Photonics, firefighting and strong momentum

Soitec, Rosenbauer, PORR, Aroundtown, Capgemini, Stellantis, UBM Development, Ferrari, DEUTZ, Galenica, LDC, ASTA Energy Solutions

At Lux Opes, we break down the latest company news into quick takes that get straight to the point - what happened, why it matters, and what to watch next.

We publish 2-4 times per week, depending on the news flow.

We are moving our email sending to our custom domain. You might for a short period receive emails either from Ghost or Lux Opes.

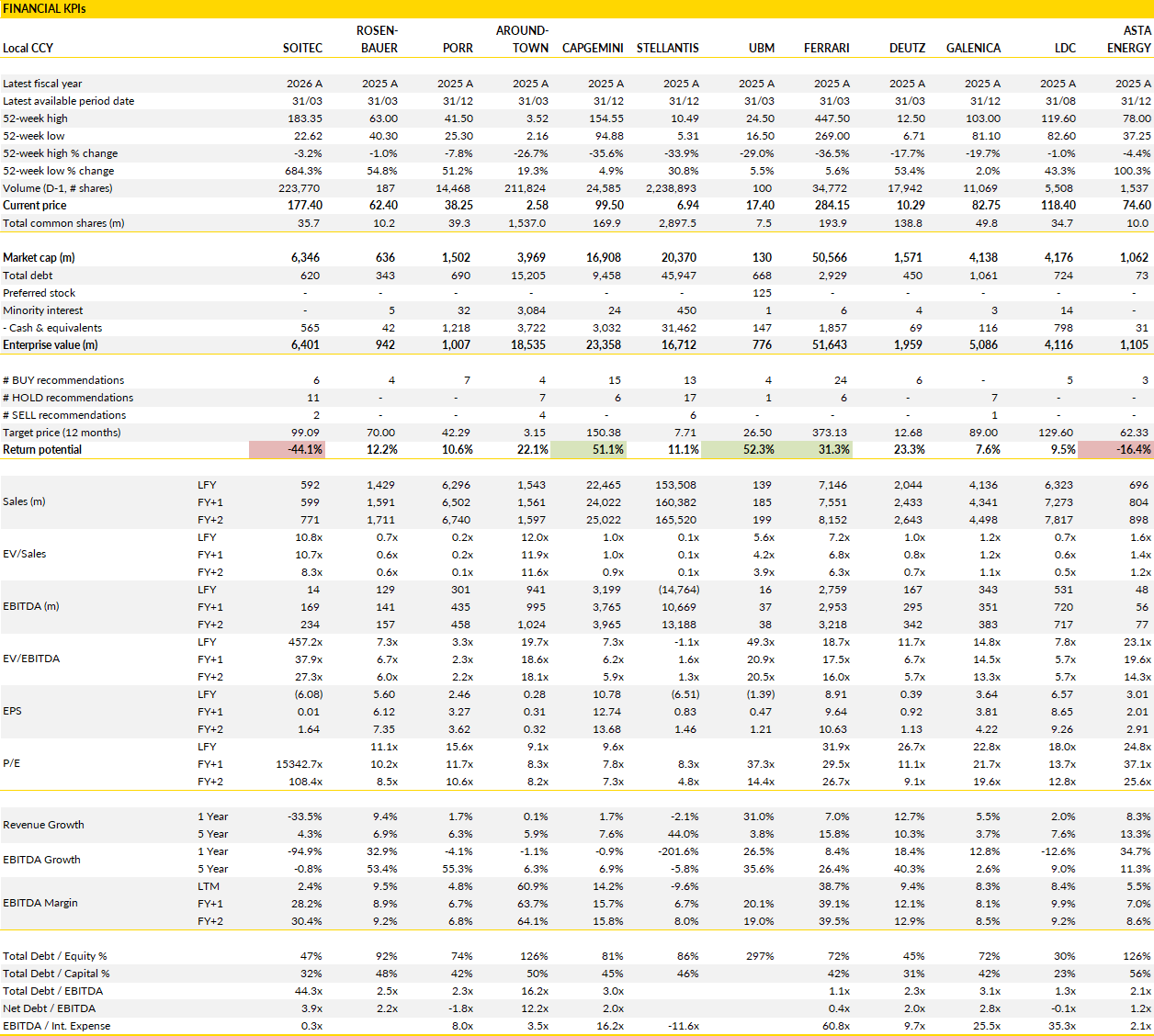

Financial KPIs

Soitec (SOI France): the downturn is ending, but the market may already be pricing the recovery

Soitec’s latest results showed two things at the same time. First, the operational pressure that crushed earnings over the past year. And second, that the company now appears to be moving beyond the worst part of the cycle.

