Copper, shoes and turnarounds

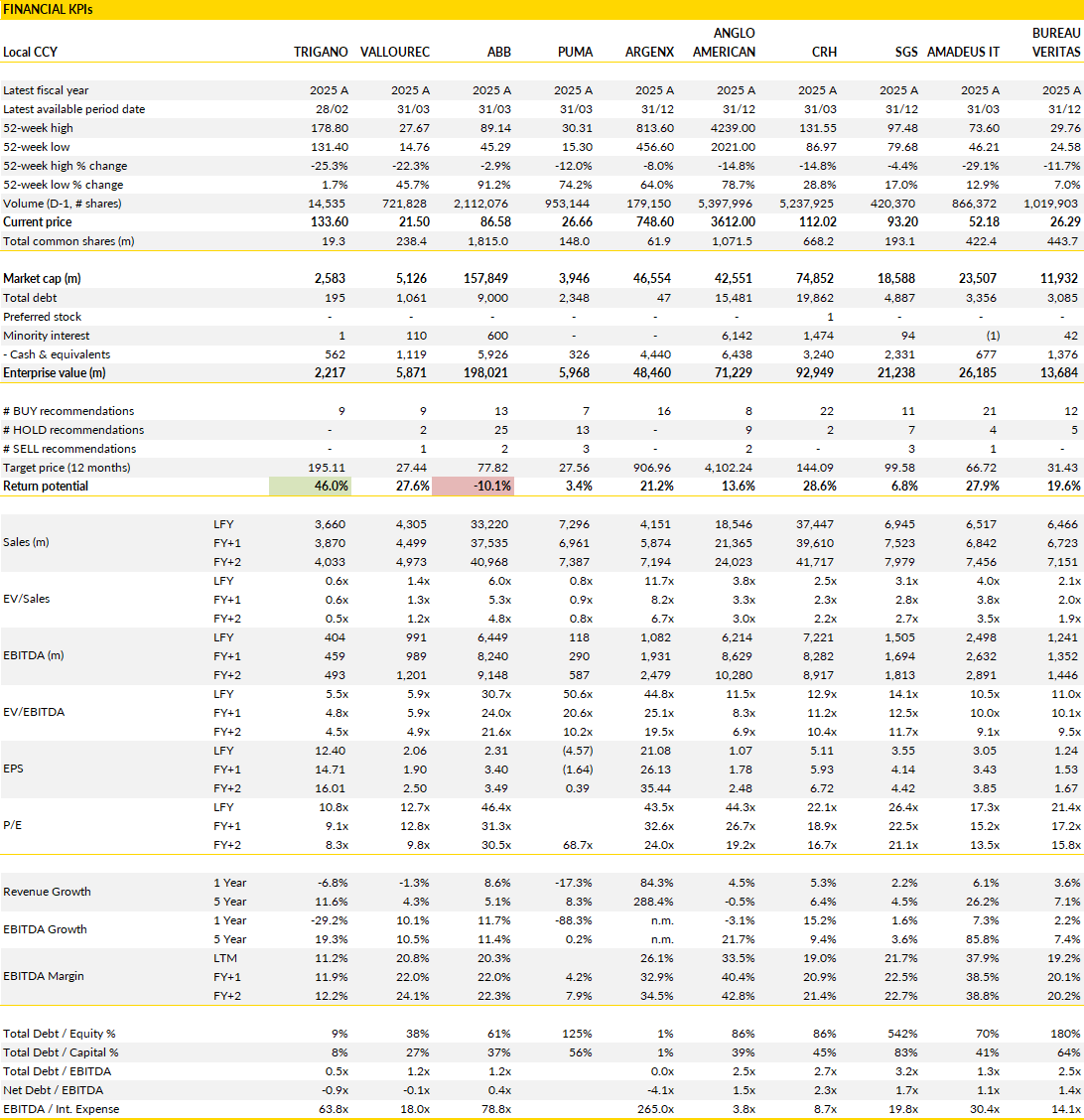

Trigano, Vallourec, ABB, Puma, argenx, Anglo American, CRH, SGS, Amadeus IT, Bureau Veritas

At Lux Opes, we break down companies into quick takes that get straight to the point - what is happening, why it matters, and what to watch next. We publish 2-4 times per week, depending on the news flow.

