Live entertainment, insurance and big price corrections

eDreams ODIGEO, CTS Eventim, Jungheinrich, Novem, Transgaz, CD Projekt, UNIQA, easyJet, Abivax, Laurent-Perrier

At Lux Opes, we break down the latest company news into quick takes that get straight to the point - what happened, why it matters, and what to watch next.

We publish 2-4 times per week, depending on the news flow.

We are moving our email sending to our custom domain. As such, you might temporarily receive emails either from Ghost or Lux Opes.

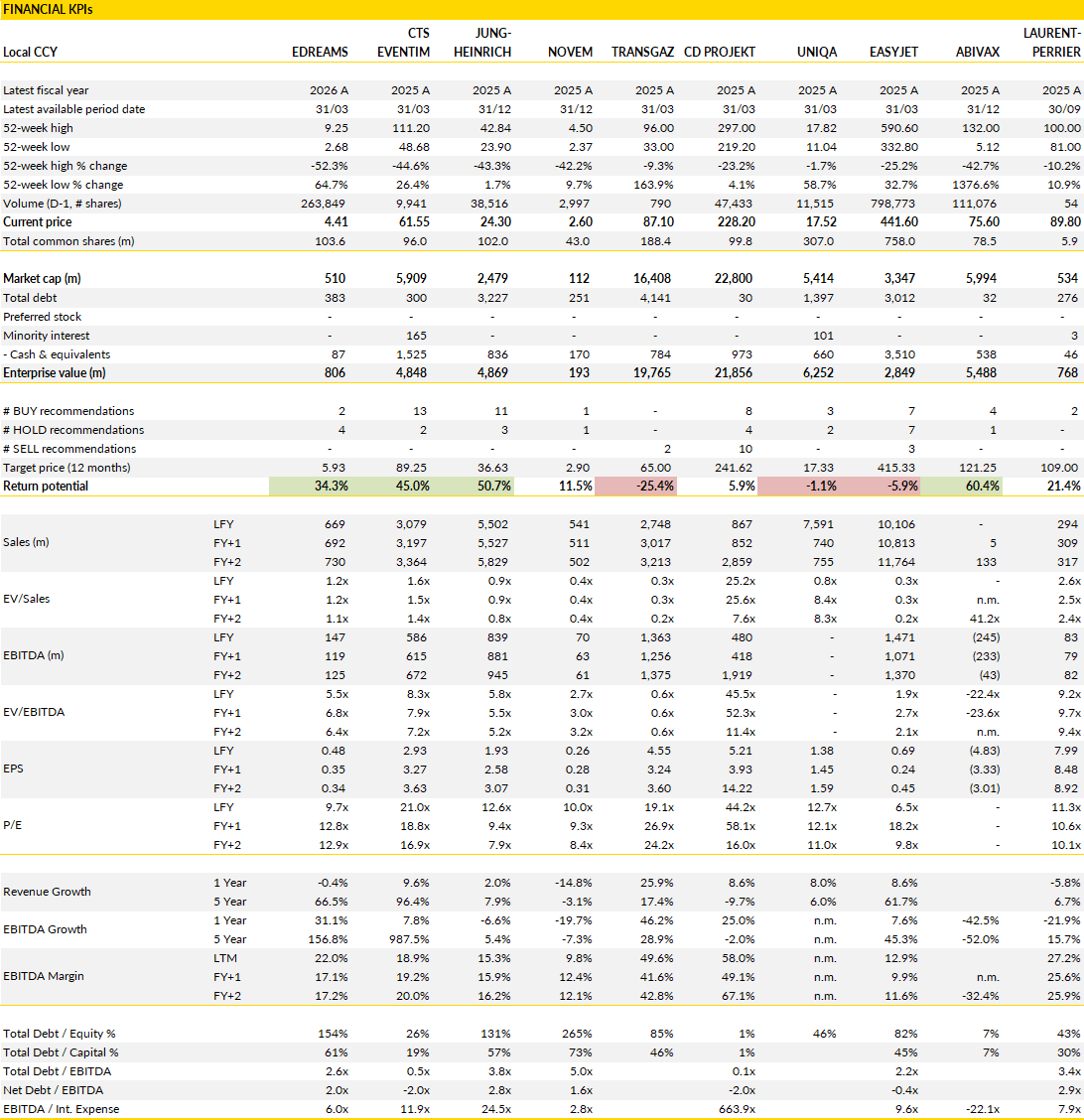

Financial KPIs

eDreams ODIGEO (EDR Spain): one of the most polarising companies in our coverage

eDreams spent much of the past year trying to rebuild investor confidence after the profit warning that massively damaged credibility in 2025. The latest results suggest that process is progressing better than many expected.

The headline revenue figures were somewhat distorted by the ongoing transition from annual Prime subscriptions to monthly payments, creating a temporary drag on reported cash revenue metrics. Looking behind that accounting effect, the underlying business remained stable and profitability improved substantially. Adjusted EBITDA rose 29% to €172m, while adjusted net profit reached a record €73m, up more than 40% from the previous year. The key driver of which was Prime, which finished the year with roughly 8 million subscribers, slightly ahead of management's own targets.

The economics of the platform also improved. Variable costs declined (-11%), customer acquisition became more efficient and the subscriber base matured further. Those developments are important because they show the model generating better profitability without relying on aggressive spending. A few years ago, many investors questioned whether Prime could actually evolve this way and become a central driver of the business. Today that debate looks largely settled.

Guidance for the next financial year was largely unchanged and broadly aligned with market expectations, but the 2030 ambitions moved materially higher. Management now targets more than 13 million subscribers by the end of the decade, comfortably above what most analysts had previously modelled. Cash EBITDA is expected to exceed €270m, again ahead of prevailing expectations.