Revenue collapsed by roughly one-third during FY2026 as the group faced a brutal combination of RF-SOI inventory corrections, weak automotive demand and significantly lower factory utilisation. EBITDA was cut roughly in half and reported net income turned negative for the first time in a decade. None of that was especially surprising after months of warnings across the semiconductor supply chain, but the scale of the reset still highlights how dependent Soitec remains on cyclical end markets despite the strong long-term technology positioning.

What matters more in the recent release was management’s confidence around the recovery path. Early signs increasingly suggest that the deep inventory correction in mobile and automotive markets is finally stabilising. Fab utilisation fell to only around 50% during the year, an unsustainably low level for a business with Soitec’s operating structure. Even a partial normalisation therefore creates substantial room for margin recovery over the next several quarters. The Q1 guidance pointing toward roughly 15% growth reinforces the idea that demand conditions are improving again, even if management itself cautions against extrapolating that pace too aggressively across the full year.

Photonics is increasingly becoming the centrepiece of the long-term investment case. The company’s legacy mobile exposure remains important, but investor attention has shifted sharply toward optical connectivity and AI infrastructure applications where Soitec sees accelerating demand. The group already generated more than $100m of photonics revenue in FY2026 and is now increasing capex plans to expand production capacity faster than initially expected. That shift is strategically important because it changes how investors think about the company’s future growth profile. Photonics potentially offers structurally stronger growth, higher barriers to entry and less dependence on smartphone replacement cycles.

The issue is that the market has moved exceptionally quickly in pricing that opportunity. The stock has surged dramatically this year as investors increasingly positioned Soitec as a critical enabler of next-generation AI infrastructure. This is of course besides AI infra being popularised on social platforms. The problem with that type of rerating is that expectations start running ahead of operational reality. Management itself still appears to be dealing with manufacturing ramp challenges and scaling constraints in photonics, while the broader recovery in traditional RF-SOI and automotive markets remains fragile. The company therefore sits in an unusual position where long-term optimism around AI-linked demand is colliding with still relatively weak near-term fundamentals.

Cash flow was actually one of the more encouraging elements of the release. Despite the earnings collapse, free cash flow came in materially ahead of market expectations thanks to sharply lower capex and improved working capital management. The balance sheet therefore remains healthy, with leverage still very modest for a semiconductor company coming out of a severe downcycle. That gives management room to continue investing aggressively in photonics and next-generation technologies without facing financing pressure.

So the broader issue for investors is valuation. The stock is now trading at levels that already assume a very powerful recovery over the next several years, while consensus expectations for FY2027 and beyond still look ambitious given the operational volatility seen recently.

Soitec undoubtedly owns differentiated technology and remains strategically important in several fast-growing semiconductor niches. However, investors are no longer simply paying for recovery from a cyclical trough. They are increasingly paying upfront for leadership in photonics and AI infrastructure markets that are still only beginning to scale commercially.

Rosenbauer (ROS Austria): firefighting demand is turning into a multi-year earnings story

Rosenbauer has clearly entered a period where operational execution starts to dominate the equity story again. Only a few years ago the debate centred on balance sheet pressure, supply chain disruption and uneven profitability. Today the conversation is shifting toward backlog conversion, margin recovery and cash generation.

The order book (~€2.35bn) provides unusually strong visibility for an industrial company of this size and reflects a supportive backdrop across municipal, industrial and airport firefighting markets. Demand remains structurally healthy as fleets across Europe and North America continue to age, while civil protection spending is rising again after years of underinvestment. At the same time, geopolitical tensions and climate-related fire risks are keeping emergency infrastructure spending high on political agendas.

Rosenbauer is therefore entering the next few years with strong underlying demand already secured, while production bottlenecks that constrained deliveries during the past cycle are gradually easing. This allows management to focus more heavily on manufacturing efficiency, pricing discipline and product mix instead of simply fighting component shortages and working capital stress.

What is impressive is how quickly profitability is rebuilding. The group is already guiding toward an EBIT margin above 6% this year, but the trajectory underneath the guidance appears stronger than the market still assumes. Q1 showed that operational leverage is returning as throughput improves and legacy inefficiencies fade from the system. The absence of several one-off charges that weighed on prior periods should also help the margin profile normalize faster over the coming quarters. Meanwhile, service, maintenance and spare parts are becoming a larger contributor to the business mix, adding a more stable and higher-margin revenue stream on top of vehicle sales. Rosenbauer is also broadening its international exposure into regions where firefighting infrastructure spending is accelerating, even if those markets can carry slightly different pricing dynamics.

