Weapons, AI Infra and some losers

Flughafen Wien, Ubisoft, AT&S, Strabag, Swiss Life, Czechoslovak Group, Euronext, EFG, Pfisterer, CFE, EDP, Hornbach

At Lux Opes, we break down the latest company news into quick takes that get straight to the point - what happened, why it matters, and what to watch next.

We publish 2-4 times per week, depending on the news flow.

If you want to make sure you always receive Lux Opes in your main inbox, please drag this email into your Primary tab or add this address to your contacts.

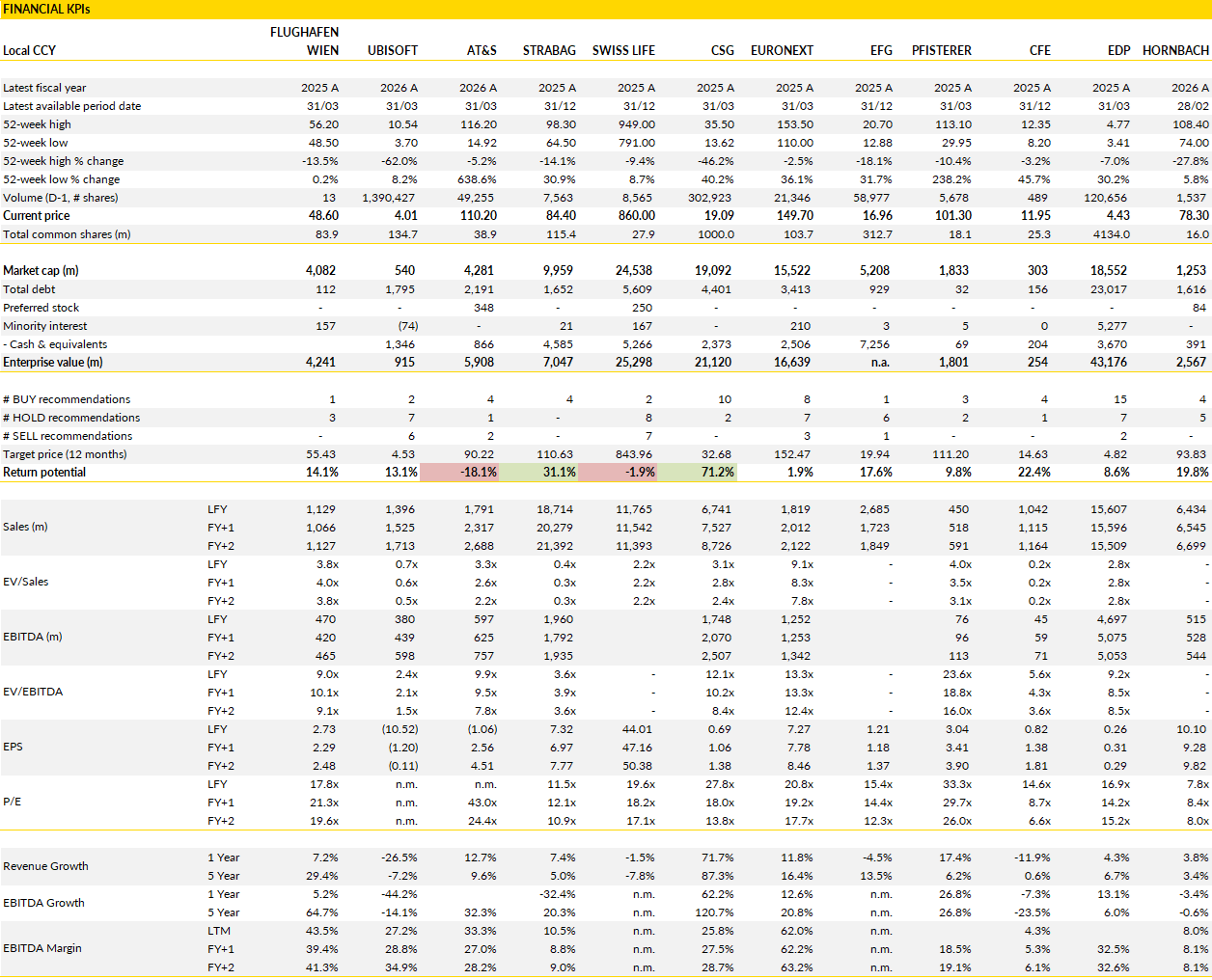

Financial KPIs

Flughafen Wien (FLU Austria): strong start to 2026, but summer traffic trends need monitoring

