Hyperscaling, cars and AI defence

Centiel, Trigano, DO & CO, Deutz, Temenos, Diagnostic Medical Systems, Volvo, LPP, Figeac Aéro, Safran

At Lux Opes, we break down company news into quick takes that get straight to the point - what happened, why it matters, and what to watch next.

We publish 2-4 times per week, depending on the news flow.

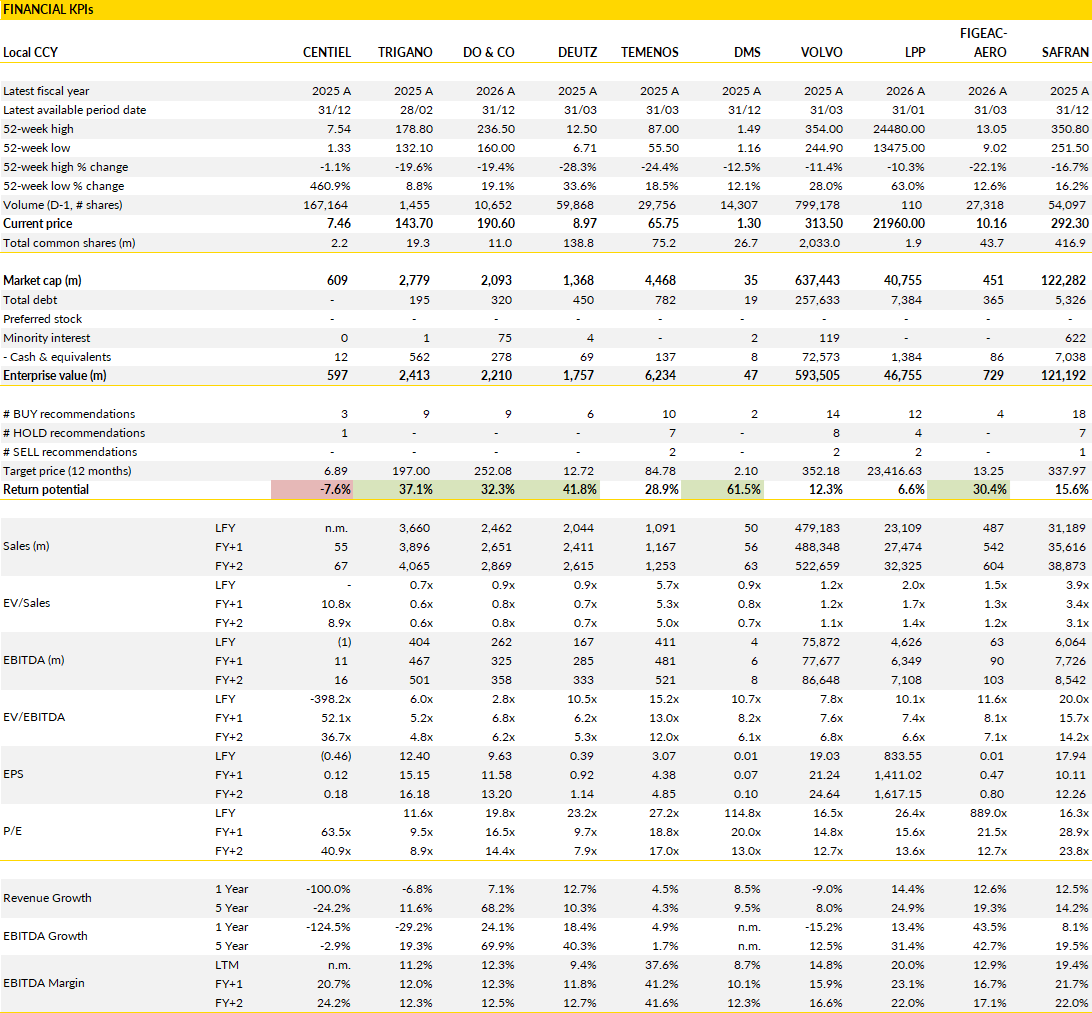

Financial KPIs

Centiel (CNTL Switzerland): A faster route into the world’s largest UPS market

Centiel has spent the past few years building a strong position in high-end uninterruptible power supply systems, with much of the investment case centred on steady expansion across Europe and selected international markets.

