World Cup ads, AI and inflections

M6, Sodexo, Agrana, Infineon Technologies, Nexans, Orège, Allegro, De' Longhi, BMW, Bechtle, DO & CO, Schneider Electric, Argan

At Lux Opes, we break down companies into quick takes that get straight to the point - what is happening, why it matters, and what to watch next. We publish 2-4 times per week, depending on the news flow.

For the best reading experience, we recommend reading at Lux Opes

Important note: With the summer holidays coming up, we will take a break for a few weeks as of next week. Lux Opes will return, just in time for earnings season to kick off.

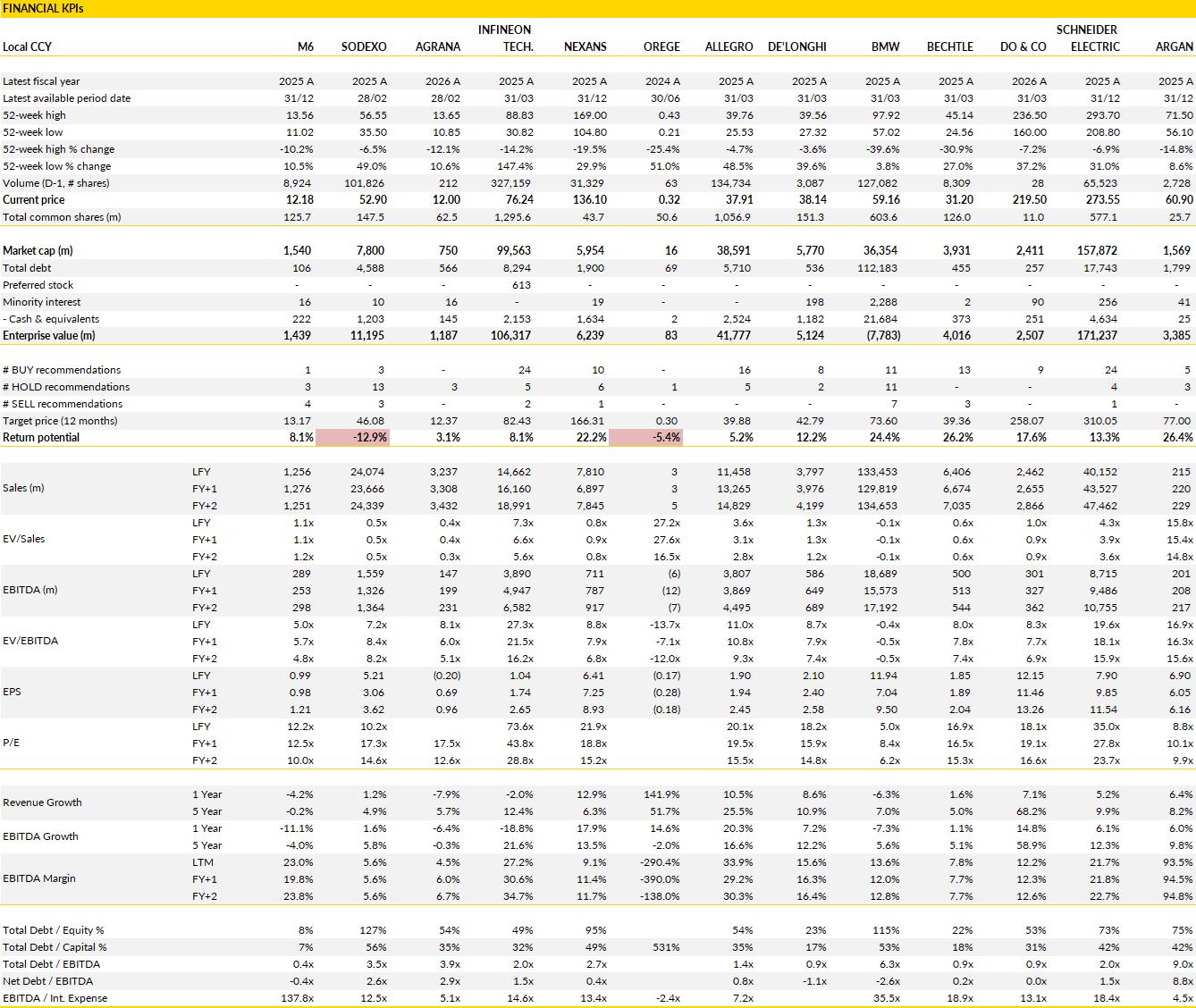

Financial KPIs

Companies covered in this edition: M6, Sodexo, Agrana, Infineon Technologies, Nexans, Orège, Allegro, De' Longhi, BMW, Bechtle, DO & CO, Schneider Electric, Argan

M6 (MMT France): World Cup advertising tailwind offsets softer audiences

The World Cup is proving to be a rather nuanced event for M6.

Average audiences have fallen compared with the 2018 and 2022 tournaments, reflecting a less favourable match schedule and an expanded competition format. However, this does not necessarily translate into weaker commercial performance. The French national team continues to attract exceptional audiences whenever it plays in prime time, demonstrating that the tournament's advertising value remains concentrated around the country's biggest matches. France's opening match against Senegal attracted around 14 million viewers with a 61.4% audience share, while the match against Norway reached 13.7 million viewers and a 62.1% share.

More broadly, although average audiences per match have declined, the larger number of matches broadcast means M6's cumulative audience during the group stage is expected to exceed that achieved by TF1 during previous World Cups.

Advertising revenue remains the key consideration. The strong reach generated by France's matches and the larger overall inventory of televised games should support second-quarter advertising income, even if the tournament itself carries a substantial cost. Broadcasting rights reportedly amounted to around €130m, meaning the immediate contribution to operating profit is likely to remain negative despite stronger advertising sales. The second half of the tournament becomes mroe important because financial upside now depends largely on how far France progresses. Every additional knockout match involving the national team materially increases advertising inventory, audience reach and pricing power. If France advances deep into the competition, the tournament could provide a meaningful revenue boost extending into the third quarter. Conversely, a (relatively) early elimination would significantly reduce that benefit. The commercial outcome remains closely linked to sporting performance over the coming weeks.

