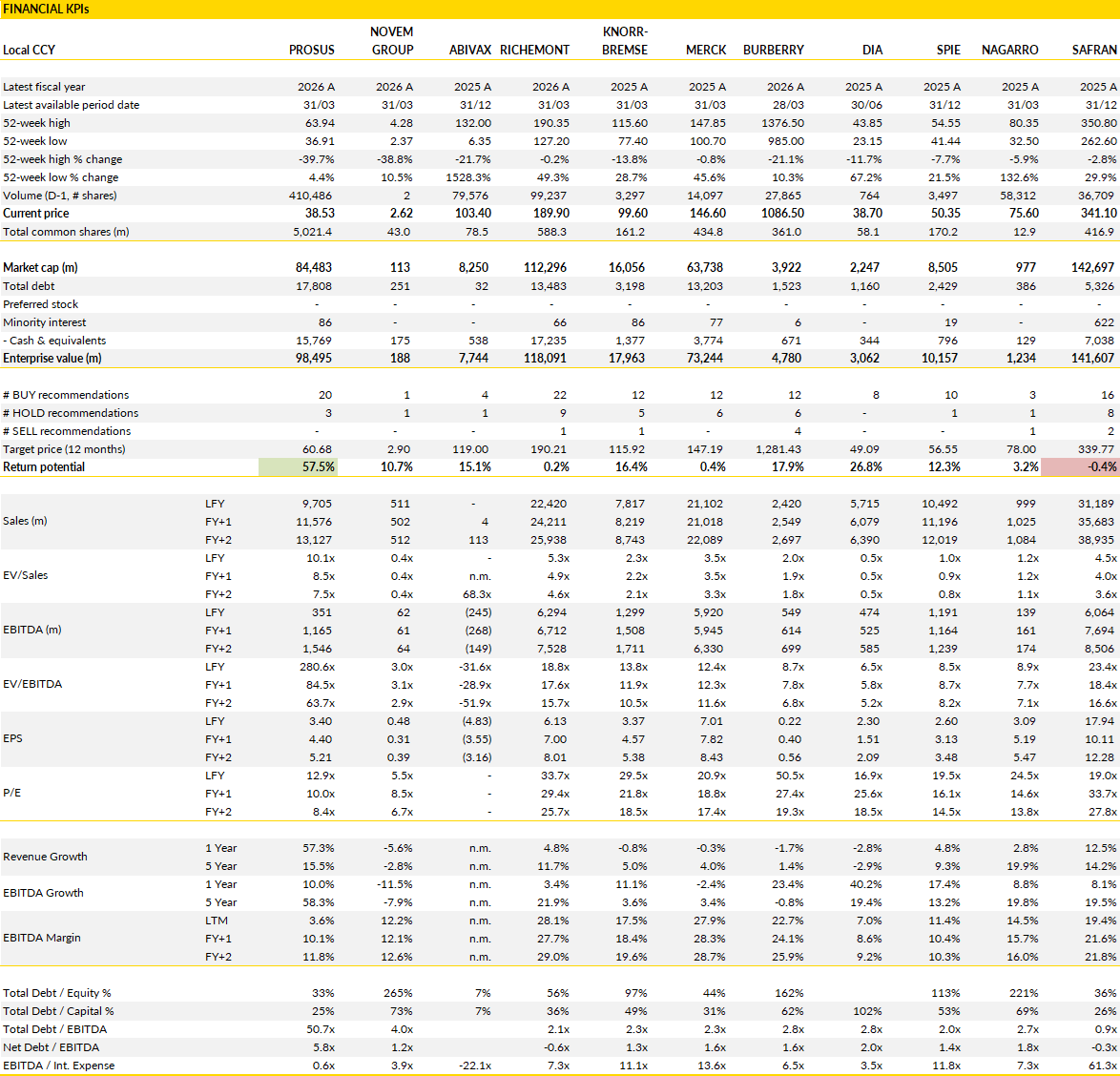

Financial KPIs

Companies covered in this edition: Prosus, Novem, Abivax, Richemont, Knorr-Bremse, Merck, Burberry, DIA, SPIE, Nagarro, Safran

Prosus (PRX Netherlands): Building integrated digital ecosystems while keeping investment firmly on the front foot

Prosus continues to execute the strategy outlined at its Capital Markets Day, prioritising the development of regional digital ecosystems.

