PE interest, China worries and positive profit warnings

Edenred, BMW, UMG, Arm Holdings, Siltronic, Theon, Whitbread, Kapsch TrafficCom, Straumann, LVMH, Medincell

At Lux Opes, we break down companies into quick takes that get straight to the point - what is happening, why it matters, and what to watch next. We publish 2-4 times per week, depending on the news flow.

For the best reading experience, we recommend reading at Lux Opes

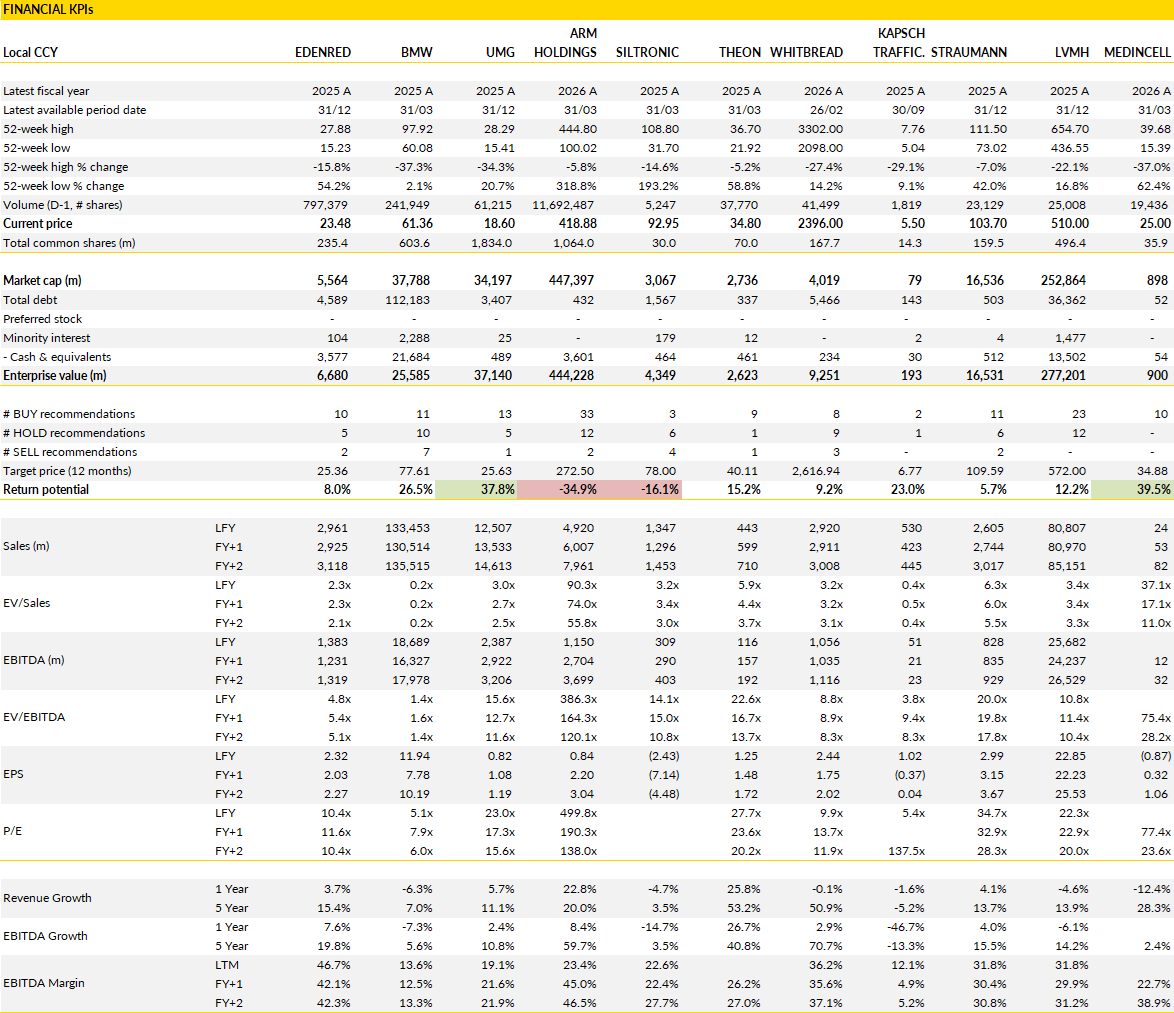

Financial KPIs

Companies covered in this edition: Edenred, BMW, UMG, Arm Holdings, Siltronic, Theon, Whitbread, Kapsch TrafficCom, Straumann, LVMH, Medincell

Edenred (EDEN France): PE interest shows the valuation disconnect

Edenred traded the past year as if its growth profile had permanently deteriorated. Regulatory concerns, particularly around meal vouchers in France, combined with a broader derating of payment and fintech-related businesses, have pushed the shares down to valuation levels rarely seen.

Against this backdrop, it is no surprise to see PE interest from 'multiple funds' (a.o. BC Partners reported). The rumoured approaches remain highly preliminary and no formal proposal has emerged, but the interest itself is noteworthy. Private equity likes to focus on businesses with recurring revenue, strong cash generation, modest leverage and opportunities for operational value creation. Edenred checks each of those boxes. The company also benefits from a fully dispersed shareholder base, making a transaction structurally easier.

The valuation gap is the central issue here. The shares trade at levels that imply a substantial discount not only to historical averages but also to many businesses with weaker growth profiles. Meanwhile, the underlying fundamentals remain intact. Edenred continues to benefit from the digitisation of employee benefits, the expansion of mobility and corporate payment solutions, and ongoing penetration opportunities across multiple geographies. Markets such as Italy and Brazil remain important growth drivers, while the business generates substantial free cash flow with relatively limited capital requirements. Net debt remains modest, providing flexibility for acquisitions, shareholder returns or, from a private equity perspective, transaction financing.

It is therefore easy to understand why financial sponsors would be attracted to an asset capable of generating more than €800m of annual free cash flow within a few years.

