Drugs, more photonics and a lot of deals

Air France-KLM, M6, Epiroc, Intesa Sanpaolo, Soitec, Fastned, Agrana, Rémy Cointreau, UCB

At Lux Opes, we break down the latest company news into quick takes that get straight to the point - what happened, why it matters, and what to watch next.

We publish 2-4 times per week, depending on the news flow.

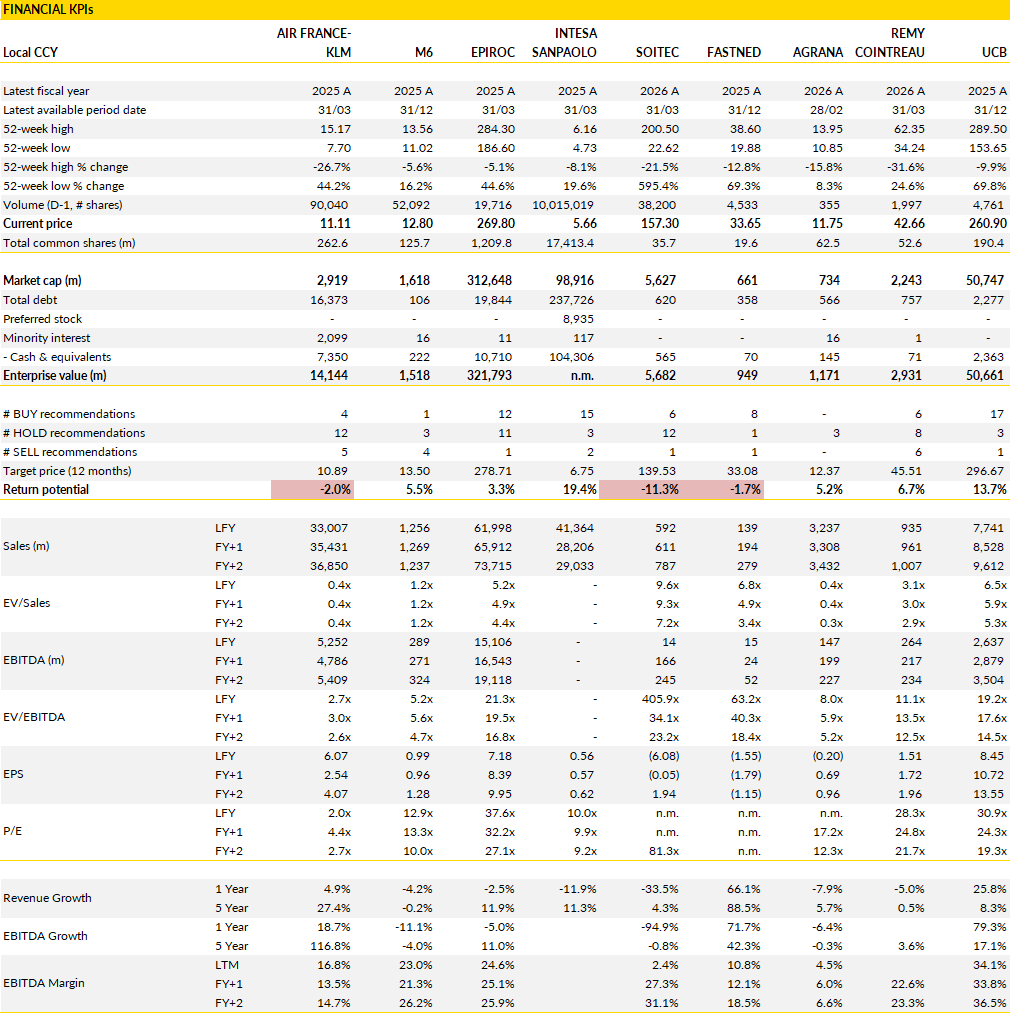

Financial KPIs

Air France-KLM (AF France): EasyJet may be available, but that does not mean Air France should buy it

Air France-KLM confirmed it could become involved in a potential transaction with easyJet after CEO Ben Smith indicated he would be willing to discuss any proposal brought forward by Castlelake.