The key point is that scale is finally starting to work again. After several years where inflation, supply chain disruptions and delayed projects compressed returns, the operating model now looks positioned for a much cleaner earnings conversion cycle. Reaching the long-discussed 7% margin threshold by 2027 no longer looks especially aggressive if current execution levels are maintained. That would bring Rosenbauer back toward profitability levels the market has not associated with the company for well over a decade.

The balance sheet is also becoming less of an overhang, which materially changes the investment case. Stronger earnings and improved cash conversion are expected to continue reducing leverage over the next few years, with net debt trending toward much more comfortable territory by 2028. That matters because Rosenbauer historically struggled to attract a premium valuation during periods where investors worried about financing risk and operational volatility at the same time. The current setup is different. Investors are now looking at a company with improving returns on capital, a visible backlog, healthier free cash flow dynamics and a business operating in structurally attractive end markets.

Even after the strong share price performance over the last year, the valuation still does not fully reflect the possibility that Rosenbauer is transitioning into a higher-quality industrial profile with more durable margins and stronger cash generation. The biggest challenge now is probably credibility, and not so much demand. The company still needs to prove that the operational consistency seen recently can be sustained across a full cycle. If that succeeds, the rerating story likely has further room to run.

PORR (POS Austria): backlog momentum keeps building even before the cycle fully improves

PORR’s first quarter did not contain any major surprises, but the underlying message from the release was still constructive because the company continues to build visibility at a time when parts of the European construction market remain subdued.

Output growth of 2% and only modest EBIT expansion were largely expected given the weather disruptions in Austria and Germany and the still uneven pace of recovery in residential activity. The more important development came from the order side, where PORR delivered another strong quarter and pushed backlog above the €10bn mark for the first time in the company’s history. That milestone changes the discussion around the stock because it reinforces the idea that PORR is no longer relying on a short-term macro rebound to grow earnings.

Infrastructure spending, rail projects, energy investments and civil engineering continue to provide enough demand to offset weakness in more cyclical areas of the market. Germany, which has been a concern for the broader construction sector, actually delivered particularly strong order intake thanks to transport infrastructure and specialist civil engineering projects. Poland also remained a major contributor as public infrastructure activity accelerated again. The backlog therefore continues to shift toward larger and more visible projects, improving revenue quality and execution visibility over the coming years.

The regional mix also says quite a lot about where the company currently sits in the cycle. Austria and Germany still showed softer operational activity in Q1, partly because of weather and partly because certain project ramp-ups remain delayed, but Eastern Europe and infrastructure-heavy operations continue to compensate. This is notable because it supports margins during a period where many investors are still worried about pricing pressure and weaker residential demand in Central Europe.

PORR has spent the past few years repositioning itself toward technically more complex infrastructure and civil engineering work where competition is lower and pricing discipline is better. The current backlog composition increasingly reflects that strategy. The market also appears to underestimate how much operational leverage can still come through once activity levels normalize further. Even relatively modest revenue growth could drive stronger-than-expected earnings progression given the improvements already made in project selection, procurement and execution discipline. Management’s guidance for moderate growth and higher margins therefore still looks achievable without requiring an aggressive macro recovery scenario. Importantly, the company did not need to change its tone after Q1 because current trends already support the existing outlook.

Another important element is balance sheet quality, which continues to improve gradually in the background. Construction investors historically tend to discount companies heavily when leverage, working capital swings and project risk all move in the wrong direction simultaneously. PORR is moving away from that profile. Cash generation has become more stable, order visibility is stronger and the quality of the backlog appears better than during previous cycles.

The investment case therefore revolves around steady execution and margin expansion. Valuation still does not fully reflect that shift. The market continues to apply fairly conservative multiples to European contractors despite a much healthier infrastructure spending backdrop across several core markets. PORR now combines visible backlog growth, improving operational discipline and exposure to structural infrastructure demand trends at a valuation that still assumes a far weaker earnings trajectory than the current order book suggests.