That said, the latest announcement changes that. The multi-year distribution agreement with Neo Critical Power has secured a strategic distribution agreement targeting the US data centre market, including both colocation operators and hyperscalers. Instead of building a local organisation from scratch, Centiel is partnering with industry veterans who already possess customer relationships, project access and field-service capabilities. This approach lowers execution risk and accelerates market entry at a time when demand for critical power infrastructure remains exceptionally strong. The agreement introduces Centiel to an addressable market that is several times larger than its existing footprint and provides access to some of the fastest-growing segments of digital infrastructure.

The timing is notable because it arrives much earlier than many expected. Until now, the assumption was that Centiel would focus on expanding its existing geographic presence before tackling the US market. Instead, management has found a way to participate without committing substantial capital to a direct buildout. The company expects an initial contribution of roughly CHF 10m-15m of revenue this year, with the longer-term framework agreement pointing to substantially larger volumes if execution goes according to plan.

That has implications for overall growth expectations. Prior assumptions were built around annual revenue growth of roughly 20%. Adding a meaningful US contribution could push that figure significantly higher over the next few years. Capacity expansion will be required, and management has already indicated that production and staffing will be increased to support anticipated demand. There will almost certainly be some near-term costs attached to that ramp-up, but the underlying economics remain attractive given the company's existing margin profile and manufacturing base.

What makes the development particularly interesting is the quality of the end market. Hyperscale and colocation data centres continue to invest heavily in power infrastructure as AI workloads, cloud computing and digitalisation drive electricity requirements higher. UPS systems are not discretionary purchases in this environment. Reliability is critical, and operators are generally willing to pay for proven technology. Centiel still needs to complete UL certification, which remains an important milestone before large-scale commercial deployment can begin. That process is expected during the second half of the year and will be closely watched.

Even with that hurdle still ahead, the announcement materially strengthens the growth story. The company is entering the largest market in its industry through a partnership structure that limits financial risk while preserving upside. For a business that was already growing rapidly, the prospect of adding a sizeable US revenue stream changes the scale of the opportunity. The next important checkpoint will come with the half-year results (in August), where investors are likely to look for updated medium-term growth targets and more detail on how management plans to support the expected increase in demand.

Trigano (TRI France): A pause in demand does not change the long-term picture

Trigano enjoyed a nice recovery last year, but 2026 is increasingly shaping up as a year of 'consolidation'. And Trigano's upcoming third-quarter sales update is likely to reflect that trend.

The company entered the year with solid momentum, posting first-half revenue growth of more than 6% and benefiting from healthy demand across its motorhome operations. Registrations across Europe remained supportive, helping Trigano convert a strong order environment into growth. But conditions have become less straightforward during recent months. Consumer confidence has been affected by geopolitical tensions, economic uncertainty and a more cautious spending environment across several European markets. Germany and France, two of the group's most important regions, have recently shown weaker registration trends, suggesting buyers are taking longer before committing to large discretionary purchases.

This softer market does not necessarily imply a (large) deterioration in fundamentals. Trigano remains the dominant player in a fragmented European market and continues to benefit from structural factors that have supported demand for years. The appeal of flexible travel, the ageing demographic profile of many customers and relatively low penetration rates in several countries remain intact. Recent comments from dealers indicate that activity in used vehicles and parts of the French distribution network has slowed, although conditions appear healthier in the UK. Industry data from competitors point in a similar direction. Volumes are still growing, but the pace is no longer as strong as it was earlier in the cycle.

Another area worth watching is input costs. Raw materials and transportation have clearly become more volatile again, although management currently appears comfortable that supplier price increases remain manageable. Chassis costs represent a meaningful portion of the group's cost base, and current indications suggest pricing pressure there remains limited. As a result, price increases for the next selling season are expected to stay modest.

Consensus has been moving down to reflect this, though the larger issue is timing. We struggle to identify a near-term catalyst that would change sentiment while macroeconomic uncertainty remains elevated, and so does the market. Indeed, the valuation has fallen to levels rarely associated with a market leader that continues to generate healthy profitability and cash flow. Trigano now trades at a substantial discount to its own history (over 30% on an EV/EBIT basis) despite retaining the same competitive advantages that helped it build its position over decades.