The route to those targets is fairly straightforward. Prime remains the centrepiece, but the company is also widening the ecosystem around it. Rail bookings, additional travel products and broader multi-product offerings are becoming larger pieces of the strategy. Geographic expansion remains another lever. Artificial intelligence also featured prominently in management's commentary, although the practical application is more interesting than the (usual) marketing language. The company is using AI to improve customer acquisition, personalise offers and reduce service costs. If executed properly, those initiatives can support margins without requiring a major increase in customer spending. Management clearly believes the addressable opportunity is larger than previously assumed.

The gap between operational progress and valuation remains quite large. Even after the recent recovery in the share price (though relatively small), eDreams still trades at levels that imply a considerable degree of scepticism about the durability of Prime and the company's ability to deliver its long-term objectives.

That discount is partly understandable given the events of 2025, but the latest results suggest the business is moving in the right direction again. Subscriber growth remains healthy, profitability is expanding and management is comfortable raising its long-term ambitions. The coming year will still involve elevated investment spending as the company pushes further into new markets and products, which may limit near-term earnings upgrades.

Even so, the business is increasingly behaving like a subscription platform with travel distribution attached to it, not simply an online travel agency. If subscriber growth remains close to current levels and the economics of Prime continue improving, the valuation gap with other subscription-oriented platforms will become harder to justify over time.

CTS Eventim (EVD Germany): strong event activity

CTS Eventim began 2026 with a quarter shaped by strong demand in Live Entertainment, lifting group revenue to €614m, a 23% increase from last year. The Live Entertainment division delivered the bulk of the growth, supported by a busy event schedule in Germany and the US and the first contributions from the new Unipol Dome in Milan. Revenue in this segment reached €404m, and venues added around €40m with a high margin profile. Ticketing grew more modestly at 3% to €219m, reflecting changes in the partnership with Stage Entertainment. Adjusted for this effect, Ticketing revenue rose 6%. Group adjusted EBITDA reached €119m, with margins slightly lower due to the heavier mix of Live Entertainment, where profitability improved but remains structurally below Ticketing.

The Ticketing division maintained a strong margin of 41%, though slightly below last year, while Live Entertainment saw its margin rise to 7.2% as event volumes increased and venue utilisation improved. Costs linked to the company’s internal excellence program remained small in the quarter.