The group delivered adjusted EBITDA of $1.27bn for the year ended March 2026, comfortably exceeding its $1.1bn target, helped by the first contributions from Just Eat Takeaway and La Centrale following their consolidation. Operational performance across the existing portfolio also remained encouraging. Food Delivery generated 28% organic growth, comfortably ahead of the previous year's pace, while OLX expanded 16%, supported by continued strength across its classifieds platform. Free cash flow reached $1.51bn, including the $1.24bn Tencent dividend, but the underlying improvement is also noteworthy. Excluding Tencent, management highlighted a $1.4bn improvement in free cash flow over the past three years, illustrating that many of Prosus' e-commerce businesses are steadily becoming self-financing as they mature.

Management remains willing to sacrifice some short-term earnings growth to strengthen long-term competitive positions. Investment will continue across several key assets, particularly iFood and Just Eat Takeaway, where the priority is to restore sustainable revenue growth before focusing on margin optimisation. Competitive intensity remains elevated, especially in Brazil, where Prosus continues investing heavily across grocery delivery, fintech, advertising and adjacent verticals.

At the same time, the group is building increasingly integrated regional ecosystems by combining payments, classifieds, food delivery, travel and financial services around shared technology and customer data. Latin America remains the clearest example of this strategy in action. Non-food delivery businesses there now generate roughly $1.5bn of revenue growing at more than 40%, while cross-selling is becoming increasingly meaningful, with 21% of Despegar's Brazilian revenue already originating from other Prosus businesses. Artificial intelligence also plays a growing role. The company highlighted its proprietary Large Commerce Model, trained on internal commerce data to improve personalisation, marketing efficiency and customer acquisition while lowering AI-related costs across the portfolio.

Capital allocation remains balanced between acquisitions and shareholder returns. Prosus intends to continue monetising part of its 22.66% Tencent stake to finance an enlarged $5bn share buyback program while selectively pursuing acquisitions that strengthen existing regional ecosystems. The group has already completed approximately €2bn of asset disposals during the past year, including the sale of its Meituan investment, creating additional flexibility for future transactions. Large acquisitions in Europe are not currently a priority, with management instead concentrating on integrating recent purchases and returning Just Eat Takeaway to sustainable growth through improved capital allocation, a unified technology platform and more disciplined city-by-city execution.

It's a measured approach reflecting a business that is clearly becoming more operational instead of purely investment-led. While the holding company discount is likely to remain, Prosus is gradually improving the quality of its underlying earnings, generating stronger cash flow and assembling digital ecosystems that could become increasingly difficult for standalone competitors to replicate over the longer term.

Novem (NVM Germany): Cost discipline is helping, but the cycle has yet to turn

Novem's recent results confirmed the preliminary release. The company remains in one of the weakest production environments that the automotive supplier sector has faced in recent years.

Fiscal 2025-26 sales declined 6% to €511 million as vehicle production remained weak across several end markets, while adjusted EBIT fell 35% to €32 million, reducing the operating margin to 6.2%. Even so, the company generated significantly stronger free cash flow, which increased to €48 million from €28 million a year earlier, reflecting tighter working capital management and disciplined capital spending. Net leverage remained stable at 1.8x EBITDA, leaving the balance sheet in a stable position despite the weaker earnings environment.