For the best reading experience, we recommend reading at Lux Opes

Financial KPIs

Companies covered in this edition: Trigano, Vallourec, ABB, Puma, Argenx, Anglo American, CRH, SGS, Amadeus IT, Bureau Veritas

Trigano (TRI France): Supply chain issues are masking a healthier demand environment

Trigano's third-quarter results are softer than expected, but the underlying picture remains quite encouraging.

Revenue growth slowed sharply from the first half (+1.6% yoy in Q3), primarily because production bottlenecks prevented completed motorhomes from reaching customers on schedule. Manufacturing volumes continued to increase, yet around 1,000 vehicles left production without all the necessary components, delaying deliveries and pushing revenue recognition into future periods. This timing issue weighed on reported sales but without indicating weaker underlying demand. Motorhomes and caravans remain the group's largest business and therefore had the greatest influence on quarterly performance. Distribution volumes also softened modestly as showroom traffic eased during April and May, although the decline remained limited given the broader consumer backdrop. Outside the core recreational vehicle activities, the rest of the portfolio continued to perform steadily, helping offset part of the temporary disruption affecting vehicle deliveries.

An important message from management's outlook for the coming selling season: retailers responded positively to the presentation of the new product range, with order volumes reported to be broadly in line with last year despite a more cautious consumer environment across Europe. This provides useful reassurance that demand for leisure vehicles remains fundamentally healthy after several years of exceptional volatility. Pricing also remains disciplined, with only modest increases planned for the next model year, suggesting management sees little need to stimulate demand through aggressive discounting. Dealer inventory levels have become much healthier following the post-pandemic normalisation period, reducing one of the principal risks that weighed on the industry over the past two years.

As a result, Trigano enters the new season with a cleaner distribution channel and a product portfolio that appears to be well received by retailers. Assuming component availability improves, the delayed vehicles should gradually be delivered during the fourth quarter, allowing part of the temporary revenue shortfall to reverse naturally.

Overall, the business continues to strengthen despite these short-term disruptions. Management still expects operating margins to improve meaningfully this year as production efficiency recovers and pricing remains supportive. At the same time, the balance sheet continues to provide considerable financial flexibility. Net cash is expected to exceed €500m even after ongoing share repurchases, giving the company ample capacity to continue investing in production, pursue acquisitions or return additional capital to shareholders when appropriate.

The market nevertheless continues to value the company as though demand has entered a prolonged downturn. Current trading suggests a more balanced view. Retail demand appears stable, dealer inventories have normalised and the latest production disruption looks operational and not structural. If supply chain constraints ease over the coming months, the market may begin focusing again on the company's strong cash generation, improving profitability and leading position within a market that continues to benefit from long-term interest in outdoor leisure and motorhome travel.

Vallourec (VK France): Geothermal energy the next growth driver?

Many have viewed Vallourec's transformation over the past few years mostly through the lens of capital discipline, operational restructuring and exposure to the oil and gas cycle. This remains an important part of the story, but management is building a second growth platform around geothermal energy.

The opportunity remains small in current financial terms, but it aligns closely with the company's broader "Value over Volumes" strategy. Geothermal wells operate in extremely demanding environments, requiring premium tubular products capable of withstanding high temperatures, pressure variations and decades of continuous operation. These technical requirements play into Vallourec's strengths, creating barriers to entry that are difficult to replicate and allowing Vallourec to compete on quality instead of price. A company that has deliberately shifted its focus towards higher-value applications, geothermal energy seems a natural extension of the existing business.

The timing of the opportunity is linked to a broader shift in global electricity demand. Growth in electrification, industrial decarbonisation and of course artificial intelligence infrastructure is increasing the need for reliable baseload power generation. Geothermal energy offers several characteristics that make it attractive in this environment. Unlike solar and wind, production is not dependent on weather conditions, and recent improvements in drilling technology have significantly reduced project costs. As drilling becomes faster and more efficient, the economics of geothermal projects continue to improve.

Vallourec estimates its addressable market across North America, Europe and Southeast Asia could reach approximately 400,000 tonnes by the end of the decade. Even under relatively conservative market share assumptions, this would create a meaningful business. More optimistic scenarios suggest geothermal energy could contribute close to 15-20% of Tubes EBITDA by 2030. This would make geothermal one of the company's most important growth initiatives outside traditional oil and gas markets. Importantly, management believes existing industrial capacity is largely sufficient to support this expansion, limiting the need for major capital investments.

