AI in payments, strategic reviews and inflections

Adyen, Virbac, Redcare Pharmacy, Securitas, Clariant, Prosegur, Banqup Group, Planisware, BioNTech, Eramet, AT&S, Figeac Aéro

At Lux Opes, we break down companies into quick takes that get straight to the point - what is happening, why it matters, and what to watch next. We publish 2-4 times per week, depending on the news flow.

For the best reading experience, we recommend reading at Lux Opes

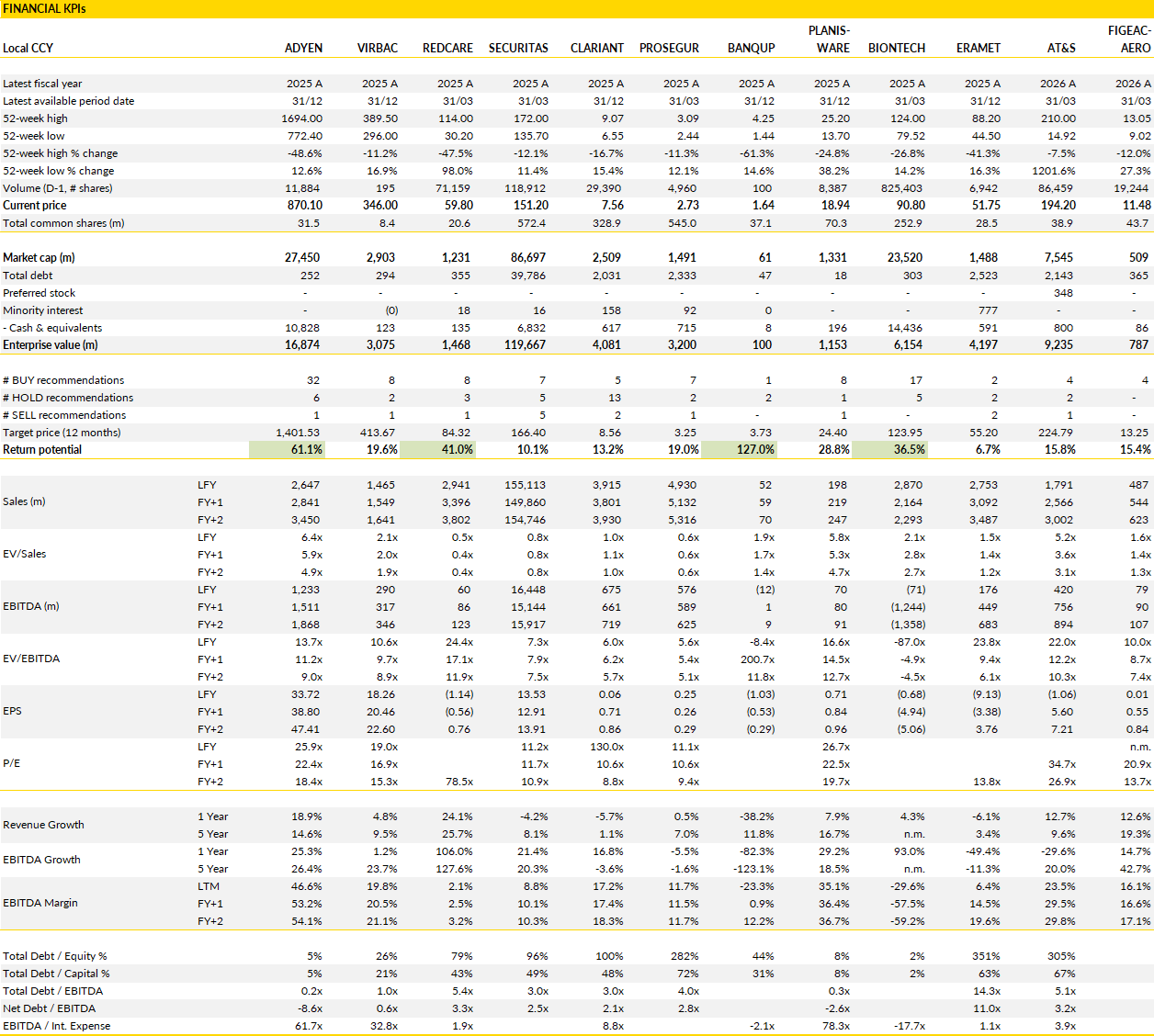

Financial KPIs

Companies covered in this edition: Adyen, Virbac, Redcare Pharmacy, Securitas, Clariant, Prosegur, Banqup Group, Planisware, BioNTech, Eramet, AT&S, Figeac Aéro

Adyen (ADYEN Netherlands): More AI

For most of its history, Adyen followed an unusually disciplined strategy. The company built its platform internally, avoided acquisitions and focused almost exclusively on payments infrastructure. That approach has now changed.

Within a matter of weeks, Adyen completed two acquisitions, spending roughly €1bn on Talon.One and Orb (roughly 75/25 split). The move says a lot about how management views the next phase (of competition). Payments remain the foundation of the business, but merchants increasingly need software layers that sit above payments and help manage customer relationships, pricing and monetisation. Adyen appears determined to become more deeply embedded in those workflows. The acquisitions are not about adding transaction volume (directly, at least). They are about ensuring that the fastest-growing digital businesses choose Adyen as their long-term platform partner.

The first transaction brought Talon.One into the group, adding sophisticated promotion, loyalty and customer engagement capabilities. The second acquisition, Orb, targets a different, important area. Many software, AI and cloud-native businesses are abandoning traditional subscription models in favour of usage-based pricing. Customers are increasingly billed according to consumption rather than fixed monthly fees. That sounds simple in theory, but it requires sophisticated infrastructure for metering, billing, invoicing and pricing experimentation. Orb specialises in exactly that. The platform allows merchants to test pricing structures, manage large volumes of consumption data and adapt commercial models without rebuilding underlying systems. This capability is becoming increasingly valuable as AI services, cloud applications and digital platforms move toward more flexible pricing arrangements. Stripe recognised the same trend earlier this year when it acquired Metronome. The fact that both companies are making similar moves highlights how quickly billing infrastructure is becoming a strategic layer rather than a back-office function.