Beyond the World Cup, the investment case remains centred on M6's strategic positioning within the French television market. Advertising remains cyclical, but the company continues to generate solid cash flow while maintaining one of the strongest balance sheets among European broadcasters.

The possibility of further consolidation within French television also remains an important source of optionality. A combination with TF1 has long been viewed as strategically attractive given the potential to strengthen advertising, streaming and content economics, even though previous attempts failed on competition grounds. While no transaction appears imminent, structural pressures facing the European broadcasting industry continue to favour consolidation over the longer term.

Sodexo (SW France): North America stabilises, stronger third quarter, higher FY26 growth

Sodexo delivered a better third quarter than many expected, suggesting the operational reset announced earlier this year is beginning to gain traction.

Revenue rose 0.9% to €6.17bn, comfortably ahead of market expectations, with organic growth of 2.0%. Pricing remained broadly stable at around 2.4%, while volumes improved to roughly 1%, a noticeable step up from the first half. Net new business was still slightly negative, but the drag eased as the impact of previously lost contracts started to fade. North America remained the weakest region overall, yet performance improved materially, with Healthcare and Sodexo Live! more than offsetting continued pressure in Education. Europe grew 0.6%, reflecting the earlier loss of a large facilities management contract, while Healthcare remained resilient. The Rest of the World once again stood out with organic growth of 10.6%, driven by recently won contracts moving into execution.

The stronger quarter prompted Sodexo to raise its organic growth guidance for the current financial year. The company now expects growth of 1.2-1.5%, compared with the previous range of 0.5-1.0%, while leaving its EBIT margin target unchanged at 3.2-3.4%. The revised outlook still assumes a relatively cautious final quarter, implying organic growth somewhere between a small decline and modest growth, suggesting management prefers to see further evidence that recent improvements are sustainable.