Vallourec remains closely associated with upstream energy spending, which often leads investors to value the company primarily through the lens of oil and gas cycles. A successful geothermal business could gradually change that perception. Exposure to energy security, electrification and low-carbon infrastructure broadens the potential shareholder base and reduces dependence on conventional hydrocarbon investment trends.

The market is not yet assigning much value to this possibility because commercial adoption remains at an early stage and visibility beyond a few years remains limited. That caution is understandable. Geothermal energy is still emerging as a large-scale industrial market.

Nevertheless, the ingredients for meaningful growth appear to be there. Rising electricity demand, improving project economics and Vallourec's technical positioning create a combination that could become increasingly valuable over time. If geothermal deployment accelerates as expected, the company may ultimately be viewed as more than a premium supplier to the oil and gas industry. And this will be reflected in the valuation.

ABB (ABBN Switzerland): Exceptional execution, but expectations have caught up

ABB continues to benefit from the strong operating environment in global industrial technology. And the second quarter appears set to extend the trends visible at the start of the year, with robust order intake, double-digit revenue growth and another step higher in profitability.

Electrification remains the primary engine, supported by sustained investment in data centres, grid expansion and power infrastructure. Demand across these markets continues to exceed expectations, creating a favourable backdrop for businesses supplying electrical equipment, protection systems and automation technologies. Automation is also performing well, particularly in marine and ports, while Motion continues to deliver consistent profitability despite a more mature cycle. The only area still recovering gradually is Discrete Automation, where industrial demand remains uneven. Even so, the division appears to be moving in the right direction after an extended period of weakness.

The strength of the current cycle reflects more than favourable end markets. Over the past several years, ABB has reshaped its portfolio, simplified its organisation and improved operational discipline. Those efforts are now translating into consistently high margins across most business lines. Electrification continues to set the pace, benefiting from a mix of pricing, volume growth and favourable product mix. Motion remains a highly profitable franchise with stable demand across industrial applications, while Automation is benefiting from stronger project execution and improving order quality. Even the e-mobility business, which continues to generate losses, has become less significant within the overall earnings profile.

Management also appears confident enough to maintain the more ambitious financial objectives introduced earlier this year. The company continues to target revenue growth in the high single-digit to low double-digit range, a book-to-bill ratio above one and further margin expansion during 2026. This suggests management sees little evidence that demand is weakening across its core markets despite a more uncertain macroeconomic backdrop.

Operationally, ABB has delivered almost everything investors could have hoped for. Revenue growth remains strong, margins continue to improve and several structural growth drivers, including electrification, automation and grid modernisation, still have many years to run.

The difficulty is that the share price now reflects much of this success. ABB trades at a substantial premium to its own historical valuation after a period of sustained earnings upgrades and strong share price performance. That premium is easier to justify than it would have been several years ago because the quality of the business has improved materially. Nevertheless, future returns are likely to depend more heavily on continued earnings growth than on further expansion in valuation multiples.

The medium-term outlook remains attractive, particularly if investment in electrical infrastructure and data centres continues at its current pace. At current levels, however, investors appear to be paying for that strength well in advance.

Puma (PUM Germany): The reset is continuing, but the turnaround remains elusive

Puma's problems are no longer a mystery. The company spent the past year shrinking parts of the business that were generating volume but damaging brand equity, particularly within wholesale channels and discount-driven distribution. This is now visible in the numbers.

Second-quarter sales are expected to decline sharply, with revenue potentially falling around 10% on a currency-neutral basis and reported sales down even further due to foreign exchange headwinds. This represents a clear deterioration from the first quarter and highlights that the clean-up process is not yet complete. Wholesale reductions, tighter inventory management and a greater emphasis on full-price direct-to-consumer sales continue to weigh on revenue growth.

At the same time, the benefits of inventory clearance are fading as the company moves beyond the most aggressive phase of stock reduction. Management appears willing to accept weaker near-term revenue in exchange for rebuilding pricing discipline and improving the long-term health of the brand. The challenge is that investors have yet to see convincing evidence that these sacrifices will ultimately produce stronger growth.