Management confirmed all full‑year outlook statements, signalling confidence in both divisions despite the mix shift. The company also noted that the first ticket sales for the Los Angeles 2028 Olympics will begin in the second quarter, with total revenue from the event expected to reach a low triple‑digit million euro amount over time.

The quarter also highlighted the growing importance of the company’s venue strategy, which has been a recurring topic among investors. With several large projects underway, questions around capital allocation and long‑term returns continue to shape sentiment. Management plans to address these concerns at the capital markets day in September, where it will outline the role of venues in the group’s broader growth strategy. In the meantime, the strong performance in Live Entertainment and the resilience of Ticketing provide a stable backdrop for the rest of the year.

CTS Eventim is showing confidence, with a robust event pipeline and early visibility on major projects such as the Olympics. While the mix shift toward Live Entertainment affects margins, the underlying demand picture remains healthy across markets. The company continues to balance investment in venues with the cash‑generating strength of its Ticketing platform, setting the stage for further updates later in the year.

There's still a lot of discussion on the strategy, but given the strong rerating of the shares, a lot of negativity is currently priced in.

Jungheinrich (JUN3 Germany): cheap shares alone are not enough

Jungheinrich has spent years being viewed as one of the higher-quality names in European intralogistics, but the latest reset highlights how much the operating environment has changed.

The company recently reorganised its reporting structure, separating the former Intralogistics division into Industrial Trucks & Services (ITS) and Automation & Warehouse Equipment (AWE). This offers a much clearer picture of where profits are actually being generated, and the conclusion is not especially encouraging.

The first quarter already pointed to weaker factory utilisation and disappointing profitability, but the new disclosure reveals that AWE was only marginally profitable during 2025 and slipped into losses during the opening quarter of 2026. At the same time, the hoped-for acceleration in demand has failed to materialise. Economic activity across key European markets remains subdued, customers continue to delay investment decisions and geopolitical uncertainty has added another layer of caution. Against this, earlier expectations for a sharp recovery now look too optimistic. The combination of weaker volumes, lower factory utilisation and a less supportive macro backdrop forces a more conservative assessment of earnings power over the next few years.

The biggest concerns centres on the profitability of the core ITS business. Management continues to guide towards an EBIT outcome that implies a very strong second half, but achieving those numbers would require margin levels that look difficult to reconcile with current demand conditions. Even assuming some improvement in activity, reaching the upper part of management's target range would require a meaningful step-up in operational performance.

There are also structural factors worth remembering. The loss of the Russian business removed a particularly profitable earnings stream, making comparisons with previous peak margins less relevant. Meanwhile, the automation activities remain in investment mode and are not contributing materially to group profitability.

As a result, we expect a continued adjustment to the market's earnings expectations for this and the next few years. The company's ambitious long-term aspirations, including its revenue targets for the end of the decade, now look increasingly disconnected from what current market conditions would suggest. Investors may eventually begin to question whether those objectives remain achievable without a significant acquisition programme.

The valuation is what keeps attracting attention. On conventional metrics the shares look remarkably cheap. Even after adjusting for the complexity of the leasing business and capital structure, the stock trades at levels that appear difficult to justify if earnings stabilise and growth returns. That argument has existed for several years, however, and it has not been enough to unlock shareholder value.

Investor confidence has taken a hit following weaker execution, softer profitability and management changes, including the departure of the CFO. There is also a realistic possibility that official guidance drifts towards the lower end of the current range as the year progresses. Those factors help explain why the valuation discount persists. The shares undoubtedly look inexpensive on paper, but cheap stocks often stay cheap when confidence is missing.

For Jungheinrich, the next step is proving that margins can recover, automation can generate meaningful returns and management can consistently deliver against expectations. Until those elements become visible in reported results, the discount is likely to remain in place despite what appears to be a very modest valuation.

Novem (NVM Germany): A difficult year marked by weak demand and limited visibility

Novem closed the 2025-26 financial year with results that reflected another period of soft market conditions and subdued call‑offs from automotive customers.