Even so, the third quarter provides a more encouraging picture than earlier in the year. Pricing continues to hold up, volume trends are improving, and contract losses are becoming less of a headwind. Healthcare remains the most dependable growth engine across several regions, while the Live business continues to benefit from healthy activity levels across sporting and entertainment events.

Attention now shifts to the Investor Update scheduled for 16 July, where management is expected to outline its medium-term ambitions. That event should provide a clearer indication of how quickly margins can recover once the current operational initiatives begin flowing through the income statement. Sodexo still generates more than half of its revenue from relatively defensive end markets, giving the business greater resilience than many cyclical service companies, while management continues to focus on operational efficiency after several years of inconsistent execution.

In short, this trading update does not remove every concern, particularly around North America, but it does suggest that the business is moving in the right direction.

Agrana (AGR Austria): Restructuring benefits begin to come through

Agrana's preliminary first-quarter results suggest that the restructuring program is finally delivering some tangible financial benefits.

Revenue declined 3% year-on-year to €855m, mainly because of weaker sugar volumes, but profitability improved far more than expected as operational changes across the business started feeding through. Operating profit increased to €33.2m, lifting the operating margin to 3.9%, while reported EBIT climbed to €35.4m from just €5.7m a year earlier. Part of that improvement reflects the absence of restructuring charges recorded in the comparable period, but the underlying trend also points to genuine operational progress. Management's efforts to simplify the business, improve efficiency and restore profitability within the starch and sugar operations are beginning to produce measurable results after several difficult years.

The strongest improvement came from the Agricultural Commodities & Specialities activities, where both the starch and sugar businesses benefited from the restructuring measures implemented over the past year. While sugar remains the group's most challenging division, there's (early) evidence that profitability is recovering despite continued pressure on volumes. That is an encouraging development because the turnaround has so far depended more on cost reductions and operational improvements than on a recovery in market conditions.

So the first-quarter performance demonstrates that Agrana has greater control over its earnings trajectory than what the market may previously have assumed. Management also maintained its full-year guidance, targeting revenue growth of 1-5% and EBIT of €70-90m, signalling confidence that the first quarter represents the beginning of a broader recovery instead of a one-off improvement.

That said, the investment case remains balanced between improving execution and the structural challenges still facing the business. Sugar continues to operate in a difficult market characterised by pricing pressure and volatile production economics, making it too early to conclude that the turnaround has been fully secured. The market will therefore look closely at the detailed first-quarter results for further evidence that profitability improvements are becoming sustainable across all divisions.

Even so, the latest update represents one of the clearest indications to date that Agrana's restructuring program is gaining traction. After several years in which earnings repeatedly disappointed, management has started demonstrating that operational improvements can offset at least part of the difficult industry backdrop. Sustaining that momentum over the coming quarters will be critical if the company is to regain the market's confidence.

Infineon Technologies (IFX Germany): Dresden expansion positions the group for the next phase of AI power demand

Infineon has officially opened its new Smart Power fabrication facility in Dresden, marking the largest manufacturing investment in the company's history and significantly expanding capacity for one of its fastest-growing businesses.

The project represents roughly €5bn of investment, of which around €2bn has already been committed to construction and the remaining €3bn will be spent on production equipment as utilisation ramps up. The 300mm fab targets power semiconductors used in AI data centres, industrial automation and automotive applications, with management estimating annual revenue potential of at least €5bn once fully loaded. Production equipment has already started arriving ahead of schedule, although the factory remains largely empty for now. Management believes that, if current demand trends persist, capacity could be fully utilised within two and a half years, illustrating how rapidly investment in AI infrastructure is impactingh the power semiconductor market.

The timing looks favourable because capacity, instead of demand, has become the main constraint. Infineon already targets at least €2.5bn of AI-related power semiconductor revenue in fiscal 2027 after approximately €750m in 2025 and around €1.5bn expected in 2026, but management has repeatedly stressed that the 2027 objective should be viewed as a minimum rather than an upper limit.

