Another AI pivot, alcohol and panic in private markets

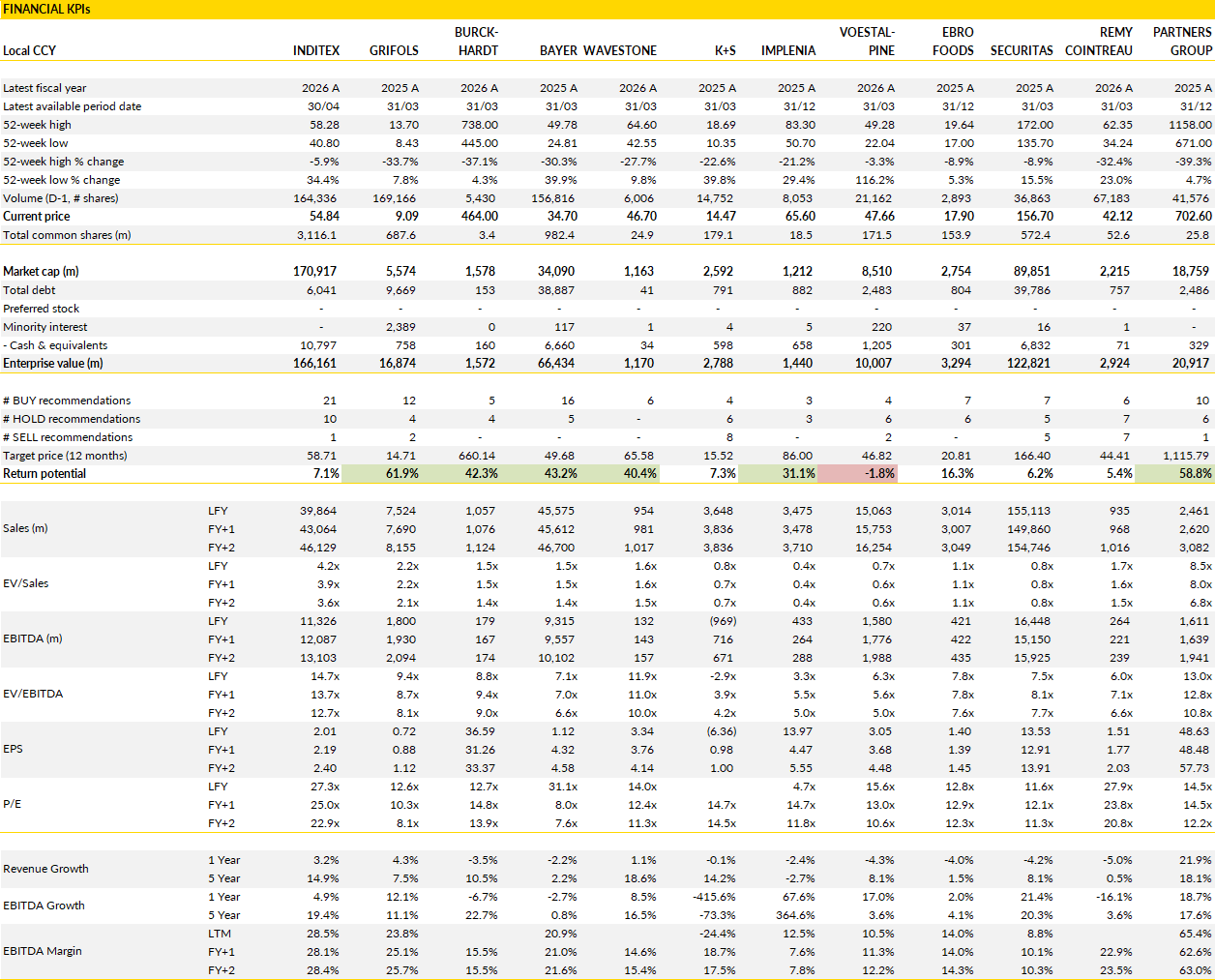

Inditex, Grifols, Burckhardt Compression, Bayer, Wavestone, K+S, Implenia, voestalpine, Ebro Foods, Securitas, Rémy Cointreau, Partners Group

At Lux Opes, we break down the latest company news into quick takes that get straight to the point - what happened, why it matters, and what to watch next.