Preliminary revenue fell 6% to €511m, while adjusted EBIT declined to €32m, bringing the margin down to 6.2%. Earnings were affected by lower volumes and a less favourable mix, although the company managed to keep leverage stable at 1.8x and lifted free cash flow to €48m through tighter control of working capital and investment spending. Reported EPS held at €0.26, with the gap to adjusted expectations explained by higher tax payments and a larger difference between adjusted and reported EBIT.

The company did not issue formal guidance for the new financial year, consistent with its usual practice, but indicated that the current environment remains challenging. Order visibility from OEMs is still limited, and geopolitical tensions add another layer of uncertainty to demand planning. Management expects revenue in 2026-27 to move broadly sideways to slightly higher, supported by ongoing efficiency measures and cost reductions. Margins are expected to improve modestly as these initiatives take hold, although the pace of recovery will depend on whether volumes stabilise or begin to recover from the low levels seen over the past two years.

The company continues to focus on the areas it can influence directly, including cost discipline, capital expenditure and working‑capital management. These efforts helped stabilise key financial indicators during a year marked by declining sales and earnings. However, the broader market backdrop remains muted, and a meaningful improvement in profitability will require a sustained pickup in production volumes from automotive customers. Without that, margins are likely to remain well below the double‑digit levels the company achieved in stronger years.

As Novem enters the new fiscal year, the main themes remain unchanged: a cautious demand outlook, limited visibility on customer call‑offs and a focus on internal measures to protect profitability. The coming year will hinge on whether market conditions stabilise enough to support higher utilisation and a gradual rebuilding of margins.

Transgaz (TGN Romania): a strong past is becoming a difficult comparison

Transgaz entered 2026 facing a challenge that often follows an exceptionally strong year: comparisons become far more demanding. The first quarter illustrates that dynamic.

Revenue declined from the unusually elevated levels seen a year earlier, while profitability also moved lower. On the surface the figures may appear disappointing, but the context is important. Early 2025 benefited from extraordinary short-term capacity bookings on the BRUA corridor that inflated earnings and created a difficult benchmark. Against that, the latest quarter looks like a return to normal operating conditions. Revenue reached almost RON 1bn and exceeded expectations, while EBIT and net profit also came in ahead of forecasts. Domestic transport revenues weakened as booked capacity revenues declined, reflecting a different mix of contracts and fewer short-term booking peaks. At the same time, transported volumes increased by 14%, providing evidence that underlying gas flows remain healthy. The contribution from Vestmoldtransgaz was also stronger than anticipated, helping offset some of the pressure elsewhere in the business.

Operating costs moved higher during the quarter, driven by rising depreciation charges, higher personnel expenses and larger provisions. These factors pushed EBIT down 20% year-on-year to RON 441m and reduced margins from the exceptionally high levels achieved in the prior-year period. Financial income was another source of pressure. Inflation-linked adjustments applied to the regulated asset base were substantially lower than last year, reducing a contributor that had previously supported earnings. Interest expenses increased as financing costs moved higher.

None of these developments were unexpected, yet they highlight a business entering a different phase. The earnings growth enjoyed during recent years was closely linked to investment activity and expansion of the regulated asset base. Investors now need to assess what earnings growth looks like when that engine slows. The current project pipeline appears considerably lighter than during the previous investment cycle, with several major projects pushed further into the future.

That issue sits today at the centre of the valuation debate. The share price has performed strongly and significantly outpaced the broader market during 2026. Investors appear to be assigning substantial value to the company's regulated profile, healthy balance sheet and strategic role in regional energy infrastructure.

The question is whether future earnings justify that optimism. With major capital projects delayed beyond 2028 and limited visibility on another meaningful expansion of the regulated asset base, the earnings trajectory looks less compelling than the valuation implies. The stock now trades well above both its own historical averages and many comparable infrastructure businesses. That premium would be easier to defend if a new investment cycle was approaching, but current evidence points in the opposite direction.