The next few quarters may lack excitement if customers remain cautious, but the current share price increasingly assumes a far weaker outcome than the operating performance suggests.

DO & CO (DOC Austria): Premium positioning keeps delivering

DO & CO closed its fiscal year with another strong quarter, extending a run that has been separating the company from many businesses exposed to travel and hospitality spending.

Revenue reached €594m in the fourth quarter, up 13% yoy, while EBIT climbed 11% to €49m. What makes the result noteworthy is that it was achieved during a period with disruptions in the Middle East, including the cancellation of Formula 1 events and operational challenges for airline customers. The airline catering division, which is the backbone of the group, grew sales by more than 11% yoy and delivered close to €40m of EBIT. Event catering expanded even faster, with revenue rising 43%, while restaurants, lounges and hotels continued to contribute steady growth. For the year, the business generated revenue of €2.46bn and EBIT of €212m, comfortably within management’s guidance despite a far from supportive operating environment.

The key feature remains its positioning at the premium end of the market. DO & CO is not competing primarily on price. Its customer base includes flagship airline contracts, major sporting events and premium hospitality venues where service quality carries greater weight than marginal cost differences. This has become increasingly important as inflation, labour shortages and geopolitical disruptions have affected the broader catering industry. Airlines continue to invest in premium passenger offerings, particularly on long-haul routes, and that plays directly into DO & CO. The company has also demonstrated an ability to win and retain large contracts while expanding existing relationships. So growth is coming from both higher passenger volumes and increased spending per passenger, ic what you want to see.

And management expects the positive trajectory to continue. The guidance is deliberately broad (hsd growth and >flat operating margins), but recent momentum has not faded. Market expectations currently point to another year of revenue growth alongside stable to slightly improving margins. This seems achievable given the combination of ongoing travel demand, contract wins and a growing contribution from higher-margin activities. Investors will naturally watch developments in aviation and global travel patterns, particularly if geopolitical tensions intensify further.

Even so, the latest results suggest a business capable of absorbing temporary disruptions without derailing growth, that is, less cyclical vs the past.

DEUTZ AG (DEZ Germany): Group transformation gains pace under the Dual+ strategy

Deutz recently completed the acquisition of Maxi Trust Power, a Brazilian producer of gas and diesel generators and a leading supplier across Latin America. The deal adds roughly €40m of annual sales at a low double‑digit adjusted EBIT margin, consistent with the company’s existing energy business.

While the financial impact on group metrics is limited, the strategic fit is significant. Deutz plans to combine Maxi Trust Power’s strong local presence with the engineering capabilities of Frerk Aggregatebau, acquired earlier, creating opportunities in the fast‑growing data‑center market in Brazil and the wider region. The acquisition also broadens the platform for a future push into the US, where Deutz already operates through Blue Star Power Systems but lacks high‑end emergency power solutions. The company aims to grow its energy‑related revenues from €170m in 2025 to around €500m by 2030 through both organic expansion and further acquisitions.

Management flagged that current trading remains strong, so the company is heading into Q2 2026 with solid momentum. Deutz is benefiting from healthy market conditions, strong order intake, and ongoing efficiency measures. Consensus is seeing roughly 20% yoy sales growth in the quarter, with adjusted EBIT nearly doubling and margins improving meaningfully. Order intake should rise by more than 30%, implying a book‑to‑bill ratio slightly above one. Free cash flow is also expected to improve sharply from the prior year, reflecting better profitability and operational discipline.

In short, Deutz appears on track to meet its full‑year 2026 targets. The company continues to guide for sales between €2.3bn and €2.5bn and an adjusted EBIT margin of 6.5-8.0%. Free cash flow is expected to reach the high double‑digit millions. The first half of the year supports this trajectory, with performance so far aligning with the midpoint of the guidance ranges.

However, management acknowledges that persistent geopolitical tensions and higher‑than‑expected input costs, particularly energy, could weigh on the second half. These risks could lead to slightly lower sales and EBIT assumptions for the year, though the company still appears positioned to deliver results around the midpoint or slightly above within its stated ranges.