The immediate challenge is that demand recovery remains difficult to predict. Management has once again avoided formal guidance, preferring to describe market conditions as subdued with only limited visibility on customer production plans. Current company expectations appear modest, with sales likely to remain broadly stable during the new financial year and profitability improving only gradually. This improvement is expected to come primarily from internal measures instead of stronger end-market demand.

Novem continues to focus on areas it can directly influence, including manufacturing efficiency, tighter capital expenditure, lower working capital requirements and ongoing cost reductions. These initiatives should help rebuild margins even if automotive production remains muted. However, the pace of improvement is likely to be gradual. The company's historical earnings profile was built on substantially higher production volumes across the premium automotive market, and a return to double-digit operating margins will require a broader recovery in vehicle output alongside continued operational improvements.

The case remains closely tied to the automotive cycle. Novem continues to occupy attractive positions within premium interior components, supplying high-end vehicle manufacturers where demand tends to recover over time as new model launches gain momentum.

The issue again is timing. There is currently little evidence that production volumes are about to accelerate sufficiently to drive a meaningful rebound in earnings. Until that changes, the focus is on the company's ability to preserve profitability and cash generation through disciplined execution. On that front, management appears to be performing reasonably well. Free cash flow has improved substantially, leverage remains stable and the business continues to generate positive earnings despite difficult conditions.

These reduce downside risk, but they are not enough on their own to support a material re-rating, despite the company trading at an undemanding ~3x EV/EBITDA.

Abivax (ABVX France): Expanding safety data strengthens confidence ahead of the regulatory review

Abivax released additional Phase III maintenance data for obefazimod that further strengthen the overall regulatory package ahead of its planned NDA submission in the fourth quarter of 2026.

The latest data focus on patients with ulcerative colitis who proved most difficult to treat, including those who failed induction therapy and those who initially responded but later relapsed during maintenance treatment. Although these analyses are not part of the primary registration package, they provide valuable evidence that the drug can continue delivering meaningful clinical benefit beyond the initial treatment period. Continued treatment with the 50 mg dose achieved 37.2% clinical remission with patients who did not respond during induction, and 34.5% endoscopic remission after longer therapy periods. A whopping 45.5% regained clinical remission after dose escalation to 50 mg for patients who relapsed during maintenance. These findings suggest that longer treatment duration and dose optimisation may substantially improve outcomes for patients who might otherwise be considered treatment failures.

That said, all eyes here where clearly on safety. Earlier in the program, several cancer cases prompted questions about obefazimod's long-term risk profile, causing what some would define as market panic. The expanded dataset provides considerably more reassurance. The two newly reported non-skin cancers were both assessed by investigators as unrelated to treatment, while the reported malignancies showed no consistent pattern across organs that would suggest a common biological mechanism. Non-melanoma skin cancers also occurred primarily in patients carrying well-recognised risk factors, including advanced age, previous skin cancer and extensive prior immunosuppressive therapy.

Perhaps most reassuring is the growing depth of the safety database itself. Cumulative exposure now exceeds 1,700 patient-years, with exposure-adjusted incidence rates of 0.35 solid tumours and 0.59 non-melanoma skin cancers per 100 patient-years, figures that remain within published reference ranges for patients with ulcerative colitis. Just as importantly, longer follow-up has not revealed any new safety signals, strengthening confidence that the earlier observations do not reflect an emerging treatment-related pattern.

Attention now shifts towards the regulatory review, where both efficacy and long-term safety will receive close scrutiny. The pivotal efficacy results remain among the strongest seen in ulcerative colitis, while the growing body of safety evidence substantially improves the overall balance of benefit and risk. Regulators will undoubtedly continue examining the malignancy data carefully, but the available evidence today is considerably more comprehensive than when the initial maintenance results were released.

For Abivax, this reduces one of the key uncertainties surrounding obefazimod ahead of filing. Beyond the NDA submission later this year, the market will also look towards the Phase IIb Crohn's disease data expected in mid-2027, which could significantly expand the drug's commercial opportunity. That said, given the size of the potential here, we expect the M&A chatter to strongly flare up again.