Transgaz remains a strategically important company with resilient cash generation and stable operations, yet the next phase is likely to be characterised by normalised earnings, slower asset growth and fewer catalysts. The business itself appears healthy. The valuation leaves much less room for disappointment.

CD Projekt (DCR Poland): new expansion announcement adds momentum after a steady Q1

CD Projekt's Q1 results showed rather steady sales growth of its core franchises and the announcement of a new expansion for The Witcher 3, scheduled for 2027.

Revenue reached PLN 191m, up 6% from last year, helped by the inclusion of The Witcher 3 and Cyberpunk 2077 on Xbox Game Pass. The Witcher 3 passed a major milestone, surpassing 65 million copies sold since launch, an increase of five million in a year. Operating costs were broadly unchanged, aside from higher administrative spending, and EBIT came in at PLN 97m. A low effective tax rate lifted net profit to PLN 106m, slightly ahead of expectations. Investment in new game development remained high at PLN 180m, with additional developers joining projects across the portfolio. Net cash increased marginally to PLN 964m, supported by proceeds from the sale of the Gog.com platform.

During the results call, management addressed progress toward the 2023-2026 incentive targets, which require cumulative net profit of PLN 2bn. After the first quarter, PLN 414m remains to be achieved. Management expressed confidence in reaching the goal, citing the newly revealed Songs of the Past expansion and three additional projects in development, including one outside gaming. One smaller‑scale project is planned for release in 2026. The company did not provide formal guidance for the year, consistent with past practice, but highlighted the strength of its franchise pipeline as a key driver for the coming periods.

The announcement of Songs of the Past adds another layer to the release schedule ahead of The Witcher 4, which is still expected in the second half of 2027. The expansion should re‑engage the franchise’s large player base and maintain visibility for the series in the run‑up to the next mainline title. More details will be shared later in the summer. The company’s development spending and team expansion reflect a continued focus on building out both The Witcher and Cyberpunk universes, with multiple projects advancing in parallel.

The share price has corrected quite a bit in recent weeks. But with a rather stable first quarter, a growing development pipeline and a major expansion planned for 2027, the company enters the next stages of its cycle with a clearer view of its near‑term catalysts.

UNIQA (UQA Austria): Strong execution leaves little room for valuation upside

UNIQA delivered a strong start to 2026, with results comfortably ahead of market expectations and further evidence that the group's transformation over recent years continues to pay off.

Insurance revenues increased 7% to €1.9bn, supported by growth across all major business lines. Health insurance once again stood out, expanding by 13% and highlighting the strength of UNIQA's position in one of Austria's most attractive insurance niches. Life insurance revenues increased 11%, while non-life advanced 5%, producing a balanced growth profile across the portfolio. Operationally, the business remains in good shape. The technical result reached €210m, ahead of expectations despite a combined ratio of 91.0%, reflecting healthy underwriting discipline across the organisation.

Unlike many European insurers that have relied heavily on investment income to support earnings in recent years, UNIQA has spent considerable effort improving the quality of its underlying insurance operations. That work is becoming increasingly visible in the reported numbers. The company is now generating growth across multiple business lines while maintaining profitability metrics that remain competitive within the European insurance sector.

The biggest surprise in the quarter came from investment performance. Management had previously flagged a potential hit from market volatility linked to developments in the Middle East, leading investors to expect a relatively weak financial result. Instead, investment income proved far more resilient than anticipated. Net investment income rose 38% year-on-year to €151m, benefiting from a much lower level of realised and unrealised losses than seen in the comparable period last year. The financial result reached €29m, almost double market expectations, helping earnings before tax climb to €160m. Net profit increased 8% to €128m.

While these figures are undoubtedly encouraging, investors should avoid extrapolating first-quarter trends too aggressively. Insurance earnings are rarely linear through the year, and the upcoming quarters typically carry greater exposure to weather-related claims. Management therefore chose to leave full-year guidance unchanged, targeting earnings before tax of €540m to €570m. That decision appears sensible.