Understandable, given easyJet's position within European aviation. Assets of this scale rarely become available. EasyJet controls valuable slots at some of Europe's most capacity-constrained airports, including Paris Orly, Amsterdam Schiphol and London Gatwick. It also remains one of the few genuinely pan-European airline platforms with meaningful scale across multiple countries. Any strategic airline would at least want visibility on a process involving such an asset.

The question is whether involvement would create enough value to justify the complexity. On that point, caution is warranted. EasyJet's slot portfolio is attractive, its market positions are attractive and its network would fit naturally alongside Transavia in several markets. None of those observations automatically make a transaction the right use of capital.

Air France-KLM already has plenty on its plate. The group remains focused on increasing its stake in SAS, a process expected to move forward during the second half of 2026. At the same time, discussions around TAP continue to circulate within the industry. Both situations arguably offer clearer industrial logic than a complicated easyJet consortium.

EasyJet is not a simple acquisition. Any transaction would likely involve multiple parties, significant regulatory scrutiny and potentially a break-up structure to address (anti-)competition concerns. The overlap between Air France-KLM and easyJet at several airports would attract immediate attention from regulators. A minority participation alongside a financial sponsor such as Castlelake would reduce those concerns but would also reduce the scope for synergies. Air France-KLM would then be committing capital without necessarily gaining operational control. That is a very different proposition from the airline acquisitions the group has pursued historically. Ben Smith's comments therefore look more defensive vs offensive. Ignoring a process involving one of Europe's largest independent airlines would be difficult. Winning and integrating is another matter entirely.

The more relevant takeaway may be the confidence management continues to express about the underlying operating environment. Demand trends remain healthy across the network, particularly through Paris Charles de Gaulle and Amsterdam Schiphol. Booking patterns have become shorter, which has been a recurring theme across the industry, but there is little evidence of a meaningful deterioration in traffic.

For investors, the debate around Air France-KLM remains about earnings, leverage and execution rather than M&A. The shares trade on roughly 3x EBITDA, a level that remains exceptionally low for a company generating solid demand and benefiting from a more rational European airline market than existed a decade ago. Debt remains the main reason for that discount. It also explains why management is unlikely to pursue an aggressive role in any easyJet transaction. Air France-KLM has spent years rebuilding credibility with investors and lenders. Protecting that progress probably carries more value than chasing a complex acquisition.

M6 (MMT France): The merger that failed in 2021 may be returning (in a different form)

Operationally, M6 remains one of France's strongest media assets, generating substantial cash flow, maintaining attractive audience positions and distributing large dividends. Strategically, it has long looked like an asset waiting for consolidation.

RTL Group has been trying to monetise its stake for years, while the French television market continues to face pressure from streaming platforms, digital advertising and shifting consumer habits. The latest reports suggesting renewed discussions between TF1, M6 and CMA CGM therefore s not a true surprise, but more a continuation of a longer-term development (since the collapse of the original TF1-M6 merger proposal in 2022).

The key difference today is structure. The previous deal attempted to combine the two broadcasters largely intact. The current discussions appear to focus on dividing M6's assets among multiple buyers, potentially creating a regulatory path that simply did not exist five years ago.

TF1 would likely be interested in the flagship M6 channel and potentially the radio assets, strengthening its position in the French television market and creating a platform capable of extracting substantial operating synergies. CMA CGM appears more interested in secondary channels and digital assets, fitting alongside the media portfolio it has already assembled through BFM and RMC. Such a structure would preserve competition between major media groups, a crucial point given the regulatory objections that ultimately killed the earlier merger attempt.

The industrial logic remains powerful. In 2021, management estimated annual synergies of €250m-350m. The media environment has arguably become even more challenging since then, increasing the incentive for consolidation. M6's audience share has gradually drifted below 8%, removing one of the ownership constraints that complicated discussions previously. At the same time, traditional television advertising faces greater competitive pressure from digital platforms, making scale more valuable than ever.

Timing remains the main obstacle. The M6 broadcasting licence cannot be transferred before May 2028 under current rules, making any transaction a multi-year process even if an agreement were reached quickly. That limitation does not prevent an announcement. A deal could be negotiated well in advance and completed once regulatory and licensing hurdles are cleared. Investors therefore face a situation where the value of M6 increasingly depends on strategic optionality instead of near-term earnings. Advertising trends remain soft, with television advertising declining during the first quarter, although sporting events should provide some support later this year.