Richemont (CFR Switzerland): Jewellery leadership continues to support a compelling long-term outlook

Richemont's momentum remains among the strongest in global luxury.

The group's Jewellery Maisons continue to distance themselves from much of the sector, having delivered 16% growth at constant exchange rates in the previous quarter, helping overall group sales increase 13%, while Specialist Watchmakers returned to modest growth of 2%. Management has indicated that trading has remained broadly consistent at the start of the new financial year, suggesting no meaningful slowdown despite a tougher macroeconomic backdrop.

The strength of Cartier and Van Cleef & Arpels continues to sustain the business. Regular collection refreshes, disciplined pricing and exceptionally strong brand positioning have enabled Richemont to keep attracting high-end consumers without relying on aggressive price increases. With the prior-year comparison still relatively favourable after 6% growth in the equivalent quarter last year, the group appears well placed to continue outperforming much of the luxury sector.

External factors have compressed profitability over the past two years despite continued operational strength. EBIT margins have fallen to roughly ~20%, down from the 23-25% levels achieved a few years ago, largely because of higher gold prices, adverse foreign exchange movements and tariff-related pressures instead of deterioration in the underlying business. Those headwinds are beginning to ease. Gold prices have moderated to around $4,000 per ounce, the Swiss franc has stabilised against the euro and management intends to hedge part of its annual gold purchases, improving visibility over future input costs.

At the same time, the increasing contribution from the Jewellery Maisons provides a structural benefit to profitability, with the mix shift adding roughly 10-15bp to margins each year. Combined with continued cost discipline and healthy gross margins, these developments create a path towards a gradual recovery in profitability over the coming years.

The company continues to focus on long-term brand desirability, accepting measured price increases instead of pursuing short-term revenue maximisation. This approach has consistently strengthened the competitive position of its jewellery brands and helped preserve pricing power across cycles. Richemont is becoming increasingly concentrated around businesses with structurally higher margins and more resilient demand characteristics. Jewellery now represents the clear core of the group, reducing dependence on more cyclical product categories.

The shares no longer trade at the discount they once did, reflecting stronger operational execution and growing confidence in the business. Even so, the combination of sustained high-single-digit growth, gradual margin recovery and the exceptional quality of the Jewellery Maisons suggests there is still scope for earnings to compound at an attractive rate over the medium term, particularly as temporary cost headwinds continue to fade.

Knorr-Bremse (KBX Germany): Growth is becoming broader than the traditional rail and truck franchise

Knorr-Bremse is evolving from a cyclical braking systems manufacturer into a broader industrial technology company with multiple structural growth drivers.

While its leadership positions in rail and commercial vehicle braking remain the foundation of the business, a growing share of future earnings is likely to come from adjacent activities that receive far less attention. Businesses such as digital services, energy solutions and signalling already account for ldd% of group revenue, yet they are growing considerably faster than the core operations and benefit from attractive margins. Management has steadily expanded these activities through internal development and targeted acquisitions, creating additional avenues for growth without relying solely on gaining market share in mature braking markets. As these businesses scale, they should represent an increasingly meaningful share of both revenue and profitability, helping diversify the earnings profile while reducing dependence on the traditional truck and rail cycles.

The core business is also entering a more supportive operating environment. Recovery in the North American truck market is expected to provide an additional boost after a softer period, while rail demand remains sustained by long-term investment in transport infrastructure and fleet modernisation. Combined with continued progress under the BOOST efficiency program, this creates potential for further operating leverage over the next several years. Management is expected to provide an update on the program alongside the second-quarter results at the end of July, with the market looking for new medium-term objectives once the current phase concludes.

Margin expansion is likely to remain a central priority as Knorr-Bremse combines productivity initiatives with a gradually improving product mix. The faster-growing adjacent businesses also contribute disproportionately to profitability, meaning their expansion supports earnings growth beyond the contribution from higher sales alone. The combination of operational improvements, stronger end markets and a more favourable mix leaves the company well placed to continue expanding profitability through the cycle.