The challenge for the investment case is not operational execution. UNIQA continues to deliver solid results, maintains a very strong solvency position and has further strengthened its balance sheet through a recent €500m Tier 2 bond issuance completed on attractive terms.

The issue is valuation. The shares already trade at a premium to many European insurance peers despite offering a business profile that is not obviously superior. The combination of stable growth, healthy capitalisation and dependable earnings generation deserves recognition, but much of that quality is already reflected in the share price.

Investors looking for substantial upside may struggle to find it at current levels. The upcoming capital markets event later this year could provide additional clarity on medium-term ambitions, yet for now UNIQA looks like a company executing well without an obvious catalyst to justify a materially higher valuation. The business remains attractive. The stock appears fairly priced.

easyJet (EZJ UK): a takeover approach shines a light on a neglected sector

easyJet has spent much of the past year frustrating investors. Operationally, the company remains one of Europe's strongest short-haul airlines, yet the share price has moved in the opposite direction.

That disconnect explains why recent takeover speculation attracted so much attention. Castlelake's confirmation that it is evaluating a potential offer may ultimately lead nowhere, but the development is significant because it highlights how parts of the European airline sector are being valued. easyJet's market capitalisation has fallen to roughly £3bn despite owning a substantial fleet, holding valuable airport slots and maintaining one of the strongest balance sheets in the industry.

The stock has materially underperformed key rivals this year, creating an opening that private capital investors are unlikely to ignore. Even if no transaction emerges, the fact that a specialised aviation investor is studying the opportunity suggests that current valuations are drawing attention from buyers with deep sector knowledge.

Castlelake is not a typical financial sponsor arriving from outside the industry. The firm has spent years building expertise across aviation finance, leasing and airline restructurings. Its involvement in the restructuring of Scandinavian carrier SAS, investments in aviation-backed financing structures and previous discussions around other airline situations demonstrate familiarity with the sector's economics.

The timing also makes sense. easyJet recently reported a disappointing first-half performance, sentiment across European airlines remains cautious and investors continue to focus on cyclical concerns. Yet the underlying asset base remains substantial. At the end of the latest reporting period the company held approximately £4.7bn of cash and reported net cash of more than £400m. The owned fleet alone represents a significant source of value, while delivery positions stretching into the next decade provide strategic flexibility that would be difficult to replicate today. Those characteristics make easyJet very different from the highly leveraged airlines that have historically attracted distressed investors.

None of this means a transaction will be straightforward. Regulatory hurdles remain considerable in European aviation. Any buyer would need to ensure that traffic rights and ownership requirements are preserved across easyJet's core markets. The company's structure, with operating certificates in the UK, Austria and Switzerland, may provide flexibility, but it does not eliminate those challenges.

There is also the question of shareholder support. The Haji-Ioannou family continues to own a meaningful stake and would likely play an important role in any potential transaction. A serious bid would almost certainly require a significant premium to secure backing.

For investors, however, the bigger takeaway may have little to do with Castlelake itself. European airlines have demonstrated far greater resilience over recent years than many expected. Demand has recovered, balance sheets have improved and capacity remains relatively disciplined.

Despite that, valuations remain compressed. easyJet currently trades at levels that imply considerable scepticism about future earnings and industry conditions. Whether Castlelake proceeds or not, the interest itself suggests that parts of the market see considerably more value in these assets than public investors currently recognise.

Abivax (ABVX France): crazy share price action on positive data

Abivax has spent years trying to convince investors that obefazimod represents something genuinely different in inflammatory bowel disease. The latest Phase III maintenance data go a long way towards supporting that claim.

The ABTECT study delivered a clean set of results, with both the 25mg and 50mg doses achieving the primary endpoint by a wide margin. Clinical remission rates after 44 weeks reached just above 50% in both treatment arms, compared with roughly 10% for placebo. Just as important, every major secondary endpoint was achieved, including endoscopic remission, corticosteroid-free remission and sustained remission.