Temenos (TEMN Switzerland): A targeted wealth management acquisition adds another layer

Temenos has spent the past few years rebuilding credibility around execution, product development and cloud adoption. The recent acquisition of additiv does not materially change that, but it does strengthen an area with attractive long-term growth.

Additiv operates a cloud-native platform focused on wealth management and digital onboarding, serving around 30 clients across Europe, the Middle East and Asia-Pacific. The business has built a reputation for rapid implementation times, extensive API connectivity and strong customer retention. In practical terms, Temenos is buying software that sits above core banking systems and helps financial institutions manage customer journeys, onboarding processes and investment workflows.

The attraction? Wealth management remains one of the fastest-growing areas of financial services, particularly in emerging markets where rising household wealth is expanding the addressable client base. Temenos already had exposure to the segment, but primarily through larger private banking clients. Additiv broadens that reach towards the mass affluent market, an area receiving increasing attention from banks and financial institutions globally.

The industrial logic here is more important than near-term financial contribution. Management expects the transaction to have only a marginal effect on ARR and subscription revenue this year while remaining neutral for earnings and cash flow. Cost synergies are unlikely to be significant because additiv will continue operating with its existing management team and organisational structure.

The opportunity instead comes from combining customer relationships and expanding product capabilities. Temenos gains additional functionality around wealth management workflows and onboarding, while additiv gains access to a much larger installed customer base. The acquisition also provides another building block for Temenos' broader AI ambitions. Additiv has developed orchestration tools that help coordinate interactions between banking systems, digital channels and third-party applications. As financial institutions increasingly look to automate client-facing and operational processes, those capabilities become more valuable. The deal therefore fits within a wider trend across enterprise software, where workflow automation and specialised AI functionality are becoming embedded within existing platforms rather than sold as standalone products.

The financial commitment appears manageable. Although terms have not been disclosed, available information suggests a relatively modest transaction size. Management expects leverage to remain comfortably within its target range (between 1.0-1.5x) and has indicated that shareholder returns, including buybacks, should not be affected.

That is probably why the market reaction has been muted. Investors are note changing their view on Temenos because of a single bolt-on acquisition generating perhaps €15m-25m of annual revenue. The larger investment case remains centred on organic growth, cloud migration, recurring revenue expansion and execution consistency. Additiv adds capabilities in an attractive niche, strengthens Temenos' position in wealth management and provides another avenue for cross-selling into existing clients.

None of those factors are likely to drive earnings upgrades immediately. They do, however, support management's objective of building a broader financial software platform with deeper customer relationships and a larger share of client technology spending over time.

Diagnostic Medical Systems (ALDMS France): Regulatory approval granted for Onyx

DMS received MDR certification for its new ONYX mobile radiology system, clearing the final regulatory hurdle before commercial launch in Europe.

First deliveries are planned for Q3 2026. ONYX is central to the group’s move upmarket under the MC2 project and incorporates several advanced features, including a carbon‑nanotube X‑ray tube that reduces overall weight, a zero‑gravity arm, a proprietary X‑Tech Cell lithium‑ion battery, and ADAM software designed to enhance image quality while lowering radiation exposure. Along its own distribution channels, the company also intends to offer the system through white‑label agreements with industrial partners.

The approval is an important milestone in the group’s strategy. Although the certification was expected, it removes the main regulatory uncertainty surrounding the launch and allows the commercial phase to begin. ONYX is positioned as a key growth driver for the radiology division, which accounts for nearly 80% of group revenues, and the next steps will focus on securing initial orders, scaling deliveries, and assessing the contribution of potential white‑label partnerships that could accelerate international expansion.

With the regulatory process now complete, the shift is now to execution. The company’s ability to ramp up production, convert interest into firm contracts, and leverage its partner network will determine how quickly ONYX contributes to growth. And expectations are high. The product’s technological positioning and lighter design are intended to differentiate it in a competitive market, and the certification now enables DMS to demonstrate these advantages directly to customers.

The launch also reinforces the broader direction of moving toward higher‑value equipment and expanding the group’s presence in advanced radiology solutions. The coming quarters are important, providing clearer visibility on adoption patterns, delivery pace, and the extent to which ONYX can support the group’s medium‑term ambitions.