We publish 2-4 times per week, depending on the news flow.

Financial KPIs

Inditex (ITX Spain): Still setting the pace in global apparel

Today's results were not particularly ahead of market expectations, yet the quality of the performance is difficult to ignore.

Q1 2026 revenue reached €8.75bn, growing 6% despite a meaningful currency headwind, while constant-currency growth approached 9%. More importantly, profitability continued to move in the right direction. Gross margin expanded by 70 basis points to 61.2%, operating profit increased 7% to €1.76bn, and the EBIT margin climbed above 20%. These results figures might appear routine for Inditex, but they are impressive considering a sector where many competitors are struggling to protect margins, clear excess inventory or generate meaningful growth. The company also reported 11.5% constant-currency sales growth between early May and early June. Part of that is due to calendar effects, but even after adjusting for timing differences, it shows a business that entered the second quarter with considerable momentum.

Inditex continues to generate growth without relying on aggressive discounting or large-scale store expansion. Management maintained its expectation of roughly 5% annual gross space growth, showing that the focus remains on productivity rather than footprint for its own sake. The combination of store optimisation, digital integration and disciplined inventory management continues to support margins. Gross profit grew faster than revenue during the quarter, something that has become increasingly common in recent years. Few retailers have managed to combine high-single-digit sales growth with operating margins around 20%.

Zara remains one of the strongest brands in global fashion, but the broader portfolio also contributes to performance across different customer segments and geographies. The result is a business that has been able to take market share through multiple economic cycles. Looking at the apparel sector today, the contrast with many peers is clear. Demand conditions remain uneven, consumer confidence is fragile in several regions, and promotional activity remains elevated across much of the industry. Inditex continues to grow despite those conditions.

The market's willingness to assign a premium valuation to the company is therefore understandable. Management left its full-year outlook unchanged, including guidance for gross margin stability and €2.3bn of capital expenditure. That conservative stance has been typical for the company. Consensus is unlikely to make major earnings revisions following these results, but these figures support confidence in existing forecasts. Revenue growth remains comfortably ahead of most global apparel retailers and margins continue to operate at levels that competitors can only aspire to.

The comparison with H&M is illustrative. Inditex is expected to grow materially faster while generating operating margins more than twice as high. Against that backdrop, a valuation close to its long-term average does not look excessive. The latest quarter simply provided another example of a retailer executing at a level that remains difficult for the rest of the industry to match.

Grifols (GRF Spain): ' Whoops'

The recent market noise around a supposed delay in Grifols’ Alpha‑1 program came from a Bloomberg update that incorrectly linked a timeline change to the company’s main Phase III study.

Grifols later clarified that SPARTA (its long‑running efficacy trial of IV Prolastin‑C in more than 300 patients) has not been rescheduled. The delay referenced in the cable appears tied to a separate, much smaller study comparing subcutaneous and intravenous Alpha‑1 formulations, focused on pharmacokinetics and safety rather than disease progression. That smaller trial sits outside the scope of SPARTA, which remains on track for a readout between late 2026 and early 2027.

SPARTA remains central to the franchise because Prolastin‑C, although already approved for weekly IV use in severe Alpha‑1 deficiency, still lacks definitive evidence on its impact on emphysema progression and exacerbations. The study is designed to address that gap by tracking lung‑density decline over several years. A clear result would strengthen the clinical case for augmentation therapy and support the higher‑dose strategy Grifols has been promoting. The Bloomberg confusion does not alter the expected timing of this key dataset.

While SPARTA progresses, the broader Alpha‑1 landscape is becoming more active. Existing IV therapies from CSL and Takeda/Kamada remain the closest alternatives today. The next meaningful entrant is likely Sanofi’s efdoralprin alfa, a recombinant therapy intended for dosing every three to four weeks, which could reach the market toward the end of the decade if development proceeds smoothly. Several early‑stage programmes (including base‑editing and RNA‑editing approaches from Beam, Wave and AIRNA) aim to address the genetic defect directly. These remain at an early stage and carry substantial development risk, but they point toward a pipeline that is gradually shifting away from traditional plasma‑derived products. Takeda and Arrowhead’s fazirsiran, meanwhile, is focused on Alpha‑1‑related liver disease and does not overlap with lung augmentation.