The regional picture reflects the uneven nature of the transition. Europe and the Americas are expected to remain under pressure as reset measures continue to affect distribution and consumer demand softens. Asia looks more constructive, partly because the region has been less affected by the restructuring actions underway elsewhere. Product momentum remains mixed, and Puma still faces intense competition from larger global peers that continue to invest heavily in innovation, marketing and athlete endorsements.

The company is trying to improve brand positioning without losing relevance in key performance and lifestyle categories. That is a delicate balancing act. Reducing lower-quality revenue streams can improve profitability and strengthen the brand over time, but only if consumers respond positively to the refreshed product offering and premium positioning. For now, management is still asking investors to focus on future benefits instead of current sales trends. The absence of a clear acceleration in underlying demand suggests that the transformation remains a headwind in itself.

There are nevertheless some encouraging signs below the headline revenue decline. Gross margins are expected to improve materially as promotional activity decreases and sales shift towards higher-quality channels. Operating expenses are also moving lower, helping reduce losses despite the significant top-line pressure. These improvements demonstrate that management's strategy is having some of its intended effects.

A reminder that comparisons become considerably easier during the second half because the prior year included severe inventory-clearing activity and substantial sales declines. This creates the possibility that reported growth could return later in 2026.

The more important issue, however, is whether the underlying business genuinely improves. A return to positive reported growth driven by easier comparisons would not, on its own, confirm that the turnaround is succeeding. Puma still needs to demonstrate that it can rebuild demand, gain market share in key categories and generate sustainable earnings growth without relying on discounting.

The company has clearly moved beyond crisis management, but it has not yet reached the stage where a durable recovery can be taken for granted.

Argenx (ARGX Belgium): Myositis could become the next major chapter for Vyvgart

Argenx has already established Vyvgart as one of the most successful launches in neuromuscular disease, but the next phase of growth depends on expanding beyond its initial indications.

Myositis is emerging as one of the most important opportunities in that effort. With phase III data expected during the third quarter, management has spent considerable time outlining why it believes the program has a high probability of success. The phase II results were compelling, showing meaningful improvements across multiple clinical measures, including muscle strength, physical function and overall disease activity. Equally important was the speed of response. Patients treated with Vyvgart achieved clinically meaningful improvements much faster than those receiving placebo, a characteristic that could become highly valuable in clinical practice. Biomarker data also supported the observed outcomes, with reductions in pathogenic antibodies and disease-related inflammatory signals occurring alongside clinical improvement. Taken together, the data provide a coherent picture that links biological mechanism, biomarker changes and patient outcomes.

One of the more interesting developments is the increasing distinction management is drawing between different myositis subtypes. Instead of treating the indication as a single commercial opportunity, argenx is highlighting immuno-mediated necrotising myopathy and dermatomyositis as potentially separate regulatory and commercial pathways. This reflects what was observed in earlier studies, where the strongest efficacy signal appeared in IMNM while dermatomyositis also produced encouraging results. From a regulatory perspective, this could create greater flexibility. Strong results in one subgroup would not necessarily depend on equally strong outcomes across the entire myositis population. Commercially, both opportunities are meaningful. IMNM alone represents a patient population with substantial unmet need and no approved therapies, while dermatomyositis offers a larger market with significant room for innovation beyond current treatment approaches. The long-term extension data presented recently provide additional support for the program, demonstrating durable responses over extended treatment periods and continued benefit in patients switching from placebo. In a chronic disease setting, durability may ultimately prove just as important as initial efficacy.

The significance extends beyond the immediate revenue opportunity. Management increasingly describes myositis as an entry point into broader rheumatology markets and a key component of its Vision 2030 strategy. Vyvgart already benefits from an established commercial infrastructure, physician relationships and reimbursement experience built through its neuromuscular indications. That foundation should lower the barriers to expansion into adjacent autoimmune diseases. The commercial potential of myositis alone appears substantial, particularly given the lack of effective long-term treatment options and the growing body of evidence supporting FcRn inhibition.

Yet the broader investment case increasingly rests on the depth of the pipeline. Empasiprubart and adimanebart represent additional late-stage opportunities that could further diversify the company's growth profile over the coming years. After the strong share price performance of the past year, expectations are undoubtedly higher. Even so, upcoming phase III readouts have the potential to further strengthen the argument that argenx is evolving from a successful single-product company into a broader immunology platform with multiple avenues for long-term expansion.