On fundamentals alone, M6 already offers an unusually attractive profile, with a double-digit dividend yield, net cash and modest valuation multiples. Adding a credible path toward industry consolidation changes the equation. M6 thus remains one of the more interesting special situations in European media despite a business environment that remains far from ideal.

Epiroc (EPIA Sweden): Long‑term strategy unchanged while valuation already reflects strengths

Epiroc used its capital markets day to restate its strategic direction and revisit the themes that have shaped the group’s positioning in recent years. Management walked through the company’s innovation agenda, the role of automation and digital tools in productivity, and the contribution of electrified equipment. The financial framework was also reaffirmed. The group continues to target average growth of 8% at constant currencies over a full cycle, supported by 2 to 3% from acquisitions, along with high returns on capital, resilient margins, an investment grade balance sheet and a payout ratio of 50%. The company expects the mining market to expand by 3 to 5% annually over time, with infrastructure slightly faster at 4 to 6%.

Innovation remains central to the strategy. Automation continues to scale through LinkOA, the fleet‑agnostic system that now supports roughly 3,900 automated units. Management highlighted its potential in aggregates following a recent order from Heidelberg Materials. Digital tools are aimed at improving safety, productivity and sustainability across operations. Electrified equipment, which accounts for a small share of sales today, has surpassed 600 units and is positioned to reduce emissions and maintenance costs while improving performance. These three areas form the backbone of the group’s technology roadmap.

Margin recovery remains the main operational priority. The adjusted EBIT margin stood at 19.6% at the end of 2025, well below the 2022 peak of 23.7%. The decline reflects the integration of acquired businesses such as Stanley Infrastructure, weaker conditions in construction and infrastructure, and a less favourable mix within the equipment and services portfolio. Cost‑cutting measures introduced in 2024 have begun to show an effect, but management continues to focus on restoring profitability to historical levels.

Forecasts for organic growth between 2026 and 2028 have been raised to 7.6%, supported by stronger metal prices, particularly copper. Market expectations remain more optimistic, with consensus assuming organic growth of 8.4% per year through 2030, plus additional contributions from acquisitions. These assumptions exceed the company’s long‑term targets and rely on a smooth progression of the greenfield investment cycle despite geopolitical and macroeconomic uncertainties.

Epiroc used the CMD to underline its strengths in technology, aftermarket exposure and operational efficiency. However, the share price already reflects these qualities. The stock trades at more than 21 times forward EV/EBIT, a level that sits roughly above its historical average since the 2018 spin‑off.

Intesa Sanpaolo (ISP Italy): A deal that may reshape Italian banking again

Italian banking consolidation has accelerated dramatically over the past two years, yet Intesa Sanpaolo largely remained on the sidelines. Investors had become comfortable viewing the group as the disciplined incumbent: dominant market positions, strong profitability, relatively generous shareholder distributions and limited appetite for large acquisitions.

The surprise approach for Banca Monte dei Paschi changes that. At first glance, the transaction looks unusual given Intesa's already commanding position in Italy. But the group appears determined to prevent competitors from using Monte dei Paschi as a platform to build a stronger challenger. Banco BPM had only just begun exploring discussions with BMPS before Intesa moved. Allowing a rival to acquire those assets could have altered the balance of power within the domestic market. By acting now, Intesa keeps control of the consolidation agenda and ensures that any restructuring of the sector takes place on terms largely defined by itself.

The industrial rationale seems big. Intesa is not attempting to buy BMPS simply to add scale. The attraction lies in specific businesses that fit into existing strengths. Wealth management, consumer finance, insurance and corporate banking all become larger. Mediobanca's activities add another layer of appeal. Under the proposed structure, Intesa would retain the most attractive franchises while transferring a significant portion of branches and support functions to Unipol through a previously negotiated carve-out process. That feature is central to the transaction. Without it, regulatory approval would be far more complicated. With it, Intesa can potentially capture most of the earnings contribution while reducing competition concerns and limiting integration complexity.

The numbers are meaningful. Customer assets would move closer to €1.7tn, approaching targets originally envisioned much later in the decade. Customer relationships would increase by almost 30%, creating one of Europe's largest retail and wealth-management platforms. Consumer finance leadership would strengthen further, while corporate and investment banking would gain additional scale. None of this requires massive synergy assumptions to create value.