An important question of course is whether public markets are undervaluing the business or whether current risks justify the discount. France remains the biggest uncertainty. Debate around meal voucher regulation has not disappeared and could return to the political agenda later this year. Any discussion around caps on merchant fees would naturally attract investor attention given the importance of the French market.

Even so, the current share price appears to assume a much harsher outcome than management or industry participants currently expect. That disconnect is precisely what creates this interest. Reports suggest a potential valuation in the €27-28 range, implying a premium of more than 30% to the current share price.

Whether a deal ultimately emerges is of course tough to predict. What the rumours do highlight, however, is that strategic and financial buyers may be looking at the same business and reaching a very different conclusion from public equity investors. The market continues to focus on regulatory uncertainty. Potential acquirers on cash generation, balance-sheet strength and long-term growth. At current valuation levels, that difference is difficult to ignore.

BMW (BMW Germany): China turns into a big headache

The scale of BMW's latest profit warning points to a much deeper issue, namely the continued deterioration of its position in China.

Automotive margins are now expected at just 1-3%, down from a previous 4-6% target, while Automotive EBIT is set to fall by roughly 60% versus earlier expectations. Deliveries are also expected to decline modestly this year rather than remain broadly stable. For a company that historically generated some of the highest margins among European premium manufacturers, these numbers are painful.

Management highlighted weaker vehicle demand in China and across parts of Asia, rising logistics costs, some raw material inflation and more than €1bn of restructuring-related charges. The restructuring component explains only part of the downgrade. The bigger issue is that China, which still represented roughly a quarter of BMW's sales, is no longer providing the earnings support investors had become accustomed to over the last decade. And the challenge goes beyond short-term demand weakness. Chinese manufacturers continue to gain share across both mass-market and premium segments, often combining competitive pricing with increasingly sophisticated technology offerings. Foreign brands that once relied on strong pricing power are finding it harder to defend market positions without sacrificing profitability.