The Dresden expansion provides the manufacturing headroom needed to pursue substantially higher volumes if customer demand continues accelerating. Recent commercial developments support that view, including Infineon's participation in NVIDIA's MGX AI Factory ecosystem and its partnership with Siemens around solid-state circuit breakers. Beyond GPUs themselves, the power management content required throughout AI data centres continues to increase as server power consumption rises, creating additional demand for power semiconductors across power conversion, cooling and electrical distribution systems. This broadens Infineon's opportunity well beyond supplying individual components.

The longer-term opportunity is substantial, although much of the optimism already appears reflected in the share price. AI has become a meaningful growth driver alongside the company's established automotive and industrial businesses, and the new Dresden capacity reinforces Infineon's ability to capture that demand over the coming years. At the same time, investors should recognise that power semiconductors have historically become more competitive as capacity expands, particularly once Chinese manufacturers increase investment, a pattern already seen in several automotive power markets. Whether AI power follows a similar path remains uncertain, but it remains a consideration beyond the current investment cycle.

Operationally, however, Infineon continues to execute well, adding capacity before supply becomes constrained while strengthening relationships with leading AI infrastructure customers. The Dresden facility therefore represents more than another factory; it provides the manufacturing foundation needed to support the company's next phase of growth as electrification and AI converge.

Nexans (NEX France): Republic Wire strengthens US exposure as growth pipeline continues to expand

Nexans is entering the second half of the year in an even stronger position in the US following the acquisition of Republic Wire.

Management recently reaffirmed its existing EBITDA guidance of €730-810m, although this still excludes the contribution from Republic Wire, which has been consolidated since 1 June and will be incorporated into updated guidance at the interim results. Trading trends remain largely consistent with the first quarter. The transmission division is expected to post weaker organic growth because of project phasing and a demanding comparison base, while Grid and Connect continue to deliver steady expansion. Grid remains particularly attractive, with EBITDA margins expected to stay above 15%, although Connect is likely to see a modest margin headwind from a less favourable regional mix. Free cash flow should remain relatively subdued in the near term as elevated capital expenditure and lower customer prepayments offset the underlying earnings strength.

The Republic Wire acquisition further reinforces Nexans' electrification strategy and looks financially attractive. The business generates around €520m of annual revenue, with more than 90% of sales coming from the US low-voltage cable market serving utilities, distributors and municipalities. Nexans paid an enterprise value of €680m, with potential additional earn-outs of €43m, implying valuation multiples that fall from 10.3x EBITDA before synergies to 7.6x after expected cost savings. Management targets €23m of annual synergies within three years, with roughly half expected during the first year. The acquisition therefore provides an immediate earnings contribution while expanding Nexans' presence in one of its most attractive end markets. Reflecting the transaction, full-year EBITDA expectations have increased to €818m, up 12.5% from last year, while 2027 EBITDA is expected to reach €922m as Republic Wire contributes for a full twelve months.

The medium-term outlook remains supported by several additional growth drivers. Management continues to pursue new medium-voltage infrastructure projects to replace the lost GSI contract, with announcements expected during the second half and financial contributions potentially beginning in the fourth quarter. The current guidance also excludes any benefit from those potential awards, making the lower end of the range appear deliberately conservative.

Beyond project wins, Nexans continues to benefit from structural investment in electrification and grid infrastructure, while operational execution keeps improving across its core businesses. Even after the recent share price recovery, the company continues to trade at a meaningful discount to major peers (NKT, Prysmian) despite similar earnings momentum and attractive margin prospects.

Orège (OREGE France): Service model gathers momentum but profitability remains some way off

Orège remains a business in transition, with FY25 highlighting both the progress made in reshaping the business model and the financial cost of that transformation.

Revenue was broadly unchanged at €3m, well below 'market' expectations (there is just one analyst covering), as service revenue reached €2.3m while equipment sales contributed €0.7m, mainly in the UK. The company reported an underlying operating loss of €8.9m, wider than the previous year, reflecting higher operating expenses as Orège continued investing in engineering capabilities in France, expanded its US operations and established a dedicated manufacturing and supply chain organisation. The bottom line deteriorated further, with the net loss widening to €14.4m after a much weaker financial result.