That said, several questions remain unanswered. The Italian government has historically played an active role in banking consolidation. Banco BPM may still attempt alternative combinations. UniCredit cannot be entirely ruled out as a participant in the broader consolidation process. Those uncertainties explain why investors have not immediately assigned full value to the proposal. Yet even without a completed transaction, the announcement changes the narrative around Intesa. For several years the investment argument rested on stable earnings, superior returns on equity and double-digit shareholder distributions. Those qualities remain intact.

The shares still trade at valuation levels that appear modest for a bank expected to generate returns above most European peers while distributing roughly 11% annually through dividends and buybacks. The BMPS proposal adds another layer. Intesa is positioning itself to determine what the Italian banking landscape looks like at the end of the decade.

Soitec (SOI France): Photonics excitement is replacing a mobile downturn, but expectations are running ahead

A few months ago, the discussion around Soitec revolved around collapsing demand, inventory corrections and the first loss in a decade. Today the conversation looks completely different.

The annual results still reflected a difficult year, with revenue down roughly one-third and EBITDA almost halved, but investors have largely stopped caring about this. The market is now just trying to determine how large the photonics opportunity can become and whether Soitec can establish itself as a critical supplier to the AI infrastructure buildout.

Recent management comments appear to have strengthened confidence on that front. Demand linked to optical connectivity inside data centres is accelerating rapidly as AI models become larger and computing clusters more complex. Management highlighted growing customer engagement, ongoing qualification work and the prospect of commercial co-packaged optics production beginning next year. Unlike many semiconductor stories, the immediate constraint does not appear to be demand. Existing manufacturing assets can support a meaningful increase in output, limiting the need for a major spending program. For investors searching for exposure to AI infrastructure beyond the obvious names, that narrative has become increasingly attractive.

At the same time, the legacy business is slowly moving from being a headwind to becoming 'neutral'. Mobile communications still represented more than half of revenue last year, yet the division remains constrained by customer inventory levels that are far above historical norms. Before Covid, customers typically carried around six months of inventory. Current levels remain closer to sixteen months. As a result, Soitec is supplying only a fraction of end-market demand despite healthy consumption trends.

Management appears increasingly confident that this distortion will gradually disappear over the next eighteen months. When that happens, RF-SOI volumes should recover without requiring heroic assumptions around smartphone growth. There are also additional opportunities from technologies such as POI that could contribute incremental growth. The new leadership team is simultaneously reviewing the broader product portfolio and focusing on operational efficiency. Factory utilisation remains unusually low, foreign exchange remains a drag and subsidy support is declining, which means profitability recovery will lag revenue recovery. Even so, the worst phase of the downturn increasingly appears to be behind the company.

The challenge is valuation. The investment debate is no longer about whether Soitec can return to growth. It is about how much future success is already reflected in the share price. After rising more than 500% this year, the stock is trading at levels rarely seen in its history. Multiples have expanded to roughly double long-term averages, despite profits still sitting near cyclical lows. Market forecasts have moved higher as photonics demand accelerates and EBITDA estimates for the next two years have been raised meaningfully.

But caution may be warranted, as the market is already discounting a very ambitious future. To justify a substantially higher valuation from here, investors must believe photonics revenue can multiply several times over before the end of the decade and that Soitec captures a leading position in that market. That outcome is possible. The company has technological advantages, established customer relationships and a growing role in AI-related infrastructure. The difficulty is that expectations have become extremely demanding. At current levels, execution needs to be close to flawless. Any delay in photonics adoption, slower customer qualifications or a more gradual recovery in mobile demand would leave little room for disappointment.

Fastned (FAST Netherlands): Commercial shift and operational Reset

Fastned used its AGM and the follow‑up event to walk through how the business is changing. Management highlighted a shift toward a more active commercial approach, adding new sales channels through partnerships with other charging networks, deeper engagement with carmakers, and a broader push into the B2B market, including fleet operators and electric truck owners. The company is also putting more effort into brand awareness, moving beyond the charging‑experience focus of earlier years and introducing marketing campaigns, membership offers, and more flexible pricing. With app registrations rising sharply, Fastned wants to steer customers toward preferred charging habits by offering discounts during quieter hours or when electricity prices are lower. Management also noted that recent developments in the Middle East have pushed more drivers toward EVs, supported by longer driving ranges, price parity with combustion cars, and meaningfully lower charging costs.