The clarification around SPARTA removes one source of uncertainty, but it does not change the broader picture for Grifols. The company faces a pivotal efficacy readout at a time when innovation in Alpha‑1 is accelerating and competitors are moving toward longer‑acting or recombinant formats. Combined with ongoing concerns around leverage, execution timing and weaker parts of the portfolio, the overall setup remains challenging.

Burckhardt Compression (BCHN Switzerland): Waiting for the next project cycle

Burckhardt Compression closed fiscal 2025 with decent results, yet challenges persist.

Revenue reached CHF 1.06bn and operating profit exceeded market expectations thanks to disciplined cost management and a strong contribution from the higher-margin Services division. EBIT rose to CHF 141m, equivalent to a margin of 13.3%, while earnings per share benefited from a favourable tax outcome. Services once again demonstrated why it has become such an important part of the business. Revenue was broadly stable, but profitability surprised positively, with margins comfortably above 24%. The segment continues to benefit from its installed base, long-term customer relationships and recurring maintenance activity. Systems also delivered solid margins despite a mixed market backdrop.

The challenge however remains in project activity, with order intake down to CHF 784m, well below market expectations and well below the level required to support growth in the near term. The weakness was concentrated in the Systems division, which remains the main driver of future revenue.

Management pointed to several factors including Swiss franc strength, delayed customer decisions and a less supportive macroeconomic environment. Those explanations are plausible, but the result is the same: visibility has deteriorated. The outlook for fiscal 2026 reflects that reality. Management expects revenue between CHF 900m and CHF 1.0bn and an EBIT margin around 12%, implying lower activity and lower profitability. Even more telling is the decision to maintain the medium-term objectives while removing the timetable previously attached to them. The company still sees a path toward CHF 1.2bn of revenue and margins between 12% and 15%, but no longer feels comfortable specifying when those targets can be reached. That shift says quite a bit about current conditions in the markets Burckhardt serves.

None of this changes the longer-term attractions of the business. Burckhardt remains exposed to structural investment themes across gas infrastructure, energy security, industrial processing and selected energy transition projects. The Services division provides a degree of earnings stability that many industrial equipment companies lack, and the acquisition of Fornovo broadens the group’s offering.

Even so, investors are likely to spend the next few quarters looking for signs that project activity is starting to recover. Management noted that customers are protecting cash, delaying spending decisions and operating equipment at lower utilisation levels. Those are not conditions that typically produce a rapid acceleration in order intake. The expectation for a stronger second half of fiscal 2026 suggests that management sees some improvement ahead, but evidence remains limited at this stage.

Until bookings begin to recover, the shares are likely to continue to reflect a market environment that has become noticeably less supportive.

Bayer (BAYN Germany): Legal milestones approach as settlement uncertainty drives volatility

Bayer’s share price has come under renewed pressure as investors reassess the likelihood that the company’s proposed settlement structure will receive court approval. The concerns stem from developments over the past week, when it became clear that the settlement could be reviewed not only by the Missouri District Court (which has already granted preliminary approval) but also by a federal court in San Francisco.

Although this information is not entirely new, the market reaction reflects heightened sensitivity ahead of several key legal dates. The next few weeks will bring a series of decisions that could influence sentiment, beginning with the 4 June deadline for plaintiffs to opt into the settlement, followed by an expected final approval ruling on 9 July, and a separate U.S. Supreme Court decision in the Durnell case anticipated around late June or early July.

The temporary involvement of the federal court in California has added complexity. Plaintiffs opposing the settlement appear to favour this venue, as the presiding judge there is viewed as more sceptical of similar settlement structures. Bayer maintains that the transfer is provisional and intends to challenge it, arguing that the majority of relevant cases are concentrated in Missouri and that the proceedings should remain under that court’s jurisdiction. The company continues to view Missouri as the most appropriate forum and believes the preliminary approval already granted there provides a solid foundation for the next steps.