Aroundtown (AT1 Germany): steady operations

Aroundtown delivered an 'ok' first quarter, with net rental income of €296.7m, up 1% from last year and slightly above the prior period. Like‑for‑like rental growth reached 3%, supported by increases of 1.5% in offices, 3.7% in residential and 4% in hotels, while vacancy held at 7.5%. Adjusted EBITDA came in at €250.2m, broadly unchanged from last year as rental growth was offset by higher operating costs and a lower contribution from equity‑accounted investments. FFO I reached €70.2m, down 8% year‑on‑year but above internal expectations, with FFO I per share stable at €0.07 thanks to the ongoing share buyback programme. EPRA NTA per share rose to €8.00, helped by retained earnings and the absence of portfolio revaluations this quarter.

The balance sheet remained broadly stable, with IFRS LTV at 42% and EPRA LTV at 59%, both slightly higher than at year‑end but still below the company’s medium‑term ceiling. Net debt to EBITDA increased marginally to around 11.1x, and interest coverage fell to 3.4x, reflecting the impact of higher financing costs. The company continued to execute its disposal strategy, closing €27m of asset sales in the quarter at a small premium to book value. A further €300m of disposals were signed year‑to‑date, and €270m closed after the quarter, supporting efforts to strengthen liquidity and reduce leverage.

The company raised its full‑year FFO I guidance to €275-305m, while keeping its FFO I per share target unchanged at €0.24-0.27. The stable per‑share guidance reflects several moving parts: a lower minority contribution following the increase in its stake in GCP to 81.5%, reduced perpetual note coupons, and the impact of the €250m share buyback program, which is now over 90% complete and executed at a significant discount (almost 70%). The buyback is expected to have a more visible effect on per‑share metrics in the coming quarters as the reduced share count flows through.

Operational trends in the first quarter were consistent with expectations, with steady rental growth and stable occupancy across the portfolio. The main areas to watch remain financing costs and leverage, which continue to weigh on profitability relative to some peers. The near‑completion of the buyback program should support per‑share performance later in the year, while upcoming portfolio revaluations in the second quarter will provide a clearer view of asset values in the current market environment.

Capgemini (CAP France): AI turning the model back to growth?

Capgemini’s latest strategic update was effectively an attempt to reposition the company from being viewed as a mature IT services player into a business sitting directly in the middle of the enterprise AI investment cycle.

One fo the most interesting parts of the Investor Day presentation was not the medium-term targets themselves, but the way management framed the next phase of demand. Capgemini increasingly sees AI as a broad architectural reset across enterprise technology stacks, operations and product development, creating a much larger addressable market than traditional digital transformation projects. This is interesting because investors have spent the last two years questioning whether generative AI would ultimately compress demand for consultants and outsourcers.

Capgemini is arguing the opposite: enterprises now need partners capable of redesigning workflows, rebuilding legacy infrastructure, integrating AI systems into existing environments and managing governance around increasingly autonomous software agents. The company believes this creates a multi-year investment cycle extending far beyond simple software implementation. Its positioning also looks relatively strong compared with smaller peers because Capgemini can combine consulting, engineering, cloud migration, operations and industry-specific expertise under one platform. The acquisitions completed over recent years, particularly Altran and WNS, now fit much more clearly into that strategy than they perhaps did when originally announced.

The medium-term targets themselves landed roughly as expected, in our view. Revenue ambitions came in ahead of market expectations, especially on the organic side, while margin ambitions were marginally softer. The market probably focuses too heavily on the second point. A slight difference in long-term margin assumptions matters less if the underlying growth profile improves structurally, particularly in a sector where investors have spent several years worrying about slowing demand and pricing pressure. Capgemini is effectively saying that the company can sustain a higher level of organic growth through AI-related spending, sovereign technology investment and digital transformation tied to industrial automation.

The company also appears increasingly comfortable discussing AI monetisation directly, which is an important shift. Until recently, many European IT services firms mainly talked about productivity gains internally. Capgemini is now openly framing AI as a revenue driver across application modernisation, software engineering, operational workflows and enterprise process redesign. The acceleration of agentic AI discussions is also important because this expands the opportunity beyond traditional IT budgets into broader operational spending pools. If that thesis proves correct, Capgemini’s end markets become materially larger than investors currently model.

One last point worth noting is that the company continues to execute from a position of financial strength despite the heavy investment cycle underway across the industry. Free cash flow guidance did not surprise positively, but Capgemini has historically guided conservatively on cash generation and still retains significant optionality for acquisitions.

The broader setup for the stock also looks different than it did twelve or eighteen months ago. Back then, the market narrative around European IT services centred on slowing discretionary spending, weak consulting demand and pressure on hiring utilisation. Today the discussion is increasingly moving toward how quickly large enterprises will scale AI deployment across mission-critical systems. Capgemini is one of the few European players with enough scale, client relationships and technical breadth to participate meaningfully across multiple layers of that transition.