The figures show clearly that Orège is still investing well ahead of revenue growth, with the benefits of those investments yet to appear.

The strategic direction, however, is becoming clearer. Rather than relying primarily on equipment sales, Orège is increasingly building a recurring service business around its mobile sludge treatment units. That shift accelerated during 2025, with services accounting for around 70% of revenue compared with just 20% a year earlier, supported by a fleet that has expanded roughly 3.5 times since the investment programme began in 2024. Management indicated that contracted service revenue for 2026 already exceeds total revenue generated during 2025, providing a degree of visibility that the business previously lacked. Growth is expected to come primarily from the US and UK, where Orège continues deploying mobile units for municipalities and industrial customers. The company has also secured longer-term contracts, including a nine-year agreement with a US dairy producer using its SLG technology, showing the potential for recurring revenue once installations move into operation.

A second growth avenue is also emerging through biogas applications. Orège's Green Gas technology increases biogas production by up to 40% while reducing sludge volumes, offering wastewater operators a more attractive economic proposition as renewable gas production becomes increasingly important. The company signed a new service contract with a Spanish municipality during 2025 and continues developing agricultural anaerobic digestion projects through pilot installations in both the US and France.

These opportunities could broaden the addressable market beyond traditional sludge treatment, but commercial adoption remains gradual and requires continued investment. With net debt standing at €76m and losses still substantial, cash consumption remains an important consideration. The recurring revenue model appears fundamentally stronger than the historical equipment-focused approach, but the pace of commercial expansion will ultimately determine how quickly Orège can convert into success.

Allegro (ALE Poland): Stronger domestic execution and improving international business lift the outlook

Allegro continues to strengthen its leadership in Polish e-commerce while its international expansion is (finally) becoming credible.

Allegro remains the clear market leader in Poland, supported by an ecosystem that extends well beyond its marketplace into logistics, payments and advertising. Those higher-value businesses continue to grow faster than the core platform, creating additional revenue streams and deepening customer engagement. Advertising revenue increased 25% year over year in the first quarter, marking a sixth consecutive quarter of faster growth than GMV, while logistics revenue more than doubled as Allegro expanded its own delivery capabilities. The SMART! subscription programme also remains a powerful competitive advantage, with members spending around seven times more than non-subscribers. Management expects to meet full-year guidance, while the planned expansion of the Allegro One Box network and a new cooperation framework with InPost could further improve logistics economics over time.

Outside Poland, the business is becoming much cleaner following the disposal of the loss-making Mall South operations and the restructuring of Mall North. These actions have reduced losses and sharpened the focus on the Czech Republic, Slovakia and Hungary, where operating trends continue to improve. First-quarter international GMV rose 67% and active buyers increased over 30%, prompting management to raise its full-year international growth targets. The company still expects the international division to reach break-even by 2029, but the path towards that is now more visible as scale improves and weaker operations have been removed from the portfolio. Combined with continued strength in Poland, the international business is gradually shifting from being a drag on earnings to (slowly) becoming a meaningful source of future growth.

Another important development is the removal of a long-standing technical overhang on the shares. Permira's sale of 131 million shares effectively clears the market of concerns surrounding a large secondary placement, and the stock has already responded positively. At the same time, Allegro's balance sheet remains strong enough to support its planned PLN 1.6bn share buyback while still leaving room for bolt-on acquisitions.

The combination of double-digit GMV and EBITDA growth, improving profitability abroad, expanding higher-margin revenue streams and greater capital flexibility strengthens the investment case.

De' Longhi (DLG Italy): Coffee leadership and premium mix continue to support higher earnings

De' Longhi's long-term growth outlook continues to be driven by coffee, where the company remains one of the strongest global players across both consumer and professional markets.