Market leadership in braking systems continues to provide a stable foundation, while the higher-growth technology businesses create additional upside that is not fully reflected by simply analysing the traditional rail and truck operations. Free cash flow generation remains strong, providing flexibility for continued investment, bolt-on acquisitions and shareholder returns.

The upcoming strategic update should offer greater visibility on how management intends to allocate capital across these different growth opportunities over the remainder of the decade. If the company continues executing successfully, investors may increasingly value Knorr-Bremse as a diversified industrial technology group instead of a conventional transport supplier. That distinction becomes more important as the adjacent businesses contribute a larger share of earnings and help sustain attractive growth even when the underlying truck cycle becomes more volatile.

Merck (MRK Germany): Bio-Techne strengthens the part of the portfolio with the greatest long-term potential

Merck is to acquire US-based Bio-Techne for $73 per share, an enterprise value of $11.3 billion. The acquisition adds a highly complementary portfolio spanning multi-omics technologies, analytical instruments and workflow solutions used throughout the research and drug development process. Bio-Techne is particularly well established in cell therapy, supplying cytokines, growth factors, antibodies and immunoassay products that support research, bioprocessing and advanced therapeutics. Around 81% of revenue comes from consumables, giving the business an attractive recurring revenue profile.

The transaction also provides Merck with a 19.9% stake in Wilson Wolf, a leading manufacturer of cell culture technologies, alongside an option to acquire the remaining ownership after fiscal 2027 under pre-agreed terms. This creates an additional avenue for expansion in one of the fastest-growing areas of advanced therapeutics. Management has long viewed Life Science as the division with the greatest structural growth opportunities, but the portfolio lacked sufficient exposure to several higher-growth research and consumables markets. Bio-Techne addresses that gap directly. The businesses are highly complementary, combining Merck's global commercial reach with Bio-Techne's specialised product portfolio and scientific expertise. At the same time, management expects meaningful cost synergies over the first three years following completion while also benefiting from stronger cash conversion than the existing Life Science business.

The acquisition also reflects a broader evolution within Merck's business mix. The company has increasingly concentrated investment around businesses with stronger structural growth characteristics and higher recurring revenue. Bio-Techne accelerates that process by increasing exposure to research consumables and laboratory workflows that typically remain resilient across economic cycles.

Although the purchase price might appear demanding (~23x EV/EBITDA), the valuation becomes considerably more attractive after synergies (roughly 17.5x EV/EBITDA) and reflects the premium generally attached to high-quality life science assets.

More importantly, the transaction addresses an area where management previously faced a strategic disadvantage relative to several competitors. Strengthening the Life Science division should leave Merck better positioned to participate in long-term trends across biologics, cell and gene therapy, diagnostics and laboratory automation. As the second-largest acquisition in the company's history, Bio-Techne represents a significant commitment, but it also demonstrates management's willingness to deploy capital behind businesses capable of generating durable growth for many years. Combined with Merck's existing Healthcare and Electronics operations, the enlarged Life Science platform further strengthens the company's position as one of Europe's most diversified science and technology groups.

Burberry (BRBY UK): Early progress is encouraging, but rebuilding margins will take considerably longer

Burberry has made meaningful progress stabilising the business, but the next phase of the turnaround is likely to prove more demanding than the initial recovery.

Recent trading suggests the brand has regained momentum across several key markets, with the United States and Greater China continuing to perform well and core product categories attracting renewed customer interest. The improvement follows a period in which management refocused the assortment around Burberry's most recognisable products while simplifying the brand message and strengthening retail execution. These initiatives should have helped return the business to positive comparable sales growth, and current trading suggests that first-quarter performance has remained broadly consistent with the previous quarter. The issue is no longer whether Burberry can stabilise revenue. Sustaining growth beyond the initial rebound will require broader product success, higher average transaction values and continued improvement in customer mix, all of which remain less certain.