These procedural developments come at a time when the company is attempting to draw a line under years of litigation. The coming weeks will likely bring elevated volatility as each legal milestone approaches. The outcome of the opt‑in period, the court’s final approval decision and the Supreme Court ruling all have the potential to influence expectations around the scale and timing of future liabilities. While none of these events directly change the company’s operational performance, they continue to shape investor perception and overshadow the broader fundamentals.

Despite the near‑term uncertainty, the longer‑term narrative remains centred on the gradual reduction of the legal overhang. As the key decisions unfold, the company aims to move closer to a more stable footing, allowing attention to shift back toward its underlying businesses. The next phase will depend on how the courts rule and whether the settlement structure can withstand the current challenges, but the sequence of upcoming decisions should provide greater clarity as the summer progresses.

Wavestone (WAVE France): Building the next chapter around AI and some consolidation

Wavestone’s latest results did not contain many surprises, yet they offered a useful snapshot of a consulting firm that seems to have navigated a difficult period better than many peers.

Revenue reached €954m, growing 1% organically, while recurring EBIT remained essentially unchanged at €120m, resulting in a margin of 12.6%. These numbers reflect a consulting market that remains hesitant, with clients continuing to scrutinise spending and large transformation projects moving forward at a measured pace. The more interesting element of the release came from cash generation. Free cash flow almost doubled to €119m, helped by favourable working capital movements and lower cash tax payments, pushing net cash above €120m. That leaves the company with a balance sheet that looks considerably stronger than many competitors.

Management remains careful when discussing the next twelve months. The outlook for fiscal 2026-27 points to only low single-digit organic growth and an operating margin around 13%. That is not the type of guidance investors would associate with a consulting sector entering a powerful recovery phase. The company also acknowledged that its previous ambition of reaching a 15% margin by 2027-28 is unlikely to be achieved within that timeframe.

Those comments reflect current market conditions more than company-specific issues. Across Europe, many organisations continue to postpone discretionary projects, particularly those linked to broader strategic transformation programmes. Against that backdrop, Wavestone appears focused on protecting profitability while positioning itself for the next cycle. The numbers suggest management expects improvement, but not a dramatic rebound.

The more interesting discussion concerns the period beyond the current slowdown. Wavestone used the results presentation to introduce its new "Lead The Shift" roadmap extending to 2030. The plan revolves around three themes: strengthening positions in higher-growth consulting segments, expanding internationally, and building a larger presence in AI-related services. Management is targeting revenue of €1.4bn by 2030, alongside margins of 14% to 16%. Geographic diversification plays a significant role in that ambition, with the DACH region and the US/UK expected to account for a much larger share of group activity. M&A will also remain central to the strategy, supported by roughly €800m of acquisition capacity.

Whether these ambitions are fully realised remains to be seen, but the direction is clear. Following a sharp decline in the share price over recent months, investors are being asked to look beyond a subdued near-term environment and focus on a company that still generates attractive margins, strong cash flow and retains meaningful capacity to reinvent itself through a combination of organic investment and acquisitions.

K+S AG (SDF Germany): Expanding its salt portfolio with a stable, higher‑margin business

K+S has agreed to acquire Qemetica Salt, a Polish producer focused on water‑treatment and food‑grade salt, for an enterprise value between €350m and €380m depending on performance milestones through 2027. Qemetica generated €125m in revenue and around €50m in EBITDA in 2025, giving it a margin close to 40%, far above the group’s average. The business has very limited exposure to de‑icing salt, with less than 10% of sales tied to weather‑dependent volumes. Most revenue comes from applications with steadier demand patterns, such as water treatment and food processing. The acquisition also broadens K+S’s footprint in Eastern Europe, where Qemetica generates more than half its sales across Poland and the Czech Republic.