BMW now faces a difficult balancing act between preserving volumes, maintaining brand positioning and protecting margins. Management has indicated that strategic and cost restructuring measures will be accelerated, with further details expected later this year. That suggests the company increasingly views the situation as structural instead of temporary. The question is no longer whether China recovers next quarter. It is whether BMW can reshape its Chinese business to generate acceptable returns in an environment where local competitors have become far stronger and where premium European brands no longer enjoy the same advantages they once did. And that's a tough one.

The market will also naturally wonder whether similar pressures are building at other German manufacturers with significant Chinese exposure. Mercedes-Benz, Volkswagen and Porsche all face related questions around pricing, market share and profitability. BMW remains financially solid, continues to support shareholder returns and has not altered its buyback program or dividend framework.

Even so, earnings expectations are going to be moving sharply lower. The stock may appear inexpensive compared with its own history, but historical valuation ranges were established during a period when China consistently generated attractive profits. That benchmark has become less useful if the economics of the market have changed permanently. BMW is now entering a phase where restructuring, cost control and capital discipline are likely to matter more than volume growth.

Until there is evidence that profitability in China has stabilised, it is difficult to argue that the shares deserve a higher valuation multiple.

Universal Music Group (UMG Netherlands): The overhang is gone and the market is missing the cash flow story

UMG has spent much of the past year in between two concerns that had little to do with the day-to-day performance of the business.

The first was ownership uncertainty. Investors worried about large shareholders (Pershing Square) reducing positions and flooding the market with stock. The second was AI. The fear was that generative AI would weaken the economics of recorded music, erode the power of major labels and shift value creation elsewhere in the ecosystem. Together, those concerns pushed the shares down roughly 30% over the past year and compressed valuation multiples to levels that would have been difficult to imagine when the company came public.

Today, UMG trades at around 9x forward EBITDA, much lower vs the multiples investors were willing to pay only a few years ago. Yet the underlying business remains one of the strongest collections of intellectual property assets in global media, with recurring revenue streams, growing monetisation opportunities and considerable operating leverage.

The ownership issue now looks considerably cleaner. Pershing Square has exited its position, removing a source of uncertainty that had weighed on sentiment for months. The process also triggered several shareholder-friendly actions from management, including a larger buyback program, additional capital returns and improved communication around strategy and capital allocation. Just as important, other major shareholders have made it clear they are not looking for an exit at current prices. That reduces the risk of continued technical pressure on the stock and allows investors to focus on fundamentals again. The market's attention can now shift back towards revenue growth, margin development and free cash flow generation instead of speculating about who might be selling next.

The AI discussion has also evolved. UMG is not approaching AI as a defensive battle against technological change. The company is trying to ensure that AI develops inside the existing rights ecosystem rather than outside it. That involves renegotiating artist contracts, securing broader rights ownership, signing commercial agreements with AI platforms and aggressively protecting intellectual property where necessary. If successful, the result is not value destruction but an expansion of the company's role in the music value chain. At the same time, the traditional streaming business remains healthy. Management expects paid streaming growth to accelerate during the year, helped by pricing actions and improved market share trends.

The more important figure, however, is free cash flow. The market appears focused on theoretical AI disruption several years from now while paying limited attention to a business that could grow free cash flow from roughly €1.4bn in 2025 to around €2.4bn by 2028. This kind of growth profile is unusual among large-cap media companies.

UMG still faces questions around technology, licensing and platform economics, but the debate increasingly looks disconnected from the cash generation trajectory of the business. The shares are no longer being priced as a scarce global music asset. They are being priced as if structural disruption is inevitable. That gap explains why the stock remains one of the more interesting opportunities in European media today.

Arm Holdings (ARM US): Ambitions keep expanding as data centre momentum accelerates

Arm is clearly no longer being valued as a mobile processor licensing company. The market is increasingly treating it as one of the central infrastructure providers for the AI era, and recent management comments suggest the company's own long-term ambitions may still be understated.