The company has been scaling its internal structure to support this shift. Over the past year it strengthened its Centre of Operational Excellence, focusing on digitalizing workflows, integrating IT systems, and rolling out a new CRM platform. Local management teams have been reinforced across all operating countries to better address differences in market conditions. Fastned expects its workforce to exceed 500 people in 2026, up from 420 in 2025. In the more mature Dutch market, where BEV penetration has reached 7.4%, annualized revenue per station stands at €465k, and operational EBITDA per station is €225k, illustrating the potential for other European markets as they catch up.

For 2026, Fastned is concentrating on building, growing, and optimizing. Management emphasized that after several years of heavy investment, the priority now is improving efficiency, automating processes, and reducing indirect costs. With a new retail bond round underway, the company reiterated its outlook: adding 70-100 new stations to reach 476*506 sites, lifting revenue per station above €350-400k, and achieving an operational EBITDA margin of 35-40%, excluding any benefit from the German highway tender.

Management also addressed past challenges, noting that weaker‑than‑expected BEV adoption and insufficient cost control had weighed on EBITDA in recent years. They now see conditions improving, helped by a rebound in BEV demand and the arrival of an interim CFO focused on tightening operating, expansion, and capital spending.

Agrana (AGR Austria): Mixed segment trends and slow sugar recovery

Agrana’s sugar business remained a major burden on results, with revenues falling 32% and the segment posting an operating loss of €30.6m in the year. Once one‑off items and restructuring costs are included, the loss widened to €106.5m, marking a third year of heavy pressure. Management still sees the potential for a gradual recovery as reduced beet acreage tightens supply and supports pricing, but the near‑term picture is clouded by unusually high inventories across Europe. For the new financial year, the company expects stable volumes but weaker sugar prices, leading to another sizeable operating loss. Savings under the Next Level program remain the bright spot, with €89m delivered last year and around €100m targeted for the current year, though these gains are still outweighed by the difficult sugar market.

The fruit, beverage and specialties segment continued to provide stability, with revenues up 1% and margins holding at 6.3%. For the year ahead, Agrana expects 5–10% revenue growth, partly helped by the consolidation of Mercator EMBA. Profitability, however, is set to come under pressure. Severe frost in Hungary last year led to a very weak apple harvest, which will limit capacity utilisation and weigh on earnings. Management anticipates a 5–10% decline in EBIT, and the company’s margin‑accretive acquisition helps soften, but not eliminate, this impact.

In starch, revenues slipped 3% and margins fell to 2.2% as lower selling prices and higher costs squeezed profitability. The outlook is more positive, with management expecting stable revenues and a clear improvement in earnings. A sharp rise in ethanol prices following geopolitical tensions in the Middle East is the main driver, supporting a rebound in margins. Agrana sees this lifting profitability meaningfully in the current year, though the outcome will depend on ethanol prices staying elevated.

Across the group, visibility remains limited. Savings efforts are progressing well, but the timing and strength of the sugar recovery are now less certain than before. Management still sees a path back to profitability in the sugar segment by FY 2028–29, but this depends heavily on continued delivery of cost reductions under the Next Level program to lower the breakeven point.

Rémy Cointreau (RCO France): A recovery plan built around execution, not financial engineering

Rémy Cointreau is trying to move the discussion away from tariffs, Cognac inventories and weak end markets and towards what the business could look like several years from now. The company recently provided more colour on its post-downturn ambitions, although investors still need to wait until November for formal medium-term guidance.

From the latest update we've seen a management team focused on rebuilding profitability through better execution. The headline objective is straightforward: add roughly €100m of operating profit by 2029. If achieved, earnings would return to levels last seen before the industry entered its current slump. The route to get there is mainly about reallocating resources, concentrating marketing behind the strongest brands and expanding distribution into areas where Rémy believes it remains underrepresented. Management has clearly been signalling that the next phase will depend as much on commercial discipline as on macro conditions.