Its leadership in fully automatic and manual espresso machines, combined with relatively low penetration in markets such as the US and parts of Europe, leaves ample room for further expansion. At the same time, the Professional Coffee division is developing into an increasingly important earnings contributor as coffee chains continue to expand, automation becomes more widespread and customers move towards premium equipment. Together, these trends are expected to keep organic revenue growth comfortably above historical levels over the coming years (>6% pa), with Professional Coffee growing materially faster than the traditional consumer business.

The improving business mix is also becoming a more meaningful earnings driver. As Professional Coffee represents a larger share of revenue, profitability should gradually improve given its structurally higher margins. Operational efficiencies and manufacturing discipline provide an additional tailwind, allowing margins to expand even as the company absorbs temporary headwinds from tariffs, input costs and product mix changes during 2026. While this year is expected to deliver broadly stable EBITDA margins, the underlying trajectory remains positive (towards ~17%), supported by higher volumes, increasing exposure to premium products and continued operational improvements. The result should be steadily rising earnings as the contribution from higher-margin businesses continues to increase.

Financial flexibility remains another important strength. Strong free cash flow generation, disciplined capital expenditure and an expected net cash position of almost €1bn looking out a few years provide considerable scope to invest without putting pressure on the balance sheet. Management therefore has the capacity to pursue targeted acquisitions, particularly within Professional Coffee, where further consolidation could strengthen the group's market position and broaden its product offering.

Despite these advantages, the shares continue to trade at a meaningful discount to peers, even though De' Longhi combines above-average growth, expanding margins, robust cash generation and one of the strongest balance sheets in the sector. This combination makes the company well placed to continue delivering attractive shareholder returns over the medium term.

BMW (BMW Germany): New leadership raises expectations, but investors still need stronger evidence of change

BMW's recent investor event marked the first major appearance of new CEO Milan Nedeljković and offered an early indication of the direction he wants to take the company.

Management acknowledged the key challenges facing the business, including weaker conditions in China, rising trade barriers and a more demanding regulatory environment, while signalling that cost discipline will become a much greater priority. More details are expected at the Capital Markets Day in September, but the broad message is operational improvement. Current earnings expectations remain largely unchanged following the profit warning issued in June, as the market waits to see whether the planned efficiency measures can materially improve profitability.

The leadership transition appears constructive, although the proposed changes stop short of a fundamental transformation. Nedeljković brings extensive manufacturing experience and intends to focus heavily on reducing costs, particularly across the supply chain, with restructuring expenses expected to reach roughly €1bn during the second half of the year.

Even so, BMW continues to pursue its established strategy centred on flexible powertrain technology, the rollout of the Neue Klasse platform and its global manufacturing footprint. That continuity may reassure long-term customers and suppliers, but it may not be sufficient to convince investors looking for a more decisive response to structural pressures, especially in China, which still represented around 25% of first-quarter vehicle volumes and remains the company's biggest challenge.

Product development and manufacturing remain clear competitive strengths. BMW unveiled the new X5, which will be offered with five different powertrain options spanning internal combustion, mild hybrid, plug-in hybrid, battery electric and hydrogen fuel-cell technology. This broad offering strenghtens BMW's position in one of the industry's most profitable SUV segments while supporting a richer sales mix from 2027 onwards. Production will continue at the Spartanburg plant in South Carolina, BMW's largest manufacturing facility with annual capacity of around 450,000 vehicles. The scale, flexibility and efficiency of the site provide an important competitive advantage in the US market at a time when tariffs and protectionist policies are becoming increasingly relevant.

Even so, with meaningful exposure to China and only incremental strategic changes announced so far, the market is likely to remain focused on whether the September strategy update delivers a more convincing roadmap for accelerating earnings growth.

Bechtle (BC8 Germany): Public sector demand and international expansion continue to drive growth

Bechtle appears set for another solid quarter, with demand remaining healthy across both hardware and software despite a more uncertain macroeconomic backdrop.