What stands behind this optimism is not simply higher chip demand but a structural shift in computing architecture. AI workloads are changing the balance between CPUs and GPUs, particularly as inference becomes a larger part of the market. Training clusters remain GPU-heavy, but inference requires far more CPU resources to manage data movement, orchestration and memory access. That shift expands Arm's addressable market substantially. The company's 2031 framework already assumes a dramatic increase in revenue, yet management appears to be working from assumptions that leave considerable room for upside if AI infrastructure spending remains on its current trajectory. Capacity constraints remain one limiting factor today, but these are expected to ease toward the end of the decade, opening the door to a larger deployment cycle.

The most important development is the emergence of Arm's AGI CPU platform. The product is attracting attention from hyperscalers and AI infrastructure builders because it addresses two of the industry's biggest constraints: power consumption and capital intensity. Management argues that Arm-based CPUs can deliver meaningful efficiency improvements versus traditional x86 architectures while allowing greater server density. For operators spending tens of billions of dollars on AI infrastructure, small improvements in power efficiency can translate into enormous savings.

The customer list continues to expand and now includes major cloud and AI players across the ecosystem. Demand indications have moved well beyond the levels originally discussed when the initiative was first unveiled. Arm is targeting a future where it controls the overwhelming majority of the data centre CPU market through a combination of direct products and licensing revenue. Whether those market-share ambitions prove achievable remains to be seen, but the direction here is clear. The company is moving closer to the centre of AI infrastructure rather than remaining a technology supplier several layers removed from the end market.

The valuation remains the obvious hurdle here. After a growth spurt that has already been extraordinary, traditional metrics offer little comfort. Investors buying Arm today are not paying for current earnings; they are paying for what the company could become by the end of the decade. The bullish argument is that even the recently announced 2031 targets may prove conservative. Revenue assumptions are built around a CPU market that could be materially larger than current expectations, while future opportunities outside data-centre CPUs remain largely excluded from management's framework. New silicon categories, accelerator-related opportunities and broader AI infrastructure spending could all become additional growth drivers over time.

The risk is equally clear. Expectations have become exceptionally high, and any sign that adoption is progressing more slowly than anticipated would likely have an outsized impact on sentiment. Even so, management's message remains consistent: the company sees itself at the beginning of a much larger opportunity than the one outlined in its current long-term plan.

Siltronic (WAF Germany): A much needed capital increase

Siltronic completed a 10% capital increase, placing 3 million new shares at €91 each for proceeds of €273m. The issue was carried out without subscription rights and priced at a 7% discount. The number of shares will rise from 30 million to 33 million, implying dilution close to 10%. HAL Trust, the largest shareholder, participated meaningfully in the placement. The new shares began trading on 17 June and are fully fungible with the existing line from 19 June, carrying dividend rights from the start of 2026.

The capital raise is aimed at reinforcing a balance sheet that has been strained by the investment cycle linked to the FabNext plant in Singapore. Net debt has climbed to around €1bn, while cash generation has remained limited during the ramp‑up phase. The additional equity improves financial flexibility and provides support for the continued scaling of the new facility, at a time when early signs of recovery are emerging in the 300mm wafer market.

The operation also reflects the sharp rise in the share price since the beginning of the year, which created a favourable window to strengthen the capital structure. Although the company had previously indicated it was not considering such a move, the scale of recent investments made the balance‑sheet reinforcement increasingly necessary.

Siltronic is entering a more constructive phase as inventories normalise in logic and memory and AI‑related demand builds, but the strong share‑price performance over the past year and a valuation now above historical cycle peaks limit the scope for further upside.

Theon International (THEON Netherlands): Acquisition of HGH

Theon International has taken a major strategic step by entering exclusive negotiations with Carlyle to purchase 100% of SAS Stéropès, the parent company of HGH Systèmes Infrarouges. The proposed transaction values HGH at roughly €300m and will be financed entirely through a bridge facility, meaning no equity issuance.