The valuation still does not fully reflect that possibility. Even after the recent rebound in technology shares, Capgemini continues to trade at levels that imply relatively muted long-term growth for a company now positioning itself directly inside one of the largest enterprise technology investment cycles of the past decade.

Stellantis (STLAM Italy): a new strategy is easy to present, much harder to execute

Stellantis used its recent capital markets day to draw a clear line under the Tavares era and present a much more pragmatic strategy for the remainder of the decade.

The new management team is openly acknowledging that the group can no longer rely on aggressive pricing, relentless cost cutting and oversized margin ambitions as the sole pillars of the equity story. Instead, the focus is shifting toward rebuilding competitiveness in North America, simplifying execution, improving market coverage and leaning more heavily on partnerships to reduce capital intensity.

In theory, the plan addresses many of the weaknesses investors have been highlighting over the past two years. The issue is that credibility now matters far more than 'just' ambition. The group is coming off a period marked by deteriorating operational momentum, weaker cash generation and increasing concern around brand positioning, particularly in the US. The market therefore appears unwilling to fully reward long-term targets until there is concrete evidence that execution is stabilising. That caution is understandable because several elements of the new roadmap still rely on fairly optimistic assumptions regarding market conditions, pricing discipline and the ability to deliver very large cost savings without sacrificing competitiveness.

North America remains the centrepiece of the recovery plan and effectively determines whether the broader turnaround works. Management is targeting a meaningful rebound in volumes, margins and market share over the next several years through a much broader product rollout, stronger affordability positioning and an expansion of the finance business. Ram and Jeep are expected to drive a large part of that recovery, supported by a renewed push into lower-priced vehicles and electrified offerings such as EREV models.

The underlying logic is not unreasonable. Stellantis still owns several globally recognised brands and maintains a scale advantage in many segments. The challenge is that the competitive environment has become materially tougher than during the post-pandemic pricing boom that previously boosted profitability across the industry. US consumers are increasingly price sensitive, Chinese competition continues to intensify globally and the transition toward software-heavy vehicle platforms remains expensive and operationally complex. Europe arguably looks even more difficult. Stellantis is targeting growth there as well despite sluggish end markets, persistent overcapacity and a still-fragmented electric vehicle landscape. Planned factory restructuring, capacity reductions and partnerships with Chinese groups may improve efficiency over time, but they also highlight how much work remains to reposition the European business structurally. The company is effectively trying to redesign large parts of its industrial footprint while simultaneously accelerating product launches and maintaining pricing discipline.

The financial framework also raises important questions. Stellantis is targeting more than €6bn of cost savings by 2028, with most of the expected margin recovery relying directly on those efficiencies flowing into profits. Historically, the automotive sector rarely manages to preserve that level of savings entirely because competition typically forces part of the gains back into pricing, incentives or product investments. That risk feels particularly relevant now given how crowded the market is becoming across both EV and combustion segments. The company is also increasingly relying on partnerships across software, platforms and autonomous driving technologies, which may reduce upfront investment requirements but could dilute long-term economic benefits.

From a valuation perspective, the stock undoubtedly looks inexpensive, but the market is clearly demanding a substantial discount until the company proves that operational consistency can return. Cash generation is expected to remain weak for several more years and balance sheet concerns have not disappeared completely. Stellantis therefore remains a story where the upside case depends heavily on execution improving quarter after quarter.

The strategic direction now looks more coherent than it did a year ago. The next phase is about proving it.

UBM Development (UBS Austria): higher revenue and a return to positive EBT

UBM Development reported a solid start to the year, with first‑quarter revenue rising 11% to €31.6m, supported by steady apartment sales and a better contribution from office projects, including the sale of property shares in Warsaw. The company sold 88 residential units in the quarter, broadly in line with recent periods. EBT reached €0.3m, marking the fourth consecutive positive result and a clear improvement from the loss recorded a year earlier, helped by stronger at‑equity contributions and lower material costs. Net profit after hybrid interest remained negative at €‑2.1m, reflecting ongoing financing and hybrid‑related charges. NAV per share excluding hybrids was stable at €30.5, and the cash position strengthened to €168m, up from €118m at year‑end.

The balance sheet continued to improve, with net debt excluding hybrids falling to €484m from €528m in the previous quarter. The equity ratio stood at 34%, comfortably within the company’s target range of 30-35%. Cost discipline also remained a focus, with headcount reduced by a further 8% since the end of 2025. While the quarter did not match the strong fourth‑quarter performance, the year‑on‑year improvement in revenue and EBT highlights a more stable operating environment compared with early 2025, when the company faced higher costs and weaker contributions from joint ventures.