Let's see about execution. Adyen has built its reputation on organic development and product consistency. Integrating acquisitions is naturally something else. Retaining founders, keeping engineering teams motivated and successfully embedding new products into the broader ecosystem will determine whether these deals create meaningful value.

Investors should also recognise that management is allocating a significant amount of capital. Combined spending on Talon.One and Orb is roughly equivalent to a full year of net profit. That is a notable departure from the company’s historical conservatism.

Still, there is a logic behind the decision. AI is accelerating changes in how digital businesses operate, how products are sold and how revenue is generated. Building every capability internally could take years, while specialist providers already possess proven technology and established customer bases. Adyen is effectively trying to position itself closer to the operating systems used by modern merchants rather than remaining solely a payments processor.

If management executes well, these acquisitions could strengthen the company’s ability to attract high-growth software, AI and digital-native customers. The market still values Adyen primarily as a payments company. Management appears to be laying the groundwork for something broader.

Virbac (VIRP France): Merger speculation

Virbac shares have periodically attracted takeover and consolidation speculation over the years, and the latest comments from Céva’s leadership have reignited that discussion. According to press reports, Céva’s executive chairman indicated he would be open to a combination between the two companies, arguing that France could support a larger national champion in animal health.

On paper, the logic is easy to understand. Céva generates roughly €1.9bn of revenue and holds strong positions in vaccines, poultry and swine health, while Virbac generates around €1.5bn of sales with greater exposure to companion animals and ruminants. The portfolios are complementary, there would be opportunities to streamline manufacturing, procurement, R&D and commercial infrastructure, and the combined entity would immediately become one of the largest independent veterinary health companies globally. Yet industrial logic and deal probability are very different. Virbac’s response was notably direct, stating that no merger discussions are under consideration and that management remains focused on its own strategic roadmap.