Based on the information disclosed, HGH generates around €40m of revenue (2025e), has grown close to 30% annually since 2023, and operates with EBITDA margins above 40%. Using an implied EV/EBITDA multiple in the high‑teens HGH’s EBITDA would be near €16–18m. The company also brings a solid order book of about €70m and is expected to lift Theon’s group margin profile while adding mid‑single‑digit EPS accretion by FY 2027. Management expects that, once synergies are realised over the next two to three years, the effective acquisition multiple should fall toward ~10x EBITDA.

HGH gives Theon an immediate foothold in one of the fastest‑expanding defence niches - counter‑drone detection and tracking. Its SPYNEL panoramic sensors and CYCLOPE analytics software are well‑established, ITAR‑free technologies already deployed in demanding environments. For Theon, this strengthens its relevance within NATO programs and accelerates its ambition to build a broader, multi‑domain sensing and optics platform. The acquisition also deepens the company’s presence in France, following earlier moves such as the Exosens stake and the Merio acquisition, marking a rapid and deliberate expansion into a strategically important market.

While HGH adds high‑quality EBITDA, the bridge‑financed structure means leverage will rise meaningfully - pro forma net debt/EBITDA is expected to exceed 2.5x. The near‑term earnings uplift is modest relative to the size of the debt taken on, making the path to deleveraging dependent on smooth integration, synergy capture and continued operational execution.

Even so, the message here is clear. Theon is moving aggressively to scale its technology offering, consolidate its position in France and broaden its relevance across defence sensing domains. The HGH acquisition fits right on within that strategy and, if executed well, should strengthen the company’s long‑term competitive positioning.

Whitbread (WTB UK): Germany gains scale as UK trading begins to stabilise

Whitbread’s first quarter offered another indication that conditions in its core UK market may finally be moving in a better direction.

The numbers were not spectacular, but they were better than expected and showed improvement compared with the sluggish backdrop seen over recent quarters. Accommodation revenue returned to growth, supported by a combination of slightly higher pricing and improved occupancy. London remained the strongest region, though the broader UK estate also moved in the right direction. Food and beverage sales continued to face pressure as the company pushes through its operational restructuring program, but that weakness was anticipated and reflects management’s willingness to sacrifice some short-term revenue in pursuit of a more efficient operating model. In short, the UK business appears to be holding up.

Germany continues to be the more interesting part of the story. The business is still relatively small compared with the UK operation, yet growth remains strong as the network expands and occupancy improves. Whitbread has spent years investing in building a second growth engine outside its domestic market, and the German operation is increasingly moving from investment phase to scale-up phase.

The attraction is clear. Germany remains a fragmented hotel market with a large independent operator base, creating opportunities for a national branded chain to gain share. Every new hotel opening increases brand awareness, strengthens distribution and improves operating leverage across the platform. The pace of growth remains well ahead of the UK business and management continues to report healthy booking trends. If execution remains on track, Germany has the potential to become a much more meaningful contributor to earnings over the second half of the decade.

Regarding the company’s five-year plan. Management is targeting a business that generates more cash, requires less capital and delivers higher returns on invested capital. The emphasis is on extracting greater value from the existing estate, improving efficiency and free cash flow conversion.

This approach becomes particularly attractive given the current valuation. The shares continue to trade below historical multiples despite a stronger German platform, a more disciplined capital allocation framework and a clearer roadmap for shareholder returns.

That said, UK demand remains sensitive and Germany must continue delivering against ambitious expansion targets. Even so, with forward bookings running ahead of last year and Germany maintaining strong momentum, Whitbread appears to be entering the next phase of its strategy with more favourable conditions than it has experienced for some time.

Kapsch TrafficCom (KTCG Austria): A difficult year masks improving fundamentals

Kapsch TrafficCom's 2025-26 results looked weak, at first glance.