Regional trends illustrate both the strengths and limitations of the current recovery. The United States continues to benefit from solid domestic demand, while Greater China has recovered alongside improving consumer activity. Europe remains more mixed, reflecting its significant dependence on international tourism, although trading conditions appear to have improved modestly following a difficult period. Elsewhere in Asia, performance remains uneven, with South Korea continuing to outperform while Japan has weakened after several exceptionally strong quarters.

Taken together, these trends suggest that Burberry's recovery remains heavily influenced by regional factors instead of broad-based acceleration across the entire business. Management also continues to invest aggressively in marketing and brand development to reinforce the repositioning. Those investments are essential if Burberry is to strengthen its long-term competitive position, but they also of course limit the pace at which profitability can recover. Higher sales alone are therefore yet unlikely to translate immediately into substantially higher operating margins.

The margin outlook remains the principal question facing the investment case. Gross margins should gradually improve as inventory normalises and exceptional write-downs disappear, allowing the business to return to a more typical seasonal pattern during the second half of the year. Even so, the combination of ongoing marketing investment, product development and brand-building expenditure is likely to keep operating leverage relatively modest.

Management appears capable of rebuilding profitability into double-digit territory over time, but consistently achieving margins well above that level may prove significantly more challenging. The luxury sector has become increasingly competitive, with leading brands continuing to invest heavily in craftsmanship, retail experiences and product innovation. Burberry is rebuilding from a weaker position and therefore needs to continue investing simply to regain lost ground.

The turnaround remains credible, and the operational improvements achieved over the past year should not be overlooked. At the current valuation, however, much of the near-term recovery already appears reflected in the shares, while the more difficult task of restoring premium profitability still lies ahead.

DIA (DIA Spain): The turnaround enters its next phase

DIA's first-half results are likely to show that the company's recovery is becoming increasingly operational (instead of financial).

Spain continues to drive virtually all of the group's progress, with strong customer demand, expanding store capacity and improving profitability combining to create a business that now looks fundamentally different from the one that entered its restructuring several years ago. Gross sales under banner in Spain are expected to increase at a hsd% during the second quarter, supported by approximately 5-7% like-for-like growth and a further contribution from network expansion. New store openings remain an important part of the strategy, allowing DIA to increase its presence while maintaining its focus on neighbourhood convenience. Argentina continues to weigh on reported figures, although the pace of decline is moderating, making it progressively less of a drag on overall group performance.

Profitability continues to benefit from higher sales density, better operating leverage and disciplined cost control, with Spain expected to generate virtually all of the group's earnings. Adjusted EBITDA for the first half is expected to increase at mid-teens %, lifting the adjusted EBITDA margin to over 5%. Argentina is still expected to report a small operating loss, although the business continues to move closer to breakeven compared with last year. More importantly, the wider business is beginning to demonstrate that growth and profitability can improve simultaneously. Capital continues to be directed towards expanding the Spanish network, strengthening omnichannel capabilities and increasing customer engagement through Club DIA instead of prioritising shareholder distributions. That approach reflects management's confidence that reinvestment currently offers the highest long-term returns as the business scales.

Attention is therefore shifting away from restructuring milestones towards execution of the longer-term growth strategy. Management is expected to reaffirm its 2025-2029 objectives, including annual Spain sales growth of 4-6%, an adjusted EBITDA margin of 7.5-8%, more than 300 additional stores by 2029 and annual investment of €150-180m in the Spanish business, although spending during 2026 could exceed €200m as expansion accelerates.

The recent annual meeting also confirmed governance changes designed to support this next stage of development. While capital returns remain a longer-term objective, management continues to prioritise self-funded growth and further deleveraging before considering dividends or buybacks. That seems appropriate given the opportunities still available within Spain.