That stance is no surprise. The Dick family has consistently prioritised independence and long-term development over financial engineering. At the same time, Virbac is already in the middle of a substantial growth program that leaves little room for a transformative merger. Capital spending plans are underway, resources are being directed toward product launches and geographic expansion, and management is pursuing a strategy built around targeted acquisitions rather than large-scale consolidation. Integrating a business of Céva’s size would require years of operational work across manufacturing sites, research centres and overlapping support functions. Even if a deal eventually emerged, the integration effort alone could distract management from opportunities already visible today.

The more interesting question is what Virbac looks like as a standalone business over the remainder of the decade. The company operates in one of healthcare’s most attractive niches, supported by rising pet ownership, growing spending on animal care and increasing demand for livestock productivity. Management plans around 60 market entries over the next five years and continues to narrow its focus toward larger franchises with stronger economics. The product pipeline remains substantial, with dozens of programmes carrying meaningful commercial potential.

Margin expansion is another important element of the plan. Operating margins are expected to move from roughly 17% today toward 20% by 2030 through a combination of higher volumes, improved mix and greater operating efficiency. Cash generation remains healthy and acquisitions continue to play a role, though primarily through smaller transactions and licensing agreements.

Against this backdrop, the merger debate feels somewhat misplaced. Investors do not need a takeover to justify the investment case. The existing strategy already offers a credible path to higher earnings, broader geographic reach and improved profitability in a sector that continues to grow regardless of the economic cycle.

Redcare Pharmacy (RDC Germany): Prescription momentum keeps surprising to the upside

Redcare entered 2026 with the market mainly focused on two questions. The first was whether electronic prescription adoption in Germany would continue at a pace capable of supporting the company’s ambitious growth targets. The second was whether management could reignite growth in the traditional non-prescription business while preserving profitability.

The latest trading update offered encouraging evidence on both fronts. Revenue growth accelerated sharply during the first months of the second quarter, reaching more than 20%, comfortably ahead of market expectations. The strongest contribution again came from the German prescription business, where sales increased 57%, reflecting continued gains in e-prescription penetration and further market share expansion. Just as important, the non-prescription operation also strengthened materially. German non-Rx growth moved from 9% in the first quarter to double-digit levels in both April and May, suggesting that consumer demand remains healthy despite a difficult retail backdrop. For a company that has often been viewed as a single-theme prescription story, seeing both contributing simultaneously is just nice.

Management responded by raising its full-year growth outlook. Revenue is now expected to increase between 15% and 17%, above previous guidance and ahead of what consensus had been modelling. The prescription business remains the largest driver. Redcare now expects German Rx revenue of €680m-720m this year, pointing to another year of exceptional expansion in what remains a structurally underpenetrated market. The more interesting change may actually be the non-Rx guidance. Management lifted its expectations to 10%-12% growth, a clear indication that recent trends are not viewed as a temporary spike. Profitability is also moving in the right direction. Adjusted EBITDA margin guidance now stands at 2.5%-3.0%, reflecting operating leverage. This is important because critics have often argued that online pharmacy growth comes at the expense of marketing intensity and margin pressure. The latest figures suggest operating leverage is (finally) beginning to emerge as scale increases.

The challenge at Redcare remains whether growth can ultimately translate into the level of cash generation implied by the valuation. The company is building a dominant position in what could become one of Europe’s most attractive digital healthcare markets, but the market still seems to be waiting for evidence that strong revenue expansion can evolve into substantial free cash flow. That remains the missing piece.

Even so, the latest update strengthens the argument that Redcare is becoming more than a regulatory or adoption story. Prescription volumes continue to expand at an impressive pace, non-prescription sales have regained momentum, and profitability is improving at the same time.

Securitas AB (SECUB Sweden): From a transformation phase to an earnings growth phase

Securitas' acquisition of Stanley Security accelerated a shift that was already underway, which is moving the group further into technology, remote monitoring, integrated security solutions and data-driven services. The latest capital markets update reinforced this direction.