UBM has not yet issued financial guidance for 2026, citing continued macroeconomic uncertainty and limited visibility on the timing of transactions. The company expects housing demand and pricing momentum to remain supportive, and 2026 is set to mark the first phase of its portfolio rotation under the affordable housing strategy. This shift is intended to rebalance the portfolio toward more resilient segments while reducing exposure to higher‑risk developments. The pace of this transition will depend on market conditions, permitting timelines and the availability of capital for new projects.

The first‑quarter results show a continuation of the gradual recovery seen over the past year, with higher revenue, improved contributions from joint ventures and a return to positive EBT. Seasonal effects explain the step‑down from the strong fourth quarter, and the absence of full‑year guidance reflects the uncertain backdrop with limited visibility (hence the current valuation).

Ferrari (RACE Italy): Luce raises bigger questions than just electrification

Ferrari’s recent Luce event appears to have reinforced many of the concerns that initially emerged after the first images were released.

The company clearly wanted this model to represent a break from the past and a symbolic step into a more electrified future, but the reaction so far suggests that the execution may be creating more debate than excitement. The Luce moves sharply away from Ferrari’s traditional design language, with a crossover-style profile and a more practical five-seat configuration that many long-time Ferrari followers do not immediately associate with the brand.

What also stands out is the apparent influence of external design studio LoveFrom, linked to Jony Ive and Marc Newson, through Ferrari chairman John Elkann. Ferrari itself shared very little on commercial expectations, volumes or profitability assumptions. Pricing is confirmed around €550k before options, while management emphasised that the Luce is meant to attract a new customer profile instead of simply serving the existing Ferrari base. Importantly, Ferrari also indicated that buying the Luce will not become a prerequisite for gaining access to future limited-edition models, which likely reflects awareness that residual value concerns around hybrid and electric Ferraris are already becoming more visible.

The broader issue is that the Luce arrives at a difficult moment for high-end electric vehicles. Luxury EV demand has cooled materially across the sector and several premium manufacturers have already struggled with radical EV-specific design strategies that alienated parts of their traditional customer base. Ferrari is now trying to navigate that same transition while simultaneously protecting one of the strongest luxury brands in the world. That balancing act is becoming increasingly delicate. Hybrid models like the SF90 and 296 are already seeing higher depreciation trends than many investors previously expected, which is feeding a wider debate around how Ferrari maintains exclusivity, scarcity and pricing power in a progressively electrified market.

Therefore, even if Luce only represents a relatively small share of deliveries over the next few years, it could influence perceptions around Ferrari’s long-term strategic direction and brand identity. The design itself remains highly divisive, but feedback around the interior appears considerably more positive, with some believing Ferrari may actually influence broader luxury automotive interior design trends if execution proves successful. Still, at this stage, the market seems far more focused on the risks than the opportunities.

What makes the situation more complicated is that Ferrari’s short-term operating performance remains extremely strong. Demand across the core business continues to hold up well, the order book still stretches roughly 18 months ahead and mix remains highly supportive thanks in part to the ramp-up of the F80. Financially, Ferrari therefore continues to execute at a very high level. The problem is that the Luce introduces a layer of uncertainty that investors are not accustomed to assigning to Ferrari. The recent sharp share price reaction reflects concerns extending well beyond the economics of a single model launch. There is risk if the project ultimately fails to resonate with customers and linked to Ferrari’s growing internal investment in EV technologies.

DEUTZ (DEZ Germany): expanding in LatAm

Deutz is moving deeper into the Latin American energy market with the purchase of Maxi Trust Power, a Brazilian producer of generator systems ranging from smaller industrial units to large‑scale power plants.

The company has a strong position in Brazil and across the region, giving Deutz immediate access to a broad customer base in a market where demand for decentralised energy solutions is rising quickly. Deutz plans to link Maxi Trust Power’s local reach with the engineering capabilities it gained through the earlier acquisition of Frerk Aggregatebau. Together, these businesses are expected to strengthen Deutz’s offering in areas such as data‑centre power infrastructure, which is expanding rapidly in Brazil and neighbouring countries. The acquisition also ties into Deutz’s ambitions in the US, where it already operates through Blue Star Power Systems but lacks a presence in higher‑end emergency power systems.