The transaction includes an earn‑out of €30m linked to volume and pricing performance in 2026 and 2027. This structure reflects the need to normalise results after a strong start to 2026, particularly in de‑icing salt. K+S expects synergies from production, logistics and overhead consolidation, which could reach a high single‑digit to low double‑digit million‑euro level. Factoring in these synergies, the effective transaction multiple falls below 6x EBITDA. Qemetica’s capital‑expenditure needs are modest at around 5-6% of sales, leaving room for a solid free‑cash‑flow contribution estimated at €15-20m after financing.

K+S plans to fund the acquisition without issuing equity. With net financial debt expected to be around €14m at the end of 2025 and leverage projected at roughly 0.3-0.4x EBITDA on a pro‑forma basis for 2027, the balance sheet provides ample flexibility. The company is evaluating a mix of straight debt and hybrid instruments, with existing liquidity lines available if needed at closing. The transaction is expected to close in the first quarter of 2027.

The deal strengthens the company’s core salt operations by adding a business with higher margins, lower volatility and strong regional complementarity. Qemetica’s focus on stable end‑markets reduces exposure to weather‑driven swings, while its geographic position supports expansion in Eastern Europe. Integration should be manageable given the overlap in products and customers, and the synergy potential provides additional visibility on earnings contribution.

Implenia (IMPN Switzerland): Going for the next phase of European infrastructure spending

Implenia has spent the last several years reshaping itself from a traditional contractor into a more focused construction and services platform with higher margins, stronger cash generation and greater exposure to structurally attractive markets.

The latest strategy discussion with management suggests that process is still far from complete. The company outlined a framework that extends well beyond the current cycle, targeting revenue growth of as much as CHF 1bn during the first phase of the plan and an EBIT margin of 4.5% by the end of the decade. Those ambitions may not appear dramatic at first glance, but they would represent a meaningful improvement from the CHF 3.5bn revenue base and 4.0% EBIT margin delivered in 2025.

More importantly, management appears increasingly selective about where growth comes from. The emphasis is no longer on expanding volume across the board. Instead, the focus is on sectors where technical expertise, project complexity and barriers to entry allow for better economics. This is important because it reflects a business that is prioritising quality of revenue alongside growth.

One of the clearest examples is data centres. Although the segment currently represents less than 5% of the order book, management highlighted profitability levels that are comfortably above the group average. Demand across Europe continues to expand as cloud computing, AI infrastructure and digitalisation drive capacity requirements. Implenia already occupies a strong position in Switzerland and is working to broaden its reach in Germany and other regions.

The company is also expanding its capabilities in mechanical, electrical and plumbing services, allowing it to capture a larger share of project value. Data centres are only one piece of the puzzle. Tunnelling, energy infrastructure, healthcare facilities, research buildings and defence-related projects all represent sizeable markets where investment levels are expected to increase substantially over the coming years. Germany's infrastructure program could become an additional source of growth, although management expects any meaningful contribution to emerge from 2027 onwards rather than immediately. That timing is worth noting because it suggests the current opportunity set remains largely independent of political stimulus measures.

Management also pointed to the continued development of its Value Assurance process, which has steadily improved project selection and bidding discipline. Pre-calculated project margins have risen materially since the framvework was introduced, and artificial intelligence is increasingly being integrated into that process. Alongside internal improvements, acquisitions are expected to play a larger role. The company is looking at targeted deals that deepen its position along the construction value chain, particularly in planning, development, digital solutions and property management. Those areas typically require less capital and can generate more stable returns than traditional construction activities. Cash generation remains another priority, with management seeking further working capital improvements and reviewing capital-intensive assets across the portfolio.

The near-term impact of the growth investment program may weigh modestly on earnings, but the broader direction remains interesting. Implenia is entering a period where infrastructure investment across Europe appears set to expand, and the company is increasingly concentrated in parts of the market where technical expertise commands a premium. This provides a clearer path to margin expansion than was visible only a few years ago.

voestalpine (VOE Austria): Strong Q4 finish, steady guidance, but valuation now looks full

voestalpine closed its financial year with a stronger‑than‑expected fourth quarter, helped by solid execution across its divisions and tight control of working capital.