Management is increasingly focused on what it calls intelligence-led security, combining physical security, software, analytics and consulting capabilities into a broader offering aimed at helping clients anticipate risks rather than simply react to them. The objective is simple: move further up the value chain and increase the share of revenue generated by activities that carry stronger margins, higher retention rates and deeper customer relationships. This evolution is visible in the numbers. A decade ago, guarding dominated the business. Today, technology and solutions represent a much larger share of revenue and an even larger share of profit growth.

The most important announcement from the event was financial. For the first time, management introduced a quantified target of 10% annual EPS growth through 2030. That figure is above consensus and creates a measurable benchmark against which future execution can be judged. The target margin remains above 10%, unchanged, but the combination of margin expansion, stronger cash generation and disciplined capital allocation makes the earnings ambition more tangible than before.

The company also upgraded its cash conversion objective, now targeting CFO-to-EBIT conversion of 80%-90%, compared with the previous 70%-80% range. This is an important detail because the quality of earnings has improved alongside profitability. Security technology, monitoring platforms and software-heavy solutions require less working capital than traditional guarding contracts and generally generate stronger cash flow characteristics. Net debt remains modest at roughly 2.1x EBITDA, leaving room for bolt-on acquisitions that can accelerate the mix shift without creating balance sheet pressure.

What makes the Securitas story interesting today is that the market still appears reluctant to fully acknowledge how much the business has changed. Consensus forecasts continue to assume only moderate earnings progression and margins that remain well below management’s long-term ambition. Yet the company has already demonstrated meaningful improvement. Adjusted EBIT margins reached 8% during the second half of 2025, compared with levels closer to 5% several years ago.

Additional progress does not require strategic pivots, jsut continued execution of a plan that is already producing results. Technology penetration can increase further, cross-selling opportunities remain significant across the existing customer base, and the balance sheet provides flexibility to acquire specialised capabilities where necessary.

Securitas is increasingly becoming an earnings growth company with a steadily improving business mix, stronger cash generation and a management team willing to commit publicly to a double-digit earnings trajectory.

Clariant (CLN Switzerland): Potential re‑opening winner on already cautious consensus for 2026

Clariant recently highlighted steady progress in Care Chemicals, where value‑based pricing is holding up despite shifts in raw material and energy costs since the Middle East crisis began. The segment has moved from passing through lower input costs earlier in the year to actively mitigating inflation, with recent price initiatives in Personal and Home Care showing resilience. Volumes have not shown signs of demand destruction, keeping the business on track for slight underlying growth, even as portfolio pruning trims around 2% of sales.

In Adsorbents & Additives, the company continues to benefit from favourable regulation in renewable fuels, which should help turn a mid‑single‑digit sales decline in Q1 into growth for the full year. Additives is seeing support from the ramp‑up of new Chinese flame‑retardant capacity and reduced availability of competing brominated products from Israel, reflected in low single‑digit growth in the first quarter. These trends suggest a more constructive backdrop for the segment through 2026.

Catalysts remains the soft spot, with delayed refill orders in the Middle East weighing on the first half. A gradual recovery in China is encouraging, but adjusted EBITDA for H1 is likely to be roughly half of last year’s level. The outlook for the second half depends heavily on petrochemical refinery restarts in the Middle East, which require the reopening of the Strait of Hormuz. So recent developments support the company’s expectation of a rebound, with segment EBITDA projected to recover meaningfully compared with the prior year.

Clariant’s full‑year guidance implies adjusted EBITDA of around CHF 670-685m, while current market expectations sit slightly below this range. If Middle East operations resume steadily, the company could benefit from a stronger second half, particularly in Catalysts. Care Chemicals and Adsorbents & Additives, which together represent the majority of group profitability, continue to show constructive trends, though uncertainty in Catalysts still weighs on visibility.