If current trends continue, DIA will increasingly be valued on its ability to deliver sustained earnings growth from a much stronger operating platform instead of simply completing its turnaround, which would also warrant a multiple rerating.

SPIE (SPIE France): Consistent execution continues to compound through steady operational improvements

SPIE enters the first-half reporting season with little sign that its long-term growth profile has changed despite a more uncertain macroeconomic backdrop.

After weather-related disruption temporarily affected activity during the first quarter, the second quarter is expected to show a clear recovery, allowing organic growth to return to around 3%. This improvement is largely driven by delayed high-voltage projects coming back into execution instead of a sudden change in demand.

The group's diversified exposure across electrical engineering, industrial services and energy infrastructure continues to provide resilience, with Germany expected to remain the strongest contributor to growth while Central Europe also continues to perform well. France remains more subdued as weaker building-related activity and slower fibre deployment offset healthier trends elsewhere in the portfolio. Even so, SPIE continues to benefit from structural investment themes that remain largely independent of short-term economic fluctuations, including grid modernisation, electrification, industrial efficiency and the broader energy transition.

Operating margins are expected to edge higher again during the first half despite ongoing geopolitical disruption and mixed regional demand. This reflects disciplined project selection, effective cost control and the continued contribution from acquisitions completed over recent years. SPIE has built a strong track record of integrating smaller businesses that expand geographical coverage or technical expertise without materially increasing operational complexity. The recent additions of ROFA and SGS should continue this pattern once fully reflected in reported numbers. Importantly, the company's acquisition strategy remains highly selective, focusing on fragmented markets where bolt-on transactions can create operational efficiencies and strengthen local market positions. This disciplined approach has allowed SPIE to combine steady organic growth with value-accretive external expansion over a prolonged period. As a result, profitability continues to improve gradually instead of depending on large cyclical swings in activity.

The balance sheet remains supportive of this strategy. While leverage has increased following recent acquisitions, management expects debt metrics to improve naturally through cash generation during the second half as seasonal working capital outflows reverse. That leaves the company with sufficient flexibility to continue pursuing acquisitions while maintaining a conservative financial profile.

The broader investment case also remains attractive because many of SPIE's end markets continue to enjoy favourable structural demand. Electrification, energy efficiency, industrial automation and infrastructure modernisation are all likely to require sustained investment over many years. Unlike equipment manufacturers, SPIE generates much of its revenue from engineering, installation and maintenance services, creating recurring customer relationships and reducing dependence on individual investment cycles.

The shares therefore offer exposure to long-term infrastructure spending through a business model that has consistently demonstrated operational discipline and resilient cash generation. While headline growth may fluctuate from quarter to quarter due to weather or project timing, the underlying trajectory continues to point towards gradual earnings expansion supported by both organic execution and carefully targeted acquisitions. This all (still) on the back of a decent valuation.

Nagarro (NA9 Germany): A takeover that recognises value the market never fully appreciated

Persistent Systems' proposed acquisition of Nagarro represents one of the largest takeover premiums seen in the European IT services sector in recent years.

The €81 per share all-cash offer values the company at roughly double its previous trading level (~10x EV/EBITDA). The bid already benefits from several factors that materially improve its credibility. Persistent has secured the support of Nagarro's largest shareholder, representing around one-fifth of the share capital, while management has also indicated its intention to tender its own holdings. Both the Management and Supervisory Boards have expressed support for the transaction, subject to reviewing the final offer documentation. Although regulatory approvals and the minimum acceptance threshold still need to be satisfied, the proposed acquisition enters the process with strong backing.

Strategically, the industrial logic is compelling. Persistent has steadily expanded its position in digital engineering, cloud services and artificial intelligence, particularly across North America, while Nagarro has built a complementary franchise with a stronger presence in Europe and recognised expertise in enterprise software, customer experience and digital transformation. Combining the two businesses creates a global technology services platform with annual revenue approaching $3bn, more than 46,000 employees and operations spanning over 40 countries.