Volvo (VOLVB Sweden): New growth avenues emerge, but the market already knows the story

Volvo’s capital markets day was not particularly exciting, but it did provide a useful look at how management sees the business evolving through the end of the decade.

The focus remains on gaining share in heavy trucks, particularly in North America, where its ambition remains considerably higher than its current position. Alongside that, management spent considerable time discussing areas that barely featured in the Volvo investment case a few years ago. Penta, autonomous transport and selected construction equipment markets are becoming increasingly important contributors to future growth plans. None of these activities are large enough to transform the group overnight, but together they show a business gradually broadening its earnings base beyond the traditional truck cycle. Management also sounded constructive on current demand conditions, with no evidence that customers are stepping back despite ongoing economic and geopolitical uncertainty.

The most interesting development may be the increasing relevance of businesses that sit outside Volvo’s core truck franchise. Penta is benefiting from several attractive themes at once. Data centre infrastructure continues to expand rapidly, while demand from industrial and marine applications remains healthy. Management believes revenue in the division can double over time, which would make it a far more meaningful contributor than it is today. Autonomous trucking is another area moving from concept to commercial reality. Volvo expects initial deployments in the United States next year, followed by a larger rollout as fleets become established. Construction equipment offers another source of expansion, supported by infrastructure investment, mining activity and quarrying projects. These opportunities are genuine and should help support growth over the coming decade, although the financial contribution remains relatively modest compared with the size of Volvo’s existing operations.

Volvo remains one of the strongest industrial businesses in Europe, with leading market positions, healthy profitability and a long track record of disciplined execution. The issue however is valuation.

Much of the operational improvement achieved in recent years is already reflected in the share price. Management acknowledged some inflationary pressure entering the second quarter, particularly around logistics costs, although there are also offsetting factors from recovering volumes and pricing initiatives. Consensus expectations already assume continued earnings progress, leaving less room for positive surprises than at some competitors. That helps explain why investors looking for cyclical recovery exposure are increasingly drawn toward names such as Daimler Truck or TRATON, where earnings expectations remain lower and valuation multiples leave more scope for upside.

LPP (LPP Poland): While profitability impresses, Sinsay’s performance is still short of the mark

We believe LPP is set to report very strong operating profitability for Q1 2026, helped by favourable currency movements, disciplined pricing, and tight cost control. We won't be surprised to see doublt-digit revenue growth, 58-59% gross margins, and sharp EBITDA growth, closing in on PLN 1,4bn, with the margin lifting to over 25% from roughly 19% a year earlier. The strength of the Polish zloty against the US dollar provided a meaningful boost, given the mismatch between revenue and sourcing currencies. Despite this, sales growth fell short of internal plans due to unusually cold weather in February and April, which held back demand.

LPP is pushing ahead with its ambition to integrate more technology into its operations. The company is adopting AI tools across trend analysis, product content creation, e‑commerce features such as virtual try‑on, demand forecasting, customer service, and logistics, where thousands of robots already support fulfilment. While these initiatives mirror what many competitors are doing, they show that the company intends to keep pace with broader industry shifts and embed more automation into its processes.

Also, Sinsay, the group’s largest and fastest‑growing brand, continues to struggle. Like‑for‑like sales dropped almost 7% in Q1, following smaller declines through most of last year, and this dragged the group’s overall LFL performance into negative territory. Heritage brands managed modest growth, but Sinsay’s weak quarter reflects ongoing adjustments to its assortment, particularly in non‑garment categories. With the brand now accounting for more than half of group sales, its performance remains a key swing factor, and the latest results suggest that further refinement is needed.

For the full year, LPP’s revenue target of PLN 28–29bn implies growth above 20%, broadly in line with current trends. The company’s guided ranges for gross margin and EBITDA margin are consistent with market expectations, and profitability is set to remain high before easing slightly in 2027. Longer term, margins are expected to stabilise within a narrower band (over 21%) as the business grows and normalises.

Figeac Aéro (FGA France): Cash generation opens the next chapter of expansion

Figeac Aéro FY results show revenue reaching €487m, roughly in line with market expectations, while underlying EBITDA increased 13% to €78.6m. The margin improvement was modest on paper, but the underlying operational trend was encouraging. Higher Airbus A320 and LEAP engine production rates continued to support volumes, while the Mexican operations reached breakeven during the final quarter of the year after several years of work. A fire at the Aulnat facility and adverse currency movements created headwinds, yet profitability still moved higher.