Prosegur (PSG Spain): Securitas raises the bar

Securitas’ latest strategic update (see above) signals a clear shift in the security industry toward higher‑value, technology‑enabled services. The company is moving away from traditional guarding and positioning itself around data, analytics, and AI‑driven security models. Its long‑term framework targets steady earnings growth, strong cash conversion, and a margin ambition above 10%, well above current levels for both Securitas and Prosegur. For Prosegur, this reinforces the direction of its Hybrid Security roadmap, showing that the market increasingly rewards providers able to combine people, technology, and data into integrated solutions.

The most relevant comparison lies within the security divisions. Securitas’ Ibero‑America business generated around €1.3bn of sales in 2025, with 37% coming from technology and solutions and a margin of 7.6%. Prosegur Security, by contrast, delivered €2.6bn of sales but only about €90m of EBITA, implying a margin near 3.5%. This gap highlights the potential for improvement if Prosegur accelerates its mix shift toward higher‑value offerings. Clearer disclosure on the share of technology‑driven solutions, sustained margin progress in Spain and the US, and consistent cash generation would help demonstrate that the division is moving in the right direction. The fact that Security reached cash breakeven for the first time in Q1 2026 is an encouraging early sign.

Competitive dynamics matter most in Spain and Portugal, which account for the majority of Securitas’ regional sales. A stronger push into intelligence‑led security could intensify competition in large corporate tenders, especially where clients seek integrated solutions. At the same time, it supports the idea that customers are increasingly willing to pay for outcome‑based, technology‑enhanced security rather than commoditised manpower. This environment plays to Prosegur’s strategy of expanding bundled Hybrid Security contracts, which combine physical presence with digital capabilities.

Taken together, Securitas’ update provides a supportive backdrop for Prosegur. It shows that the industry can structurally move toward better margins, stronger cash conversion, and more technology‑led contracts. Prosegur already matches Securitas at the group margin level, and its Security division offers meaningful catch‑up potential if execution continues to improve.

Banqup Group (BANQ Belgium): Strategic review

Banqup has spent the last several years trying to simplify a business that was built through multiple activities, technologies and acquisitions. The result has been a company with a valuable e-invoicing platform sitting alongside slower-growing and lower-margin operations, making it arguably difficult for the market to understand what they actually own.

The latest announcement suggests management is working to change this. Following a strategic review conducted with Lazard, the group is now exploring a range of options including divestitures, alternative financing structures and even a full sale of the company. The review once again confirms that quality of the e-invoicing and e-reporting activities. This business combines recurring revenue, attractive margins, strong visibility and declining capital requirements. It also sits directly in the path of a powerful regulatory tailwind as mandatory e-invoicing rules begin rolling out across Europe. France is first (Q3 this year), followed by Germany and Spain, creating a multi-year growth opportunity that is largely independent of the broader economic cycle.

The disconnect between the core business and the market valuation has become increasingly difficult to ignore. Recent operating trends illustrate the problem. The digital activities continue to grow at a healthy pace while legacy operations shrink rapidly. Profitability is equally different. The software and compliance platforms generate margins that resemble a SaaS business, whereas the remaining operations carry a much lower earnings profile. Combining those activities into a single listed entity has created a valuation discount that management clearly believes is excessive.

Investors looking at consolidated numbers see a mixed business with modest growth. Looking at the e-invoicing operation on a standalone basis would likely produce a very different conclusion. That appears to be the central finding of the strategic review. The current structure masks the quality of the strongest asset and limits the market's willingness to assign a premium multiple.

The interesting question now is what value enhancing structure will be chosen. A separation of assets would probably be the most direct route, allowing investors to value the e-invoicing platform independently from the rest of the group. A sale of individual businesses is another possibility. A full takeover cannot be ruled out either, although that outcome depends on the willingness of buyers to look beyond the company's limited liquidity and small market capitalisation. Timing remains uncertain, and corporate reviews often take longer than investors expect. There is also the broader challenge that software valuations have become less generous as markets debate the long-term impact of AI on certain business models.