Anglo American (AAL UK): Keep an eye on copper

Following a series of disposals and portfolio changes, copper is increasingly emerging as the group's defining business, accounting for roughly three quarters of underlying EBITDA. But the recent weakness in the share price does little to reflect that shift. The decline has largely mirrored broader mining sector sentiment instead of company-specific deterioration, despite copper remaining one of the strongest-performing major commodities. Structural demand continues to be supported by electrification, grid investment, renewable energy and artificial intelligence infrastructure, while supply growth remains constrained by permitting delays, declining ore grades and rising project complexity.

Anglo is in this environment with one of the industry's most attractive development pipelines. The company has spent the past two years simplifying its portfolio and concentrating capital on assets capable of generating higher returns through the commodity cycle. That process is beginning to reshape both the earnings profile and the strategic identity of the business.

Attention remains centred on Chile. Copper production is expected to improve modestly during the second quarter following the temporary restart of additional processing capacity at Los Bronces. Water availability continues to be one of the principal operating challenges across the region, making desalination infrastructure increasingly important to future production stability. Although the environmental permitting setback at the Collahuasi desalination project introduces some uncertainty, the long-term direction remains unchanged. Significant capital has already been invested, and the project plays an important role in Chile's broader water management strategy. Management therefore appears confident that a workable solution can ultimately be found. At the same time, iron ore is experiencing a more difficult operating backdrop. South African and Brazilian exports face higher freight costs than Australian competitors, while energy and diesel expenses continue to pressure profitability. Those headwinds partly offset the strength in copper, but they also reinforce the rationale behind Anglo's ongoing portfolio repositioning. The company is becoming progressively less dependent on businesses with weaker structural growth prospects and greater exposure to cyclical cost inflation.

The next eighteen months will likely determine whether this transformation is completed successfully. Several major transactions remain outstanding, including the sale of the diamond business, regulatory approval for the nickel disposal, completion of the steelmaking coal transaction and the closing of the Teck Resources joint venture. Collectively, these steps should leave Anglo with a far more focused portfolio centred on copper and premium iron ore assets.

Looking further, management continues to explore opportunities to optimise its Chilean operations through closer integration between neighbouring assets, creating additional potential for productivity improvements and lower operating costs. This strategic simplification comes at a time when long-term copper fundamentals continue to strengthen. While near-term earnings will inevitably remain influenced by commodity prices and operational execution, the business is becoming increasingly aligned with one of the most attractive structural themes in global mining.

If management delivers on the remaining portfolio changes, Anglo American could emerge over the next several years as one of the purest large-cap listed vehicles for investors seeking long-term exposure to copper demand.

CRH (CRH US): Doubling down on America's fastest-growing infrastructure markets

CRH has strongly been reshaping itself into a predominantly North American infrastructure and construction materials business, and the acquisition of Arcosa represents another serious step in that direction.

The company's biggest deal ($8.5bn EV in cash) expands CRH's exposure to some of the most attractive construction markets in the United States, particularly Texas, the Southeast and parts of the Southwest where population growth, industrial investment and infrastructure spending continue to outpace national averages. Arcosa ($2.9bn revenue and ~$580m EBITDA in 2025) brings a high-quality aggregates platform with significant reserve life, alongside a fast-growing engineered structures business serving electricity transmission, grid modernisation and data-centre construction.

These are markets benefiting from long-term structural investment themes that extend well beyond traditional construction cycles. The transaction strengthens CRH's position in areas where demand visibility is relatively strong and where barriers to entry remain meaningful.

The engineered structures business may ultimately prove just as important as the aggregates assets. Electricity networks across the United States require substantial investment over the coming decade as utilities upgrade ageing infrastructure and accommodate growing power demand from electrification, manufacturing reshoring and artificial intelligence-related data centres. Arcosa is already a significant supplier of transmission structures and related products, giving CRH exposure to a market that is expanding independently of residential construction activity.

At the same time, the aggregates business provides a complementary source of growth through public infrastructure projects and state transportation budgets. The reserve base is particularly attractive, offering decades of future production potential in regions where permitting new quarries is increasingly difficult. This combination of infrastructure materials and critical infrastructure products broadens CRH's growth profile and reduces dependence on any single end market. Management also sees substantial opportunities for operational improvements, logistics optimisation, procurement savings and vertical integration benefits, with targeted synergies exceeding levels typically associated with previous acquisitions.