Group revenue came in at €3.9bn, slightly below last year, but EBITDA reached €448m, well ahead of expectations and lifting the quarterly margin to 11.4%. The Steel division delivered the largest contribution, supported by stable shipments and firmer margins. High Performance Metals benefited from restructuring measures, while Metal Engineering posted another resilient quarter with steady demand in rail and wire products. Free cash flow was a highlight: €537m for the full year, driven by a €311m reduction in working capital. Net financial debt fell to €1.3bn, reinforcing the balance sheet ahead of a capex‑heavy period.

For 2026-27, the company expects EBITDA between €1.6bn and €1.85bn, broadly in line with market expectations. The main swing factor for the year will be cash flow, which is set to decline meaningfully as investment peaks. Total capex is planned at around €1.15bn, including €400m for the greentec steel program. Working capital is also expected to absorb roughly €100m. As a result, free cash flow is guided at around €200m, well below the level achieved in 2025–26. The company proposed a dividend of €0.75 per share for the past year, reflecting the strong cash generation before the step‑up in investment.

The group continues to benefit from its positioning in more specialised and structurally healthier end‑markets than traditional European steelmakers. Exposure to rail infrastructure, aerospace, energy and high‑value engineering products provides a degree of resilience in a still‑soft macro environment. Its downstream integration and focus on higher‑grade steels also help cushion the impact of weaker commodity‑driven segments. The company’s measured approach to the green transition (with a gradual rollout of greentec steel rather than large‑scale hydrogen or DRI commitments) supports capital discipline during a period of elevated investment.

Even so, the share price has already captured much of this quality premium. After a strong run over the past year, the valuation now reflects the company’s strengths more fully, while the near‑term cash‑flow profile becomes more constrained by capex. voestalpine remains one of the better‑positioned names in the sector, but the risk and reward balance looks pretty even as the group enters a year shaped by heavy investment and only modest demand recovery.

Ebro Foods (EBRO Spain): Navigating turbulence while preparing the next growth phase

Ebro Foods is facing a considerably more complicated backdrop this year than the one investors had hoped not jsut long ago.

The message from management at the annual meeting was not exactly upbeat, but it also wasn't a warning that the business is deteriorating. Instead, the discussion centred on a collection of external pressures that are making operations more difficult across several markets. Trade policy uncertainty in the United States, continued disruption to global shipping routes, higher energy costs, geopolitical tensions in the Middle East and currency movements are all creating headwinds simultaneously. Management quantified part of the challenge, pointing to a potential €38m cost burden during 2026.

Against this, the fact that the company continues to target profitability improvement later in the year is noteworthy. The first quarter was affected by several temporary factors, including the sale of higher-cost inventory accumulated previously, weaker rice pricing and elevated logistics expenses. Those issues weighed on margins, but management expects conditions to become more favourable as the year progresses and older inventory works its way through the system.

Nonetheless, Ebro continues to invest despite the difficult operating environment. The group is pursuing two acquisitions with a combined value of roughly €50m, one focused on the US rice market and another linked to ingredients in Italy. Those transactions are not transformational individually, but they fit a long-standing pattern of disciplined bolt-on expansion. At the same time, Ebro is committing capital to categories where it sees stronger long-term growth. The new fresh pasta facility in Missouri represents an important step in expanding its presence in a segment that offers attractive growth potential in North America. The project combines the previously acquired manufacturing site with approximately $50m of additional investment and is expected to begin production during 2027. Closer to home, recently completed investments in Spain are starting to provide additional capacity and new product opportunities. Taken together, these initiatives suggest management remains focused on building the business beyond the current cycle instead of simply defending short-term profitability.

An important question now is on how quickly margins can recover. Rice markets have become unusually challenging, with lower global prices creating pressure across agricultural supply chains in both Europe and the United States. Management was particularly vocal about competitive dynamics in Europe, where imported Asian rice and the increasing influence of large retail buying groups are creating pricing pressure throughout the value chain. Those conditions are unlikely to disappear overnight.