Flughafen Wien opened 2026 with a solid Q1 supported by resilient passenger traffic and continued strength in non-aviation revenues.

Revenue increased 6% year on year to €240m, ahead of market expectations, helped by passenger growth at Vienna Airport of 1.6%, stronger retail activity, higher de-icing income and the absence of incentive programmes that affected the comparison base last year. EBITDA reached €87.9m, up from €81.3m a year earlier, while the EBITDA margin improved 70bp to 36.7% following ongoing efficiency measures and disciplined operating costs. EBIT came in at €54.4m and EPS at €0.44.

The quarter confirms that Flughafen Wien continues to benefit from stable travel demand and the increasing contribution from commercial activities across the airport platform. Free cash flow declined to €3.8m versus €6.4m last year, mainly due to capex increasing to €85.8m from €66.6m and higher tax payments. Operationally, the company remains in good shape and continues to generate healthy profitability despite a more uncertain macro and geopolitical backdrop.

Management reiterated full-year guidance despite growing uncertainty around Middle East traffic flows and softer trends from some low-cost carriers. The company still expects around 30m passengers at Vienna Airport and roughly 41.5m across the group in FY26. Financial guidance was also maintained, with revenue expected at €1.05bn, EBITDA at €415m and net income at €185m.

So far, stronger traffic to Western Europe and the Far East has compensated for weakness on Middle Eastern routes, although April traffic trends already showed some moderation. Capex guidance remains high at €330m as Flughafen Wien continues investing in infrastructure and long-term capacity expansion. The business remains supported by a diversified route network, exposure to premium traffic and a commercial mix that has become more resilient over the past few years. This combination continues to support margins even when passenger growth becomes less dynamic.

The question for the second half of 2026 is how much softer airline capacity and geopolitical uncertainty will weigh on travel demand during the peak summer season. Flughafen Wien has demonstrated over recent years that it can manage costs effectively and protect profitability during volatile traffic periods. Commercial income streams such as retail, parking and services also provide an additional earnings buffer.

At the current valuation, however, the market already recognises much of that operational resilience (despite the recent derating). Future upside likely depends on whether passenger growth stabilises above current assumptions and whether the airport can continue expanding margins despite slower traffic momentum.

The broader investment case remains intact, supported by solid infrastructure assets, healthy balance sheet metrics and long-term passenger growth trends in Central and Eastern Europe, but near-term momentum certainly looks less straightforward than it did at the start of the year.

Ubisoft (UBI France): slugging along

Ubisoft’s FY 2026 results were in line with the major profit warning issued in January, and they underline how deep the reset still is.

Revenue fell 17% to €1.53bn, matching the revised guidance. Operating losses reached €1.05bn and net losses €1.48bn, both broadly consistent with the warning. Free cash flow was heavily negative at -€443m. The January warning had already flagged the drivers: a reshaped release pipeline, postponed partnerships and a €650m impairment tied to cancelled developments and extended production timelines on titles with lower expected returns.

At year‑end, non‑IFRS net debt stood at €187m, helped by the €1.16bn cash injection from Tencent in exchange for a 26% stake in a joint venture housing the three flagship franchises. Even with this support, the balance sheet remains tight.