What makes the dataset particularly interesting is not simply the efficacy itself but the balance between efficacy and safety. Ulcerative colitis has become one of the most competitive therapeutic categories in biotechnology, with multiple biologics, oral therapies and emerging mechanisms all competing for market share. Strong efficacy alone is rarely enough. Physicians increasingly want treatments that can be used for extended periods without introducing complex monitoring requirements or meaningful safety concerns.

That is where obefazimod appears to be building a differentiated position. Across the 44-week maintenance period, the safety profile remained broadly stable, with no new signals emerging. Severe infections remained uncommon and there were no indications of some of the issues that investors have worried about with other immunomodulatory approaches. The mechanism itself, centred on miR-124 regulation, continues to look distinct from many competing therapies. This is importanmt because physicians are often reluctant to move all patients toward a single class of drugs, preferring a range of mechanisms that can be matched to different patient profiles and treatment histories.

The commercial discussion is now becoming more relevant than the scientific debate. Investors will naturally compare obefazimod with established therapies such as Rinvoq, Zeposia and newer anti-TL1A programmes currently moving through development. Direct comparisons between studies always require caution, but the latest results place Abivax firmly within that conversation. The convenience of a once-daily oral therapy is also important. Many patients prefer oral treatments over injections or infusions, provided efficacy remains competitive.

That all said, the share price nonetheless took a beating (~25%) as several cancer cases among treated patients (plus one on placebo) triggered panic among investors and raised regulatory uncertainty. Independent monitors saw no causal link, yet analysts now expect a real overhang as the FDA review approaches later this year.

Even so, the latest results materially strengthen the investment case, in our view, and the price action might actually push the company to consider selling sooner.

Laurent-Perrier (LPE France): taking market share while the industry slows

Laurent-Perrier's latest results highlight a characteristic that has defined the company for many years: it tends to perform best when conditions become more challenging.

The broader Champagne market contracted during 2025-26, yet Laurent-Perrier managed to grow volumes by 3.8%, taking share from both the overall market and the major Champagne houses segment. That achievement is particularly notable given the premium positioning of the brand. Premium categories have generally experienced softer demand across luxury goods over the past two years, yet Laurent-Perrier continued to attract consumers and distributors in key international markets. Growth was led by Europe and the rest of the world, compensating for weaker conditions in France. Export markets now account for more than 88% of sales, a figure that has steadily increased over time and reflects management's long-standing focus on international expansion. The company's premium cuvées, which represent more than 40% of sales, experienced some moderation in growth, but that trend mirrors developments across the wider prestige Champagne category rather than indicating any company-specific weakness.

The financial performance was equally solid. Higher grape costs created pressure on gross margins, which declined by 130 basis points during the year. Even so, operating profitability remained above 25%, a level that most beverage companies would struggle to achieve under favourable conditions. Careful cost management played an important role. Marketing expenditure remained tightly controlled and administrative costs were kept in check, allowing operating profit to continue moving higher despite inflationary pressures within the supply chain. Net profit increased 7%, helped by lower financing costs and a healthier balance sheet. One of the more interesting developments was the improvement in financial flexibility. Net debt declined to €208m despite continued investment in inventories, which reached more than €700m.

The company remains cautious, which is hardly surprising given the uncertain consumer backdrop and continued pressure on luxury spending in several regions. Management expects grape prices to remain elevated and there is a reasonable chance that permitted harvest yields will be reduced again. Those factors create natural limits on volume growth across the industry. Laurent-Perrier's response continues to focus on value rather than volume. The objective is not to maximise bottle shipments but to protect brand equity, pricing power and profitability. That strategy has worked exceptionally well over long periods.

And the latest results suggest it is still working today. Market share gains, stable premium positioning and margins above 25% are difficult to find elsewhere in the listed Champagne sector. The company will not deliver explosive growth, but it continues to demonstrate an ability to grow earnings in an industry that is currently struggling to do so. That combination of resilience, pricing discipline and financial strength explains why Laurent-Perrier continues to command attention despite operating in one of the more challenging areas of the European consumer sector.