Even so, Ebro retains several characteristics that have historically helped it navigate difficult environments. Its portfolio consists largely of established brands, it operates across multiple geographies and categories, and cash generation remains solid enough to support investment while maintaining shareholder returns. The annual dividend was left unchanged at €0.69 per share, reflecting management's confidence in the underlying financial profile despite current volatility.

The near-term outlook remains constrained by factors largely outside the company's control, particularly currencies, tariffs and logistics costs. For that reason, major earnings upgrades appear unlikely in the coming quarters. The longer-term picture, however, looks more balanced. Ebro is still investing, still expanding selected businesses and still generating the cash needed to support those ambitions. The challenge now is waiting for external conditions to become less hostile.

Securitas (SECUB Sweden): A different company than the market still seems to recognise

Securitas is increasingly being valued as if little has changed over the past decade, yet the company operating today bears limited resemblance to the labour-intensive guarding business that long defined the group.

The acquisition of Stanley Security marked a turning point. What was once predominantly a traditional manned-security provider has evolved into a broader security platform where technology, remote monitoring, electronic systems and integrated solutions account for a much larger share of revenue and profits. Ten years ago, guarding represented almost the entire business. Today, technology and solutions contribute roughly a third of sales and an even larger share of earnings.

This shift has practical consequences. These activities carry margins above 10%, require less labour, generate stronger returns and create cross-selling opportunities across a customer base that spans hundreds of thousands of sites globally. The strategy is not centred on replacing guards with technology. It is built around combining both, creating longer customer relationships and increasing revenue per client over time. The Stanley acquisition accelerated that process by several years and has given Securitas a position that few security companies can match at scale.

The financial profile has changed alongside the business mix. Operating margins spent much of the previous decade around 5%, a level that reflected the competitive nature of traditional guarding contracts. In 2025, adjusted EBIT margins reached 7.4%, including 8% during the second half of the year. That improvement did not come from a favourable economic backdrop. It came from contract repricing, portfolio clean-up, greater exposure to electronic security and tighter execution across North America and Europe. Cash generation has strengthened as well. Cash conversion has exceeded 80% for three consecutive years, comfortably above management's long-term targets. The acquisition of Stanley temporarily pushed leverage above 3x EBITDA, creating understandable concerns at the time, but those fears have largely disappeared. Net debt has fallen rapidly through internally generated cash flow and leverage now stands near 2x. Return on capital, which dropped sharply following the acquisition, is moving back toward levels that characterised the company before the deal.

The result is a business producing better margins, stronger cash generation and a healthier balance sheet than many investors appear willing to acknowledge.

Now an important question is how much further profitability can move. Management continues to talk about a long-term EBIT margin objective of 10%, while market expectations remain anchored around 8%. That gap explains much of the valuation discount. At present, Securitas trades below historical multiples despite operating with a more attractive business mix and a stronger balance sheet than it had before the Stanley transaction.

Investors remain cautious because the path from 8% to 10% is not yet fully mapped out. The Capital Markets Day in June could become relevant if management provides greater detail around timing, productivity initiatives and the contribution expected from technology-led services. Even without reaching 10%, the current valuation appears difficult to reconcile with the progress already achieved. The market continues to treat Securitas as a mature guarding company. Earnings, cash flow and business mix increasingly point to something else.

Rémy Cointreau (RCO France): Good brands, improving trends, but still waiting for a cleaner recovery

Just a few years ago, investors were willing to pay a premium for exposure to Cognac, attracted by strong pricing power, attractive margins and expanding demand from China and the United States. How times have changed.

The latest results show a business that remains profitable and financially sound, but one that is still working through the after-effects of inventory corrections, uneven consumer demand and shifting geographic trends. Organic sales were broadly stable during the past fiscal year, yet operating profit fell 24% and the operating margin slipped to 17.7%. The pressure came largely from mix, with higher-margin categories contributing less than in prior years, while foreign exchange and tariffs added further friction. Even so, the outcome was slightly better than expected. Earnings per share reached €1.71, ahead of market forecasts, and net debt increased only modestly to €690m. The balance sheet is not the problem. The issue is earnings momentum, which remains weaker than investors would like for a premium spirits company.