That said, by most conventional measures, Arcosa is not a cheap acquisition. The multiple paid (~11.5x EV/EBITDA) sits above several recent transactions completed by large building materials groups and reflects the premium often attached to high-quality U.S. infrastructure assets. Investors initially reacted cautiously for that reason.

The question is whether the quality of the assets and the growth opportunities justify the purchase price. Management appears confident that synergies (roughly $60m in yr 1 and $130m in yr 2), operational improvements and favourable end-market exposure will support attractive returns over time, but much of that value creation will take several years to emerge. Near-term financial returns are likely to look modest relative to the capital deployed.

Even so, the transaction provides an interesting signal about CRH's future direction. The company is increasingly becoming a pure-play North American infrastructure operator, and this acquisition further concentrates the portfolio around that theme. It may also increase the likelihood of future portfolio simplification, including the potential disposal of remaining non-core European assets.

SGS (SGSN Switzerland): Growth remains intact as the transformation phase begins to fade

SGS enters the second half of 2026 from a position of relative strength. The company is dealing with some temporary disruption from geopolitical events in the Middle East, but the broader operating picture remains remarkably stable. Exposure to the region is limited, and the group's diversification continues to demonstrate its value. While the impact from Iran-related disruption is expected to be more noticeable in the second quarter than it was in the first, management's message has not changed materially. Organic growth remains consistent with guidance, and most end markets continue to perform well. This highlights one of SGS's core strengths. The business is not dependent on a single geography, industry or testing category. Instead, it participates across a broad range of inspection, testing and certification activities that collectively provide a resilient growth profile. As a result, localised disruptions rarely have a lasting impact on overall performance. Current market expectations still point to organic growth above 5% this year, with some improvement anticipated as the year progresses.

The quality of growth across the portfolio remains encouraging. Health & Nutrition continues to benefit from strong demand in food testing, offsetting softer conditions in pharmaceutical services where early-stage research spending remains constrained by biotech funding conditions. Natural Resources faces the most direct impact from Middle East disruptions, particularly within oil, gas and chemicals, yet minerals and metallurgy activity remains healthy enough to offset much of that weakness. Industries & Environment is also progressing steadily despite a small drag from project-related activities and the continued exit from lower-quality contracts.

The latter is particularly important because it reflects a deliberate effort to improve profitability. Over the past several years, SGS has been reshaping parts of its portfolio, improving operational discipline and focusing on higher-return activities. That process is now reaching a point where the benefits are becoming increasingly visible. Growth is no longer dependent on restructuring actions or portfolio optimisation. Instead, the company is beginning to generate growth from a stronger operational base.

Margins remain another important component of the investment case. Management continues to balance profitability improvement with investment in future growth areas, including digitalisation, artificial intelligence and operational efficiency initiatives. This may limit the pace of margin expansion in the near term, but it should strengthen the competitive position of the business over time. Current expectations still call for margin improvement this year, followed by further gains in 2027.

The upcoming capital markets day later this year could become an important milestone because the company is already approaching several objectives outlined in its existing strategic plan. Management will likely have the opportunity to present a new framework focused less on recovery and more on acceleration.

Amadeus IT (AMS Spain): Strong fundamentals are running into a difficult travel backdrop

Amadeus finds itself in the unusual position of executing reasonably well while facing external conditions that are becoming increasingly challenging. The company's core business remains tied to global air travel volumes, and those volumes weakened materially during the second quarter following disruption across the Middle East. Passenger traffic growth, which began the year on a relatively healthy footing, slowed sharply as airlines adjusted capacity, routes were disrupted and booking patterns became more volatile.

Management appears to be seeing the same trend. Discussions with the company suggest that recovery has been gradual rather than immediate, leaving the second quarter significantly weaker than originally anticipated. The impact extends across multiple parts of the business. Air IT continues to benefit from healthy revenue per passenger boarded, but lower traffic volumes are limiting growth. Distribution activity has also been affected as airline bookings softened during April and May. Even Hospitality Solutions, which has historically provided some diversification away from aviation, is expected to feel the effects through weaker bookings, payments activity and media-related revenues.