The growth agenda itself looks quite different from the one investors associated with the company a decade ago. China and the US remain critical markets, but much of the planned expansion is expected to come from areas that currently represent a relatively small portion of the business. Travel Retail and emerging markets are both targeted to double in size over the coming years, with particular attention on India, Brazil, Mexico and parts of Africa. In the US, the focus is shifting towards convenience retail, e-commerce and products aimed at higher-volume consumption occasions rather than purely prestige positioning.

Management also sees room to expand categories beyond premium Cognac. Brands such as Cointreau and The Botanist feature prominently in the plan, reflecting the desire to broaden the earnings base and reduce reliance on one category. Product formats are being adapted to fit changing consumption patterns, including cocktail culture and ready-to-drink trends. Internally, procurement, marketing allocation and organisational simplification are expected to contribute meaningfully to profitability gains. The message though is not one of austerity. Spending will continue, but management wants a larger share of every euro invested to generate revenue growth.

The latest results were 'respectable', but that is all. Operating profit came in close to market expectations, earnings per share benefited from below-the-line items and guidance for the current year implies only a modest return to growth. Consensus estimates for next year are unlikely to move dramatically. Investors appear more interested in the possibility that the company has finally reached the low point of the cycle.

That may prove correct, but visibility remains limited. The balance sheet still carries leverage above historical levels, which explains the dividend reduction and the renewed emphasis on capital allocation. Management is prioritising debt reduction while preserving flexibility for investment. At roughly 25x earnings, the valuation already assumes a degree of recovery. The long-term plan is credible, but many of the key assumptions still need to be proven.

UCB (UCB Belgium): Bimzelx is building a case to become one of the defining assets

UCB spent years arguing that Bimzelx could become a major player across inflammatory diseases. The latest data in psoriatic arthritis gives the company its strongest piece of evidence yet.

In the BE BOLD study, Bimzelx became the first approved biologic to demonstrate superiority over AbbVie’s Skyrizi in a head-to-head trial in psoriatic arthritis, achieving ACR50 response rates of 49.1% versus 38.4%. Equally important was the speed of response. Separation between the two therapies was already visible after four weeks, with response rates of 19.9% compared with 7.2%. Rheumatologists place significant value on rapid control of inflammation because delayed treatment can lead to irreversible joint damage. The study also showed stronger combined outcomes across joint and skin disease, while complete skin clearance remained highly competitive. For a drug competing in one of the most crowded areas of immunology, these are the types of results that influence prescribing habits rather than simply adding another line to a product label.

The broader significance is that UCB continues to accumulate comparative clinical evidence at a pace rarely seen in large immunology franchises. Many successful drugs rely on placebo-controlled studies and indirect comparisons. Bimzelx increasingly has direct evidence against established competitors. The company now has multiple superiority studies across different indications, giving physicians a growing body of real-world relevant data when making treatment decisions. That clinical record arrives at an important moment. Bimzelx is already approved in five indications, is marketed in more than 50 countries and still has numerous regulatory reviews underway.

The opportunity therefore extends beyond market share gains in existing categories. Each new indication expands the addressable market and deepens physician familiarity with the product. UCB's strategy has been straightforward: keep broadening the evidence base, keep expanding labels and allow commercial momentum to build from there. Recent results suggest that approach is working. Bimzelx is no longer viewed simply as another entrant in the IL-17 class. It is increasingly becoming one of the reference products against which competitors are measured.

The attraction of UCB today extends beyond a single drug. The company now has a collection of growth assets spread across immunology and neurology, reducing dependence on any one product cycle. Bimzelx remains the largest value driver, but newer products such as Rystiggo, Zilbrysq and Fintepla are also contributing to growth. That portfolio mix gives UCB exposure to several attractive therapeutic areas without carrying the concentration risk often associated with biotech-style stories.

Consensus seems to have recently increased assumptions for Bimzelx sales over the coming years while also factoring in higher research spending following recent acquisitions. Even after those adjustments, earnings growth remains substantial. The market continues to focus on quarterly prescription trends and indication launches, but the more important development is the gradual strengthening of UCB's competitive position. A few years ago the company was heavily reliant on ageing franchises and pipeline execution. Today it owns one of the strongest growth platforms in European biopharma, supported by assets that are gaining both clinical credibility and commercial traction.