Scale has become increasingly important within IT services as customers seek partners capable of supporting large multinational digital transformation programmes while also investing heavily in artificial intelligence capabilities. The combined business would possess a broader customer base, deeper engineering resources and stronger relationships with leading software vendors and cloud providers. For Persistent, the acquisition significantly strengthens its European presence. For Nagarro, it provides access to greater financial resources and a larger global delivery platform at a time when competition within digital engineering continues to intensify.

For (minority) shareholders, the practical decision is relatively straightforward. The offer represents an exceptionally large premium to both the undisturbed share price and recent trading averages while valuing Nagarro at a multiple broadly consistent with comparable strategic acquisitions in the sector. Although investors can always speculate about the possibility of a competing bid, that outcome appears relatively unlikely given the current valuation environment for European IT services businesses and the strong level of support already secured by Persistent.

The acquisition recognises strategic value that the public market had been reluctant to assign to the business. While Nagarro arguably possessed greater long-term potential than its previous valuation suggested, the proposed consideration crystallises that value today with a high degree of certainty. Unless another bidder unexpectedly emerges, the transaction offers shareholders an opportunity to realise a price that would likely have taken many years to achieve through standalone execution alone.

The deal is expected to close late this year to early next year, a.o. conditional of reacing a 50% + 1 share acceptance level.

Safran (SAF France): Exail expands strategic capabilities

Safran's proposed acquisition of Exail (confirmed at €128.5 per share) would broaden Safran's capabilities in inertial navigation, particularly within naval and maritime applications, while also adding exposure to defence technologies that continue to benefit from rising global security spending.

The proposed structure appears well advanced. Safran has entered exclusive negotiations with the Gorgé family, which controls more than 40% of Exail, making a successful transaction highgly likely. That said, the possibility of a competing offer cannot be dismissed entirely. Exail possesses several strategic assets that could also appeal to defence groups such as Thales or Naval Group, both of which already have meaningful activities in adjacent markets. Even so, any rival bidder would likely need to offer a materially higher valuation given Safran's apparent agreement with the controlling shareholder and the advanced stage of negotiations.

From an industrial perspective, the strongest logic lies within inertial navigation systems. Exail has developed recognised expertise in fibre-optic gyroscope technology and maritime navigation systems, areas that complement Safran's existing portfolio without creating significant overlap. The acquisition would strengthen Safran's position in naval applications, where it has historically maintained a relatively focused presence compared with its leadership in aerospace. Beyond navigation, Exail also contributes businesses in maritime drones and naval robotics, although these appear less directly aligned with Safran's traditional operating model. Safran has generally concentrated on supplying critical systems instead of complete platforms, making the strategic fit somewhat less obvious in these activities. While the company could improve procurement, industrial efficiency and international commercial reach, these businesses remain comparatively niche and are likely to face increasing competition as autonomous maritime technologies mature.

On conventional financial measures, the acquisition appears expensive (~26x EV/EBIT over 2027 estimates). Expected returns remain relatively modest in the near term, reflecting the premium required to acquire a high-quality defence technology asset and the limited scope for immediate synergies. But the economics become more attractive over a longer time horizon as Exail continues to grow and integration benefits gradually emerge, so investors are effectively paying today for value creation that may only become visible several years from now.

That does not necessarily make the acquisition unattractive. Defence technology assets with differentiated intellectual property have become increasingly scarce, and strategic positioning often commands a premium. Nevertheless, this is a long-term portfolio investment instead of a transaction capable of transforming Safran's earnings profile. The company's broader investment case continues to rest primarily on its leadership in aircraft propulsion, aftermarket services and aerospace equipment. Exail strengthens selected defence capabilities and expands exposure to attractive technologies, but the acquisition alone is unlikely to become a defining driver of earnings over the medium term.