Volume is expected to rise over 10% to more than €2.15bn, comfortably ahead of revenue growth in the hsd% (~€1.6bn), reflecting continued strength in order intake. Germany remains well supported by public sector spending, while international operations are increasingly contributing to growth as both government and private sector customers continue investing in IT infrastructure. Profitability should also improve, with earnings before tax expected to increase by ldd%, although ongoing investment in internal IT systems and higher depreciation continue to weigh modestly on margins.

Overall, trading suggests that demand has remained resilient across most end markets, even if management is likely to remain cautious when discussing the second half of the year.

The underlying mix is also evolving in a favourable direction. Software continues to represent a growing share of demand, although activity remains broad-based across infrastructure, services and hardware rather than being concentrated in any single category. PC pricing remains above historical levels, but management has indicated that the period of widespread price increases is probably coming to an end as competitive pressure among vendors intensifies. Future growth is therefore likely to depend more on volumes, customer mix and services than on pricing.

AI-related projects continue to increase, particularly around Microsoft Copilot deployments, although they still account for only a small proportion of overall revenue. More importantly, these projects reinforce Bechtle's position as an adviser and systems integrator rather than simply a reseller, creating opportunities for higher-value consulting, implementation and managed services as enterprise AI adoption gradually expands.

Despite the strong first-half momentum, management is unlikely to raise full-year guidance when second-quarter results are released. Visibility into the second half remains limited, particularly around customer spending patterns, year-end public sector budgets and vendor rebate programmes that typically influence profitability later in the year. This caution seems understandable given the seasonal nature of the business rather than any deterioration in underlying demand.

Bechtle also appears relatively well placed to benefit from the structural changes taking place across enterprise IT. While concerns about AI disrupting traditional IT services have weighed on sector valuations, the company's strengths lie in integrating complex IT environments, managing long-term customer relationships and delivering end-to-end technology solutions, areas where AI is more likely to improve productivity than replace the service offering. Continued international expansion, resilient public sector demand and a growing software and services mix leave the business well positioned even if near-term guidance remains conservative.

DO & CO (DOC Austria): Premium positioning continues to lift margins

DO & CO delivered another record year, demonstrating that demand for its premium catering model remains strong across airlines, sporting events and hospitality.

Revenue increased 7.1% to €2.46bn during the financial year, while EBIT rose to €212m from €184m, lifting the operating margin from 8.0% to 8.6%. The company also increased its dividend to €2.50 per share from €2.00 previously. Geopolitical disruption in the Middle East had only a modest impact despite affecting the final quarter, reducing revenue by around €16m and EBIT by €2-3m. Even with those headwinds, the fourth-quarter EBIT margin remained a healthy 8.3%, highlighting the resilience provided by a diversified customer base and a flexible operating model.

Management expects that momentum to continue into the new financial year, guiding for revenue growth of 7-8% alongside another year of margin expansion to 8.6-9.0%. The guidance appears achievable given the continued strength in premium travel demand and improving operating efficiency. If geopolitical conditions continue to stabilise, trading could prove somewhat stronger than current expectations.

Beyond this fiscal year, profitability should continue to benefit from a richer customer mix, disciplined cost control and pricing improvements across existing contracts. The recently expanded partnership with American Airlines also provides an additional source of earnings growth as volumes ramp up over the coming years.

Scale benefits, operational discipline and a premium market position continue to lift margins, while the balance between airline catering, international events and hospitality reduces reliance on any single end market. Management now believes operating margins can move into the 9-10% range over time, suggesting there is still room for further earnings expansion.

With strong cash generation, rising profitability and a business model that has demonstrated resilience even during periods of geopolitical disruption, DO & CO remains well positioned to continue delivering attractive growth over the medium term.

Schneider Electric (SU France): Cognite for the next phase of industrial AI

Schneider Electric is acquiring Norwegian industrial software company Cognite for $3.1bn in cash, adding another strategic asset to the software platform it has built around Aveva.