The most notable figure, however, was cash generation. Adjusted free cash flow reached €36m despite nearly €47m of capital expenditure. Inventory discipline, customer advances and tighter working capital management allowed the company to reduce net debt and bring leverage down from 3.9x to ~3.4x EBITDA. For a business that historically carried quite the heavy balance-sheet, this is interesting.

But the next phase will require more investment. Management is asking investors to accept lower near-term free cash flow in exchange for faster growth opportunities. Over the next two years, an additional €20m-30m will be allocated across core aerospace programs, defence activities and selected acquisitions.

The immediate reaction may be concern that Figeac is returning to the aggressive investment habits that characterised parts of the 2010s. The context today though looks very different. Aircraft production rates continue to recover, supply chains remain constrained and defence spending is rising across Europe. Those conditions create opportunities for suppliers capable of expanding capacity and taking market share. Management appears aware of the mistakes that can accompany rapid expansion. New projects are being screened against relatively demanding return thresholds (vs history), with expected payback periods of three to four years and profitability targets above the group’s medium-term margin ambitions. The objective is growth that lifts earnings quality.

The medium-term outlook remains centred on operational leverage. Management maintained its target of more than €100m of EBITDA by fiscal 2027-28 after guiding to €86m-94m for the current year. This would represent a substantial increase from current levels and reflects both higher production volumes and a healthier operating structure. Defence could become a more important contributor than in the past, providing some diversification away from commercial aerospace cycles.

There is also a corporate angle that remains difficult to ignore. Founder Jean-Claude Maillard has indicated his intention to pursue a sale process and is reportedly moving closer to selecting advisers. With aerospace assets remaining scarce and industry consolidation continuing, that possibility remains part of the broader investment case.

Even without it, the valuation appears disconnected from the company’s earnings path, with the numbers increasingly point to a business generating cash, reducing debt and investing from a position of strength rather than necessity.

Safran (SAF France): Defence electronics emerges

Safran recently highlighted how defence electronics is now approaching €2bn of annual revenue, growing at a pace rarely associated with a company of Safran’s scale.

Revenue in the activity expanded at a 17% annual rate between 2022 and 2025, helped by a sharp increase in production of systems such as the AASM Hammer precision-guided weapon. Order intake continues to run well ahead of revenue, with a book-to-bill ratio of 1.6x and orders rising 60% last year. European rearmament is clearly supportive, but the opportunity extends beyond budget increases. Modern conflicts require larger quantities of precision systems, navigation equipment, intelligence capabilities and electronic warfare tools. Those trends favour suppliers that can manufacture at scale while maintaining technological depth.

What stands out today is the breadth of Safran’s positioning. No dependence on a single platform, customer or weapons program. Navigation systems, optronics, missile seekers, artillery fire-control systems, intelligence gathering and counter-drone technologies all sit within the portfolio. Management has spent years building these positions through a combination of internal development and targeted acquisitions. Critical technologies are brought in-house where possible, international partnerships are developed to access local markets and products are designed to work across multiple platforms rather than being tied to a specific defence contractor. This flexibility becomes increasingly valuable as procurement patterns evolve and new players enter the defence ecosystem. The recent €50m investment in Germany reflects that approach, as does the group’s expanding presence in regions such as India and the Middle East.

The acquisition of Preligens, now operating as Safran.AI, provides another example of how management is building capabilities around emerging technologies rather than simply reacting to them. Revenue has increased from roughly €28m in 2023 to around €75m today, profitability has been achieved and the business has expanded beyond satellite image analysis into broader intelligence applications.

Artificial intelligence is becoming embedded across defence systems, surveillance networks and decision-support tools, creating opportunities that did not exist a few years ago. Safran is attempting to position itself at the centre of that development. None of this changes the reality that aerospace remains the main earnings driver, and investors continue to value the company accordingly.

The recent share-price weakness linked to concerns over higher fuel prices and airline demand has improved the valuation somewhat, but the market still assigns relatively little value to the possibility that defence becomes a much larger contributor over the next decade. Defence electronics is no longer a niche activity inside Safran.