The deal is a moderate but meaningful addition to the group. Maxi Trust Power is expected to contribute around €40m in annual revenue once consolidated, with profitability broadly in line with the margins Deutz already generates in its Energy Solutions division. The purchase price sits in the mid‑double‑digit million range and is scheduled to be paid at closing in the second quarter of 2026. Deutz intends to fund the transaction from its existing balance‑sheet resources, which remain solid and leave room for further strategic investments. The company’s leverage stood at roughly 1.7x net debt to EBITDA at the end of the first quarter, giving it flexibility to absorb acquisitions without compromising financial stability.

This move fits directly into Deutz’s long‑term plan to scale its energy business. The company aims to lift revenue in this segment from about €170m in 2025 to roughly €500m by 2030, driven by a mix of organic growth and targeted acquisitions. Maxi Trust Power adds both geographic breadth and technical capability, strengthening Deutz’s position in a market where customers increasingly seek reliable, decentralised power solutions. The combination of local manufacturing, engineering expertise and a broader product range should create opportunities across multiple regions and customer groups.

By adding another specialised energy company to its portfolio, Deutz continues to build out the structure needed to support its Dual+ strategy. The acquisition broadens its footprint in a fast‑growing region, deepens its capabilities in power‑generation systems and positions the group to benefit from rising demand in sectors such as data centres and industrial backup power. The company now enters the next phase of its energy expansion with a larger network, a more complete offering and the financial capacity to continue pursuing similar opportunities.

Galenica (GALE Switzerland): pharmacy momentum offsets softer consumer health trends

Galenica opened 2026 with a relatively strong trading update after a quite muted second half last year.

Sales for the first four months reached CHF 1.41bn, up 7% year-on-year and modestly ahead of consensus forecasts. The strongest contribution came from the Products & Care division, where pharmacy activity remained healthy across Switzerland. Prescription medicines continued growing well, GLP-1 demand stayed elevated and the Puravita integration added additional support to reported growth. Pharmacy sales rose 7%, while the broader Swiss pharmacy market expanded at a slower pace, indicating additional market share gains during the period. Management also highlighted continued strength in prescription-driven categories, which helped offset weaker demand in more seasonal consumer healthcare products.

The update was encouraging because the first months of the year were not helped by a strong cold and flu season. In previous years, those categories often provided a temporary boost to over-the-counter sales. This year, the opposite happened, yet the group still delivered growth above the upper end of its full-year guidance range. Logistics & IT also developed steadily, with wholesale activity broadly matching the underlying pharmaceutical market in Switzerland.

The weaker parts of the portfolio were largely concentrated in Products & Brands. Revenue there declined 13%, mainly because of lower international Perskindol inventories and softer demand for pain relief and cold-related products in Switzerland. Verfora also had a slower start to the year. Those categories are currently facing more difficult comparisons and weaker seasonal demand patterns, and management was careful not to overstate the strength of the overall release because of that. Even so, other activities inside the group continued progressing well. Services & Production grew 9%, while the Diagnostics business contributed CHF 41m following consolidation. HCI Solutions also continued expanding rapidly, with CDS checks rising 73%.

The mix inside the business is therefore gradually shifting toward healthcare services, prescription exposure and infrastructure-related activities with steadier demand patterns. That gives Galenica a more stable earnings profile than traditional consumer healthcare companies that remain heavily dependent on seasonal OTC demand. It also helps explain why management remains comfortable reiterating its full-year EBIT growth guidance despite softer conditions in some consumer categories.

Guidance for 2026 was left unchanged at 5-7% sales growth and 6-8% EBIT growth, alongside a dividend at least in line with the prior year. That stance looks sensible. The first four months were clearly solid, but part of the growth still reflects acquisition effects and easier comparisons in certain areas. The current pace is therefore unlikely to continue unchanged through the full year.

Even so, the publication should help confidence recover after recent share price weakness. Galenica continues to execute well operationally, pharmacy market share is moving in the right direction and prescription demand remains healthy across the Swiss market.

The shares already trade on a valuation that reflects the defensive quality of the business, so the release probably does not change the longer-term valuation debate materially. Still, Galenica’s combination of predictable cash generation, healthcare exposure and steady operational delivery should continue attracting interest.

LDC (LOUP France): nice results!

LDC closed the 2025-26 year with results that much exceeded market expectations, driven by stronger margins and solid contributions across most business lines.