Revenue fell almost 19% and EBIT declined close to 40%, hardly the profile investors typically look for. The numbers however need to be viewed in the context of several exceptional factors. The group lost roughly €80m of revenue following the end of the Gauteng tolling contract in South Africa and the disposal of its Belarus operation. Project delays, a sluggish global tolling market and slower contract awards also weighed on activity. Against this, management still delivered revenue and EBIT above guidance and ahead of market expectations. The company also benefited from the settlement related to Germany's failed tolling project, but even excluding that contribution, the underlying picture looks more stable than the headline decline suggests. North America, which had been a problem area for several years, continued its recovery and contributed both improved profitability and new business wins.

The most encouraging aspect of the update is the order environment. New orders reached approximately €496m during the year, comfortably above annual revenue, while backlog climbed to around €1.3bn. That backlog provides a degree of visibility that is often missing in smaller infrastructure technology businesses. Management also highlighted that some customer-related delays should reverse during the current year, creating an opportunity for revenue recovery without relying entirely on new contract awards. The tolling business remains the core earnings engine and generated a stronger margin than expected despite lower activity levels. Traffic management was weaker, slipping into a loss, but that division accounts for a smaller portion of group profitability.

The overall takeaway is that Kapsch appears to have moved beyond the period when investors were primarily worried about contract disputes, balance-sheet pressure and execution problems. The focus is gradually shifting back towards project delivery and earnings (recovery).

The outlook remains cautious, which is understandable given the state of the global tolling market. Management is only guiding for revenue and EBIT growth rather than providing aggressive targets. Even so, cost control remains disciplined, the backlog is healthy, North America is improving and delayed projects should contribute to activity levels over the next twelve months.

The investment case is mainly becoming a recovery story centred on operational execution and margin rebuilding. After several years dominated by restructurings, legal disputes and contract losses, Kapsch is finally in a position where normal business performance matters more than exceptional events. If management can convert backlog into revenue and continue rebuilding profitability, the current valuation still leaves room for a meaningful reappraisal.

Straumann (STMN SW): A positive profit 'warning'

Straumann has lifted its profitability outlook for 2026 after seeing stronger‑than‑expected operational improvements across all business areas, a favourable regional mix, and lower tariff costs. The company now expects core EBIT margin expansion of 140-170 basis points at constant currencies, compared with the earlier range of 30-60 basis points. This reflects broad‑based progress rather than reliance on any single market, with efficiency gains and cost discipline contributing meaningfully to the upgrade.

Across its franchises, Straumann is benefiting from manufacturing efficiencies, supply‑chain optimisation and tighter cost management, which are driving higher gross margins and better operating leverage. Orthodontics continues to improve as the Smartee transformation advances, and profitability in intraoral scanners is also moving in the right direction. These trends indicate that the company’s operational measures are taking effect faster than initially expected. Straumann also expects up to CHF 17m in tariff refunds, though these are excluded from the updated guidance as they are non‑core in nature.

In China, the expected rollout of VBP 2.0 has been delayed, keeping pricing conditions more favourable for longer. Customer destocking has largely run its course, and patient demand is gradually normalising. The new Shanghai campus supports margins, and the absence of price cuts linked to VBP has made the delay beneficial for profitability. As a result, the company is seeing improving earnings momentum in the region.

The revised guidance implies a margin uplift well above current market expectations, which still reflect a more cautious view. With the new range pointing to a 140-170 basis‑point improvement from last year’s 25.2% core EBIT margin, consensus is likely to move higher. The timing and scale of the upgrade stand out, and the company’s recent commentary suggests that operational execution is tracking ahead of plan.

LVMH (MC France): The recovery is uneven, but the pieces are starting to fall into place

The luxury sector is still operating in a difficult environment, yet the discussion around LVMH is gradually moving to be about 'recovery'.