Even so, Banqup now finds itself in a position where strategic optionality is becoming a larger part of the investment case. The operating business is benefiting from favourable regulatory trends, the balance sheet is stronger than it was a few years ago, and management has publicly acknowledged that the current structure is failing to reflect the value of the underlying assets.

Planisware (PLNW France): Expanding the platform while making AI practical

Planisware’s annual Exchange26 conference provided a useful reminder that the company is approaching AI from a very different angle than many software vendors.

Rather than presenting AI as a standalone product, management is embedding new capabilities directly into the workflows that customers already use for project portfolio management, product development and resource allocation. The latest evolution of Oscar, the company’s existing AI assistant, reflects that approach. What started as a single assistant is gradually becoming a collection of specialised agents tied to specific functions within the platform. The bigger announcement, however, was Prisma, a new hybrid agent designed to work across Planisware’s ecosystem while drawing on a customer’s own operational data and business processes. The objective is not simply to generate insights but to automate actions, reduce manual configuration work and make the platform easier to use. For a business whose software can be highly powerful but also complex, lowering the barrier to adoption could prove incredibly valuable.

Alongside the AI roadmap, management is reshaping how the company presents its products to customers. Historically, Planisware sold a broad platform with different modules that could be combined depending on the customer’s needs. The new strategy packages those capabilities into more clearly defined offerings aimed at specific markets. Horizon targets IT portfolio management, Nova focuses on product development, while additional launches are planned for engineering projects, revenue-generating project portfolios and asset investment planning. In many ways this is a commercial rather than technological change, as the underlying software already exists. The benefit is improved visibility. Customers can more easily understand what the platform offers, sales teams can position solutions more clearly, and AI models can interact with a more structured product architecture. Each of these verticals represents a sizeable addressable market in its own right, giving Planisware additional avenues for expansion beyond its traditional customer base.

What also stands out is consistency. The company continues to invest heavily in product development while maintaining a focus on profitable growth. Unlike many software firms that are racing to build proprietary large language models, Planisware is taking a more pragmatic route. Prisma is designed to remain LLM-agnostic, allowing customers to connect the models of their choice while reducing dependence on rapidly changing AI economics. Monetisation is also being approached in a structured manner, with different pricing tiers ranging from basic functionality to advanced tools aimed at administrators and engineers.

The overall picture is a company that continues to strengthen its position in a specialised software category where execution, domain expertise and customer relationships often matter more than headline AI announcements. Revenue and EBIT are still expected to grow at double-digit rates, yet the valuation remains well below that of many software peers. The market appears to remain cautious, but the operational trajectory looks considerably stronger than the share price suggests.

BioNTech SE (BNTX US): Investment case now supported by several late‑stage assets in oncology

BioNTech’s latest data for pumitamig presented at ASCO 2026 strengthened confidence in its position within the emerging class of PD‑(L)1 x VEGF bispecific antibodies. In the ROSETTA Lung‑02 study, confirmed response rates reached 63.6% in non‑squamous NSCLC and 72.7% in squamous NSCLC at the Phase III dose, despite more than half of patients being PD‑L1‑negative. The activity seen in this harder‑to‑treat group, with a confirmed response rate of 47.6%, suggests the mechanism could broaden the reach of immunotherapy beyond biomarker‑selected populations. The development plan is wide‑ranging, with ongoing studies in TNBC, SCLC, HER2+/PD‑L1+ gastric cancer, mCRPC, hepatocellular carcinoma and MSS‑CRC. The choice of PFS as the sole primary endpoint in ROSETTA Lung‑02 has sparked debate, but the aim is to accelerate regulatory timelines while keeping OS preserved in the statistical plan.

A major long‑term differentiator for BioNTech lies in its ability to build proprietary combinations around pumitamig. The company has several complementary therapeutic platforms, including late‑stage ADCs, mRNA immunotherapies and multiple immunomodulators. The next advances in oncology are expected to come from combinations that deepen and prolong responses while addressing resistance mechanisms without compromising safety. Initial data from combination studies pairing pumitamig with trastuzumab pamirtecan, BNT324/DB‑1311 or BNT326, expected in the second half of 2026, will be important in testing this strategy. Additional readouts from gotistobart in squamous NSCLC, trastuzumab pamirtecan in HER2‑low breast cancer, and BNT113 in HPV16+ ENT cancers should help show how BioNTech is assembling several interconnected oncology franchises.