FY 2027 is set to be another difficult year. Management expects revenue to decline at a high‑single‑digit rate, reflecting a limited slate of new releases and continued investment ahead of the larger FY 2028 lineup. The operating margin is expected to remain negative in the high‑single‑digit range, implying another sizeable operating loss. Free cash flow is again guided to be deeply negative, potentially reaching -€500m. The company has €1.35bn in cash, which covers the €470m maturity in November 2026, but options are still being evaluated for the €675m maturity in November 2027.

The first signs of recovery are only to be seen from FY 2028 onward (hopefully). Ubisoft points to a more robust and diversified content pipeline anchored by Assassin’s Creed, Far Cry and Ghost Recon, alongside continued momentum in live services such as Rainbow Six Siege. Restructuring efforts are ongoing, with a targeted fixed‑cost reduction of €175m by FY 2028, equivalent to a 12% cut versus FY 2026. Management expects a return to positive operating income and positive free cash flow from FY 2028, with cumulative free cash flow turning positive over FY 2027–2029.

Ubisoft needs time to rebuild its ability to deliver consistent hits, restore profitability and generate sustainable cash flow - though this is hardly news. With the business still in a heavy reorganisation phase and the balance sheet under strain, the near‑term risk‑reward remains unattractive.

AT&S AG (ATS Austria): AI demand keeps the cycle hot, but valuation has moved even faster

AT&S delivered Q4 2025-26 results that were broadly in line with market expectations, although the market reaction is likely influenced more by positioning and valuation than by the actual numbers.

Q4 sales reached €477m, up 21% year on year and up 33% adjusted for FX, slightly ahead of consensus. EBITDA came in at €121m with a 25.4% margin, modestly below expectations, while EBIT of €31.7m was effectively in line. For the full year, revenue reached €1,791m against prior guidance of around €1.7bn, while EBITDA came in at €418m for a 23.3% margin. Operating cash flow remained strong at €414m, capex was lower than expected at €179m and the equity ratio improved to 23%. Cash declined sequentially to €738m as the company continued funding expansion projects. Management again proposed no dividend distribution, which underlines that capital allocation remains fully focused on growth investments and balance sheet flexibility during this phase of the cycle.

The operational backdrop remains exceptionally supportive. Demand linked to AI infrastructure, advanced CPUs and ABF substrates continues to drive tight supply conditions across the semiconductor ecosystem. AT&S is one of the more leveraged European names to this theme through its exposure to high-end substrate manufacturing. Management now guides for FY2026-27 revenue growth of 30-35% on a currency-adjusted basis with an EBITDA margin between 25% and 29%. That implies another major step up in scale and profitability.

The company also announced plans to further expand capacity in Chongqing, with investments in the high double-digit million euro range that are already backed by long-term agreements. AT&S expects these investments to contribute a high double-digit million euro EBIT benefit already in FY2026-27. At the same time, capex guidance increases sharply to around €400m versus consensus closer to €288m. Management also indicated that it is evaluating the issuance of hybrid convertible and/or hybrid bonds of up to €500m combined, highlighting that balance sheet optimisation remains part of the financing strategy as expansion accelerates.

The broader discussion now is on how much of the AI upside is already reflected in the share price. Since the last results, the stock has rallied around over 170%, pushing valuation multiples well above historical averages. On current estimates, the shares trade around 31x 2027 EBIT. That leaves little room for execution issues, cyclical pauses or slower AI infrastructure spending.

There is likely still conservatism embedded in management guidance given current industry conditions, especially around AI-related shortages and substrate demand, but expectations have also become significantly more aggressive after the recent move in the stock. The company clearly benefits from one of the strongest structural themes in global semiconductors, though the valuation now assumes that current industry conditions remain favourable well into the medium term.

STRABAG (STR Austria): resilient demand across core regions

Strabag’s Q1 2026 trading statement offers a clearer and more constructive picture than many would have expected heading into a winter‑affected quarter.