The key Fashion & Leather division remains under pressure, but that pressure is shrinking. After a 2% decline in the first quarter, the business appears close to returning to growth despite ongoing weakness among Chinese consumers, subdued spending in Europe and disruption linked to the Middle East. Expectations have come down over recent months, particularly for brands such as Dior, but the operational trends now suggest that the worst phase may be passing. Jewellery continues to perform well, Sephora remains a reliable growth engine and several brands that struggled through 2024 and early 2025 are beginning to show signs of stabilisation. That does not mean growth is about to surge, but it suggests that the earnings cycle is turning in the right direction.

Much of the focus remains on Fashion & Leather because that division drives the majority of group profits. Louis Vuitton remains the most important piece of the puzzle, accounting for roughly half of divisional revenue. Store traffic is still mixed and consumers remain selective, but management's efforts around product development, merchandising and brand management appear to be laying the groundwork for a return to moderate growth once macroeconomic conditions improve.

Dior is becoming increasingly important in that context. The brand has spent the last year navigating a creative transition while working through product-cycle challenges. Recent indications are more encouraging. Core leather goods are stabilising, newer product launches are gaining traction and comparisons become easier in the second half of the year. Beyond Dior, brands such as Céline and Fendi also have room for operational improvement. Taken together, the division looks far healthier than it did six months ago, even if reported growth remains modest in the near term.

LVMH does not need a return to boom conditions to produce attractive earnings growth. Even under relatively conservative assumptions, Fashion & Leather is expected to move from roughly flat growth this year toward a more normal mid-single-digit trajectory next year. That would allow group EBIT growth to accelerate meaningfully after a period of stagnation.

The shares no longer trade at the premium multiples investors once associated with the luxury sector, yet LVMH retains the strongest collection of brands in the industry, broad geographic exposure and substantial financial flexibility. Luxury stocks have recovered somewhat from recent lows, but LVMH still trades at a discount to many peers despite having arguably the highest-quality portfolio in the sector.

The debate is slowly shifting away from how bad conditions can get and toward how quickly profitability can recover. That is a much healthier discussion than the one investors were having a year ago.

Medincell (MEDCL France): The upcoming ramp-up should sustain the momentum

Medincell reported annual revenue of €24.3m, a decline mainly explained by the absence of last year’s one‑off milestone payments. Beneath this, the shift toward recurring, higher‑margin royalties is becoming clearer. Royalties from UZEDY reached €9.3m, up 42% yoy, supported by a 54% increase in product sales at Teva, though partly offset by currency effects. Partnership revenue totalled €10.2m, including €6.4m from AbbVie. Operating costs rose 17% to €45.0m due to higher R&D spending and expanded commercial functions, resulting in an operating loss of €20.8m and a net loss of €31.3m. Cash burn was €24.6m, but the company ended the year with €84.8m in cash following a €48.2m capital raise in March.

The company now enters a period dense with strategic milestones. UZEDY’s commercial trajectory continues to strengthen, and its recent approval in bipolar disorder broadens the product’s reach. The long‑acting olanzapine formulation is progressing through the US regulatory process, with a potential FDA decision expected in the fourth quarter of 2026. Meanwhile, the first clinical programme emerging from the AbbVie partnership has been pushed to 2027, extending the timeline but not altering the strategic relevance of the collaboration. Beyond these headline assets, Medincell is advancing a pipeline of more than ten programmes, adding depth and optionality to its medium‑term outlook.

Short‑term profitability remains constrained by the deliberate increase in investment, but the company’s financial profile should gradually improve as UZEDY scales and olanzapine LAI approaches launch. The delay in AbbVie’s first clinical entry removes one near‑term catalyst but does not change the broader momentum of the portfolio. With a strengthened balance sheet, expanding royalty streams and several catalysts approaching, visibility on the growth trajectory continues to improve.

Medincell’s evolution toward a business model anchored in recurring, higher‑margin revenue is becoming more evident. Rising contributions from commercial products, a maturing late‑stage pipeline and a reinforced financial position together create a more robust foundation for the next phase of expansion.