The company’s pipeline now spans multiple platforms that can be combined within a single portfolio and applied across a broad range of solid tumours. This diversification reduces reliance on any single modality and creates multiple independent clinical opportunities. BioNTech also has a sizeable cash position of €16.8bn, giving it the ability to fund pivotal trials while continuing to invest in business development.

Eramet (ERA France): The shareholder question is becoming as important as the commodity cycle

Reports surged that Orion Critical Minerals is discussing the acquisition of part or all of the Duval family’s 37% stake have shifted attention toward a topic that has been lingering in the background for years.

The timing is not accidental. Eramet is entering a crucial period that includes a planned €500m capital increase, potential asset disposals and a broader effort to strengthen a balance sheet that has come under pressure following large investments and weaker commodity markets. A new strategic shareholder with substantial financial resources would immediately change how investors assess the company's ability to execute that roadmap. Orion, backed by US and UAE capital and focused on securing access to critical minerals, fits naturally with Eramet’s portfolio of manganese, nickel and lithium assets. The industrial logic is straightforward, particularly at a time when Western governments are trying to diversify supply chains away from Chinese dominance.

The challenge is that financial logic and political reality may not point in the same direction. The French state already owns 27% of Eramet and remains a key stakeholder in any major corporate decision. Allowing a foreign-backed investment vehicle to become the dominant shareholder of one of France’s most strategically important mining groups could prove politically difficult.

The timing adds another layer of complexity. France is approaching a presidential election cycle, a period when governments are generally reluctant to approve transactions involving national industrial assets and foreign influence. Even if Orion were interested in taking a large position, there is no guarantee that such a move would receive political support. For that reason, a full replacement of the Duval family appears less likely than a more limited participation in future financing rounds. Other potential investors may also emerge. Sovereign wealth funds, particularly from countries with strategic interests in critical minerals, could find Eramet’s asset base attractive despite the operational and geopolitical risks associated with locations such as Gabon, Indonesia, Senegal and Argentina.

Overall, this makes the investment case more interesting. On one side sits a collection of valuable mining assets positioned in commodities that are likely to remain strategically important for decades. Eramet holds meaningful positions across several critical mineral markets and generally operates assets that sit in competitive parts of the cost curve. On the other side sits a complicated financial agenda, political uncertainty and commodity prices that have softened after a strong start to the year. Nickel and manganese markets remain volatile, while lithium has yet to establish a sustained recovery.

The next phase for Eramet may therefore depend more on whether management can secure the right partners to support its financing needs. A successful capital raise backed by credible long-term investors would remove a major overhang. Failure to do so would leave the market focused on balance sheet concerns rather than the underlying quality of the asset portfolio.

AT&S (ATV Austria): AI demand rewrites the economics of the business

AT&S has spent years fighting a perception problem. Investors largely viewed the company as a cyclical substrate manufacturer trapped in an industry prone to overinvestment, margin compression and periodic balance-sheet stress. That scepticism was understandable. The group deployed enormous amounts of capital over the past decade, generated deeply negative cumulative free cash flow and repeatedly asked investors to look beyond the next downturn.

The latest guidance update changes that discussion in a meaningful way. The company is no longer talking about modest utilisation improvements or incremental efficiency gains. It is projecting a step change in profitability, with EBITDA expectations rising by roughly 50% and margins moving into territory that would have seemed unrealistic only a year ago. Just as important, management now expects strongly positive free cash flow despite a new investment program approaching €2bn. This combination was largely absent from the previous AT&S narrative and explains why the market has completely re-evaluated the stock.