EBITDA rose to €720m, a 40% increase, supported by improved profitability in the International division and steady progress in French Poultry. Operating profit reached €427m, lifting the margin to 5.9%. In France, poultry activities benefited from the delayed pass‑through of price increases, which continued to support margins through the year. EBIT in this segment reached €291.4m, with a margin of 6.2%, while the upstream business saw a slight decline in earnings due to cost pressures. International operations delivered a sharp improvement, with EBIT rising to €100.6m as acquisitions and resilient consumption offset higher prices. Convenience food also strengthened, helped by a larger contribution from Pierre Martinet. Net profit increased by 32% to €321m, while net cash fell to €178.7m following recent acquisitions.

For the current year, the group is targeting sales above €7.7bn and an operating margin above 5.5%. The company has already secured price increases in France at the start of the year, with around 3% in poultry and 1-1.5% in convenience food. These adjustments should help support volumes, particularly as the Marie brand returns to shelves in the ready‑meals category. The guidance reflects the impact of ongoing geopolitical and cost‑related pressures, especially in fuel, raw materials and packaging, but the company expects the combination of pricing, operational improvements and recent acquisitions to sustain momentum. Consensus will have to be adjusted to reflect the stronger‑than‑expected finish of the year and the early visibility on pricing for the new financial year.

LDC also outlined its ambitions for 2030-31, aiming to reach €10bn in sales and €550m in EBIT. The plan assumes balanced growth across the portfolio, with French Poultry expected to reach €5bn in revenue, International activities to double to €3bn, and Convenience Food to reach €1.5bn. The upstream segment is set to play a larger strategic role, with a target of more than €800m in sales, including €500m from eggs, reinforcing the group’s control over its supply chain. This long‑term roadmap highlights the company’s intention to expand capacity, strengthen its geographic footprint and continue acquiring businesses that complement its core operations.

The latest results confirm that LDC is entering the new financial year with stronger fundamentals, better margins and a clearer view of its medium‑term trajectory. The combination of operational discipline, recent acquisitions and supportive pricing in key categories provides a solid base for the next phase of growth.

ASTA Energy Solutions (1AST Germany): strong pricing and utilisation drive a solid start after the IPO

ASTA opened 2026 with a stronger quarter than expected, particularly on the operational metrics that investors are currently watching most closely.

Reported sales rose to €196m, but the more relevant figure for the business model remains net-value sales, which strips out copper price effects and gives a cleaner picture of underlying activity. On that basis, Q1 came in at €46m, well ahead of expectations and showing that customer demand remained healthy across the group’s core cable and conductor markets. The operational leverage in the quarter was also notable. Adjusted EBITDA reached €17m, materially above forecasts, with margins improving both against reported sales and net-value sales.

The company again pointed to high production utilisation, favourable pricing conditions and continued customer demand support. Those comments fit with the tone management already adopted after the FY2025 results and with the additional customer agreements signed in recent months. The market has clearly started pricing in a stronger earnings trajectory since the IPO, with the shares already up sharply over the past month, but Q1 still came in ahead of where expectations stood operationally.

The quarter also gave another indication that ASTA’s business mix is currently moving through a favourable phase. Net-value sales growth translated efficiently into EBITDA, suggesting pricing discipline remained firm and manufacturing utilisation stayed high across the production footprint. EBIT reached almost €12m and EPS broadly matched expectations despite IPO-related one-offs during the quarter.

Management left full-year guidance unchanged at more than €790m of sales, net-value sales of at least €170m and EBITDA between €55m and €59m. That was expected given the guidance was only introduced recently, but investors will probably focus more on the implied trajectory inside the range. During the previous conference call, management already sounded comfortable with the upper end of the EBITDA guidance corridor, and the Q1 delivery does little to challenge that view.

The broader backdrop for electrification-related infrastructure spending remains supportive. Demand linked to grid investments, industrial applications and energy infrastructure has continued holding up well across Europe, helping support pricing and capacity utilisation levels throughout the sector.

The main area where investors may remain more cautious is cash flow quality. The company highlighted a positive internal free cash flow measure, but that definition excludes working capital movements. Reported operating cash flow was negative during the quarter because of inventory and working capital build-up linked partly to higher activity levels and partly to copper price movements. Capex was also relatively low in Q1 compared with what some investors may have expected for the year. That means future quarters will probably carry higher investment spending if management wants to maintain current utilisation rates and support further growth. Even so, the publication should still be viewed positively overall. The operational performance was strong, margins were ahead of expectations and demand commentary stayed constructive.

The discussion is now more on valuation after the strong share price performance since listing. Multiples have expanded quickly and the stock no longer screens cheaply on near-term numbers. Even so, if current pricing conditions and utilisation rates persist through the rest of 2026, earnings expectations could continue moving higher over the coming quarters.