Founded in 2017, Cognite develops AI-enabled software for asset-intensive industries, helping customers organise and contextualise operational data before applying advanced analytics and AI. The company generated more than $170m of revenue in 2025 and serves sectors including energy, utilities, chemicals, mining, infrastructure and manufacturing. Financially, the transaction is easily digestible, increasing net debt/EBITDA from roughly 1.2x to 1.5%, while regulatory approvals are expected over the coming quarters. The acquisition is small relative to Schneider's overall size, but strategically it addresses one of the most attractive parts of industrial automation as manufacturers increasingly seek to turn operational data into productivity gains through AI.

We get the industrial rationale. Schneider has spent years expanding beyond electrical equipment into software, automation and digital services, with Aveva becoming the centrepiece of that strategy. Cognite complements (instead of overlaping) with those capabilities by providing the data architecture that allows AI applications to operate across complex industrial environments. Management described the company as unique in combining data contextualisation, knowledge graphs and agentic AI into a single platform, allowing industrial customers to connect previously fragmented data and deploy AI across operations. Aveva's installed base of more than 23,000 customers should significantly accelerate commercial adoption, while Cognite gains immediate global reach and access to industries where Schneider already holds leading positions.

In short, the acquisition extends Schneider's software offering, while further increasing exposure to recurring software revenues and higher-margin digital services.

But the main question today is about valuation. Paying high-teens 2025 revenue is a demanding multiple for a business generating just over $170m of annual sales, although Schneider has historically shown a willingness to pay premium prices for strategically important software assets. Management disclosed few financial details beyond highlighting Cognite's attractive gross margins, suggesting the emphasis is on long-term strategic value rather than near-term earnings accretion.

Ultimately, success will depend on Schneider's ability to scale Cognite through its global commercial network and embed its AI capabilities across the broader automation portfolio. Given Schneider's track record of integrating software businesses, its strong cash generation and continued focus on organic growth, the transaction strengthens an already differentiated position in industrial automation and leaves the group well placed as AI becomes an increasingly important driver of productivity investment across manufacturing and infrastructure.

Argan (ARG France): Full occupancy and disciplined expansion continue to sustain steady growth

Argan delivered another dependable set of rental figures for the first half of 2026, highlighting the resilience of its logistics portfolio despite a more subdued French leasing market.

Rental income increased 4% to €109.7m, largely reflecting the full contribution from developments completed during 2025 together with the annual 0.6% rent indexation implemented at the start of the year. More importantly, occupancy remained at 100% following the successful re-letting of the 32,000m² Coudray-Montceaux warehouse to JS Logistics at a prime rental level. This performance contrasts with a French logistics market where tenant decision-making remains cautious and vacancy rates have risen to around 7%. The absence of vacant space allows Argan to continue converting rental growth into recurring cash flow without sacrificing pricing or occupancy, a combination few property owners are currently achieving.

Management responded by modestly increasing its 2026 rental income guidance to at least €221m from €220m, effectively removing the conservative vacancy assumption embedded in the original outlook. The investment program also remains firmly on track. Six developments were completed during the first half for customers including Puma, Pomona, Celio, Ferrero and Danone, while two additional projects for Jacky Perrenot and ID Logistics are scheduled for delivery later this year. The ID Logistics project has even been brought forward by two months, allowing rental income to begin earlier than originally planned.

Total investment for 2026 has been confirmed at around €160m, €5m below the initial estimate without affecting expected rental income, reflecting lower acquisition costs rather than changes to the development pipeline. The program continues to target returns above 6%, maintaining the disciplined capital allocation that has characterised the business for many years.

Visibility beyond this year also appears encouraging. During its recent asset tour, management indicated that nearly €100m of investment has already been secured for 2027 through pre-let developments with high-quality tenants, while additional projects remain under negotiation. That provides confidence that rental growth can continue without relying on speculative construction.

Attention now shifts to the more detailed first-half results later this month, where investors will look for confirmation that recurring earnings remain on track following the refinancing of the group's €500m bond. Argan continues to differentiate itself through full occupancy, long-term tenant relationships and disciplined development rather than aggressive expansion.