The issue is not that Amadeus has lost competitive position. In fact, the underlying franchise remains exceptionally strong. The company continues to benefit from deep integration with airlines, travel agencies, airports and hospitality providers. Revenue quality remains attractive, pricing trends remain healthy and cost discipline appears intact. Air IT revenue per passenger boarded continues to grow at a solid pace, demonstrating the value of the software and technology services embedded within customer operations. This is particularly important because it shows that the current weakness is volume-driven instead of competitive. Airlines remain dependent on Amadeus' infrastructure and continue investing in technology despite a more uncertain operating environment. The company's long-term drivers also remain intact. Digital transformation within travel, airline retailing, airport modernisation and cloud migration continue to support demand for Amadeus' products.

The challenge is that these structural opportunities cannot fully offset a slowdown in global travel activity over a period of several quarters. When passenger growth weakens, the effects inevitably flow through the model.

Attention is therefore shifting towards guidance. Management entered 2026 assuming air traffic growth above 4%, an assumption that no longer appears realistic. Industry forecasts now point closer to 2%, creating a gap that will be difficult to bridge through pricing alone. The company still appears capable of protecting profitability thanks to disciplined cost management and a more favourable cloud cost profile, but revenue growth expectations have become harder to defend.

Amadeus is not facing a structural problem. It is facing a cyclical slowdown that is affecting one of the most important drivers of its business. The market increasingly expects management to acknowledge this reality through a reduction in full-year growth guidance. Such a move would not necessarily change the long-term investment case, but it could weigh on sentiment in the near term, particularly if second-quarter results come in below expectations.

The business remains one of the highest-quality software franchises in Europe. The problem is that quality alone may not be enough to offset a softer travel environment during the remainder of 2026.

Bureau Veritas (BVI France): Temporary disruption is obscuring a business that continues to improve

Bureau Veritas is heading into its first-half results with momentum that appears weaker.

The principal reason is geopolitical disruption across the Middle East, which has delayed inspection work, reduced activity in oil and gas and interrupted project schedules across several divisions. Industry has been the most affected, particularly where refinery maintenance has been postponed and customers have delayed discretionary operating expenditure. These disruptions are expected to weigh on second-quarter growth, but they appear to reflect timing instead of lost business.

Management continues to describe the commercial pipeline as healthy and expects delayed work to be executed during the second half. This distinction is important. Bureau Veritas is not experiencing a deterioration in demand across its core markets. Instead, parts of its inspection business are waiting for projects that have been deferred rather than cancelled. The company's diversified portfolio also limits the financial impact, preventing weakness in one region or activity from dominating overall group performance.

Performance across the portfolio remains uneven but generally constructive. Buildings & Infrastructure continues to benefit from sustained investment in data centres and large construction projects, reinforcing one of the company's strongest structural growth drivers. Technology within Consumer Products Services also maintains healthy momentum, although Softlines faces more demanding comparisons after an exceptionally strong prior year. Marine & Offshore is naturally moderating following an unusually robust period of growth, while Certification continues to recover more slowly than initially expected as customers take longer to finalise contracts and begin new projects. Agri-Food & Commodities is dealing with a combination of Middle East disruption and portfolio changes within government-related activities.

Viewed individually, these developments create a mixed picture. Collectively, they suggest a business that continues to grow across most end markets but is temporarily affected by project timing and external events. Management expects many of these headwinds to ease during the second half, allowing the underlying growth trajectory to become more visible again.

Margins are likely to follow a similar pattern. The first half is expected to absorb the operational impact of lower laboratory utilisation, project delays and foreign exchange effects, resulting in weaker profitability than investors have become accustomed to. Management nevertheless continues to guide towards margin improvement for the full year, implying a meaningful recovery during the second half as activity normalises and delayed projects return. That recovery should also benefit from improved absorption of fixed costs and a stronger conversion of the existing order pipeline.

Bureau Veritas has spent several years improving the quality of its business through portfolio optimisation, operational discipline and investment in higher-growth activities. Those efforts remain intact despite the softer first-half outlook. The company therefore appears to be dealing with cyclical disruption instead of structural weakness. If activity in the Middle East gradually returns and commercial conversion improves as expected, the second half should provide a clearer indication of the earnings potential embedded within the business.