What makes the situation more nuanced is that several commercial indicators have started moving in the right direction. Rémy Martin is gaining market share in China despite the difficult backdrop for luxury consumption. Conditions in the United States have improved compared with the inventory-led downturn that weighed heavily on the category over the last two years. Travel retail has also begun recovering and management believes the business can double in size over the next three years.

These developments do not yet translate into rapid profit growth, but they do paint a different picture from the one reflected in recent earnings declines. Management expects fiscal 2026-27 to deliver a return to organic sales growth and a modest improvement in operating margins. That outlook broadly matches market expectations. The company appears comfortable discussing a gradual recovery but noticeably avoided setting new medium-term targets. Investors hoping for a detailed roadmap will need to wait until November, when management plans to present updated strategic objectives. The absence of those targets is understandable given the current environment, although it does little to improve confidence after several years of earnings pressure.

Another theme emerging inside the group is the effort to broaden the business beyond its traditional dependence on Cognac. Management wants faster growth from other categories, a larger presence in emerging markets and a more balanced geographic footprint. Dedicated teams have already been established to support expansion outside the United States and China, with an ambition to double the size of those emerging market operations over the next three years. That strategy reflects lessons learned during the recent downturn. Cognac remains an exceptional category when demand is strong, but concentration risk has become more visible.

Investors therefore face a business with high-quality brands, improving commercial trends and a recovery that appears underway, yet still lacking the visibility normally associated with premium consumer staples companies. The dividend reduction to €0.75 per share and the postponement of medium-term guidance both reinforce that reality. Rémy Cointreau no longer looks like a company in decline, but it has not yet reached the point where investors can confidently underwrite a sustained earnings acceleration.

Partners Group (PGHN Switzerland): The wealth machine is being tested for the first time

The appeal of the private markets industry over the past decade has been built on a simple assumption: bringing private equity, private credit and infrastructure products to wealthy individuals would create a vast and sticky source of capital. Partners Group became one of the biggest beneficiaries of that trend. Its evergreen structures allowed investors to access private markets without the traditional ten-year lock-up associated with institutional funds, opening a much larger addressable market.

But all comes to an end - or at least, it looks like. Withdrawal requests in several evergreen vehicles accelerated sharply during the second quarter, forcing the group to activate redemption limits in one fund and likely do the same in its flagship US vehicle. The immediate financial impact remains modest. The Global Value SICAV fund saw redemption requests of roughly $0.85bn, a small figure relative to the firm's overall assets under management.

The main point is that investors are now seeing the first meaningful stress test of the evergreen model during a period of weaker sentiment towards private assets.

The speed of the change is difficult to ignore. Annualised withdrawal rates implied by current requests reach roughly 40% in the Global Value SICAV fund and around 24% in the larger US vehicle. Those figures sit far above the approximately 10% annual redemption levels observed across the evergreen platform between 2023 and 2025. Management continues to highlight strong fundraising momentum and remains committed to its target of raising $26bn-$32bn this year.

This is important because fundraising and redemptions are now becoming two separate debates. The industry spent years proving it could gather capital from private wealth channels. The next challenge is demonstrating that this capital behaves differently from traditional retail money during periods of uncertainty. Recent activity suggests wealthy investors are acting more opportunistically than many asset managers had hoped. The assumption that evergreen investors would remain relatively stable through market volatility is no longer as clear-cut as it appeared twelve months ago.

The implications extend beyond Partners Group. One reason the company historically commanded a premium valuation was the perception that its product mix carried lower redemption risk than managers more exposed to private credit wealth products.

Recent developments blur that distinction. Management itself acknowledged that redemption pressure initially visible in private credit has started spreading into other asset classes, including private equity. That observation could become increasingly relevant for firms such as CVC and EQT, both of which have expanded their wealth-channel ambitions in recent years. The market reaction to Partners Group was severe, with the shares falling roughly 16% in a single session, but the move reflects concerns about future growth rather than current earnings.

The firm's overall platform remains substantial, fundraising remains healthy and the absolute level of withdrawals remains manageable. What has changed is investor confidence in one of the industry's most important growth narratives.