The catalyst is demand for advanced AI substrates. AT&S has reached agreements with AMD and another major technology customer, widely assumed to be a hyperscaler, to expand production capacity in Malaysia. Unlike previous industry expansion cycles, this project appears heavily supported by customer commitments, including long-term agreements and prepayments. That distinction is critical. Historically, substrate manufacturers often built capacity first and hoped demand would arrive later. AT&S is now describing a model where customers effectively help finance the expansion.

The result is a dramatically different risk profile. Management expects revenue growth of 45-55% next year, compared with previous expectations of 30-35%, while EBITDA margins are projected to rise into a 32-37% range. Those numbers imply that advanced AI-related packaging carries substantially better economics than many investors had assumed. They also suggest that bargaining power has shifted in favour of suppliers as customers compete for access to advanced substrate capacity.

That does not mean the risks have disappeared. The substrate industry remains cyclical and competitors are responding aggressively. Ibiden and Unimicron are both increasing investment, and industry history shows that periods of exceptional profitability often attract new capacity. There are also longer-term technology questions surrounding glass substrates and next-generation packaging architectures. AT&S may have reduced financing risk, but it has not eliminated industry risk.

After a share-price increase of more than 350% this year, investors are no longer paying distressed multiples for the business. The stock now trades at valuation levels that already assume a large portion of the AI opportunity materialises. Even so, the company emerging from this announcement is fundamentally different from the one investors analysed a year ago. The bear case centred on weak economics, persistent cash burn and balance-sheet pressure. Those concerns have become much harder to defend after management presented a framework built around customer-funded expansion, materially higher margins and substantial free cash flow generation.

Figeac Aéro (FGA France): Investing today to expand tomorrow

Figeac’s actions might be easy to misread. The company is increasing capital expenditure and reducing near-term free cash flow expectations. That normally raises concerns, particularly in an industry where investors have become more focused on cash generation after years of heavy investment cycles. Looking more closely, the decision appears driven by opportunity rather than necessity. Management plans to invest an additional €20-30m before March 2028, split roughly between civil aerospace, defence and acquisitions. More importantly, the criteria attached to these projects are significantly stricter than in previous cycles. Management is targeting payback periods of three to four years, compared with five to seven years historically, and expects returns comfortably above its existing profitability targets. The overall message is that demand conditions and customer discussions are creating opportunities that management believes justify accelerating investment.

The underlying aerospace business remains in a favourable position. The company sits at the intersection of several production ramps that still have years to run. Airbus continues to increase output of the A320 family, while the A350 mix is gradually becoming more attractive as the larger -1000 variant and freighter versions gain weight within the programme. LEAP engine production remains another important driver as Boeing works through the 737 MAX recovery and Airbus continues pushing narrowbody volumes higher. Defence is emerging as an additional growth pillar. The current numbers do not fully reflect the potential contribution from programmes linked to companies such as Safran, Thales and KNDS, nor do they include the impact of larger contracts currently under discussion.

Some of these opportunities could extend visibility well into the next decade. As a result, the company’s medium-term targets may prove conservative if a portion of this pipeline converts into production work. What is notable is that management has not yet incorporated much of that potential into formal guidance, suggesting further updates may arrive over the next year.

The market appears focused on the temporary reduction in free cash flow and is paying less attention to what the balance sheet could look like several years from now. Even after the additional investment programme, leverage is still expected to decline from around 3.4x EBITDA at the end of fiscal 2026 to below 1x by 2030. That trajectory is supported by rising earnings rather than financial engineering. At the same time, the company retains an additional element that few aerospace suppliers can offer.

Founder Jean-Claude Maillard continues to prepare for an eventual exit and has reiterated plans to appoint an adviser ahead of a potential sale process by 2028. Recent aerospace transactions have taken place at materially higher valuation multiples than where Figeac currently trades. The stock changes hands at roughly 7x forward EBITDA despite occupying a strategic position within major aircraft programmes and operating in a sector where consolidation remains active. Investors may need to wait for updated long-term targets before the market fully recognises the opportunity, but the current valuation leaves considerable room for a different outcome than the one implied by today's share price.