Output rose 4% to €3.87bn despite cold weather in Austria, Poland and parts of Germany. That alone is notable, because the company typically sees a meaningful seasonal drag in Q1, and internal expectations were for flattish development at best. The performance was driven by a strong contribution from the North and West region, where output grew 10% to €1.69bn, supported primarily by Germany’s continued momentum in infrastructure and building construction. The South and East region delivered 5% growth to €1.18bn, helped by solid activity in Czechia, Croatia and Slovenia, which more than offset softer conditions in Austria and Poland. The International and Special Division declined 5% to €0.96bn, reflecting a base effect from real estate development rather than a deterioration in underlying demand.

The order book remains one of Strabag's key strengths. The backlog reached €33.06bn, up 18% year on year and broadly in line with expectations. What stands out is the implied order intake of €5.56bn, which is roughly 10% above internal estimates and results in a book‑to‑bill ratio of 1.44x.

This is a healthy signal for the rest of the year, especially given the company’s disciplined bidding strategy. Activity was particularly strong in the Americas, where Strabag secured a large mining contract in Chile, and in core European markets such as Austria, Germany and Czechia. By division, North and West rose 3% to €13.56bn, South and East was stable at €8.61bn and the International and Special Division surged to €10.87bn, reflecting the contribution of large‑scale projects.

Management confirmed full‑year guidance, which was widely expected. Strabag continues to target output of around €22bn and an EBIT margin of 5.0% to 5.5%. Current estimates remain more optimistic, with output of €22.2bn and a margin of 5.8%, implying EBIT of €1.20bn. These forecasts also sit above the broader market view, which remains closer to €1.11bn and a 5.4% margin. The company also raised its outlook for net investments by €100m to up to €1.5bn, reflecting an expanded M&A pipeline and continued confidence in long‑term demand.

Overall, the Q1 statement shows strong operational momentum, a diversified regional footprint and a robust order book that provides visibility well into the year. The combination of better‑than‑expected output, healthy order intake and stable guidance supports a constructive outlook for 2026, with Strabag well positioned to benefit from ongoing infrastructure demand across Europe and selected international markets.

Swiss Life (SLNH Switzerland): the fee engine keeps compounding while investment income cools off

Swiss Life started 2026 with another solid quarter operationally, even if market reaction may end up relatively muted because most of the strength came from areas investors already expect to perform well.

Premiums increased 5% in local currency to CHF 8.2bn, slightly ahead of market expectations, while fee income rose 6% to CHF 686m. Swiss Life continues to steadily shift its earnings mix toward capital-light activities with higher visibility and lower balance-sheet intensity. Asset management, advisory services and fee-based products are gradually becoming more important contributors to profitability. Switzerland again stood out, with premiums rising 10% to CHF 5bn and comfortably ahead of expectations. France was softer on headline premium growth because of a tougher comparison base, though the quality of business continued to improve. Unit-linked products represented 73% of sales in France during the quarter, showing that Swiss Life is still pushing customers toward products with lower capital consumption and structurally better economics for the group.

Asset Managers also delivered another healthy quarter. Third-party assets under management increased to CHF 148bn while net new money reached CHF 4.2bn, ahead of consensus despite facing a demanding comparison against last year. Fee income within the asset management division remained strong and total income rose 12% year on year. This part of the business increasingly matters for the investment case because it provides a more recurring and scalable earnings stream compared with traditional life insurance operations.

Management continues to point toward the “Swiss Life 2027” targets and nothing in this release suggests execution issues so far. The acquisition of TELIS in Germany fits directly into that strategy as well. Adding roughly 1,800 advisors strengthens Swiss Life’s position in one of Europe’s more fragmented financial advisory markets and pushes pro forma annual fee income in Germany above €1bn. Advisory and wealth planning remain structurally attractive areas for the group because they deepen customer relationships while requiring significantly less balance-sheet risk than traditional guaranteed products.

The only real weak point in the quarter came from investment income. Income declined to CHF 942m from CHF 1.08bn a year ago and came in below expectations due to weaker contributions from infrastructure, equities and foreign exchange movements. This matters because Swiss Life still depends heavily on investment returns to support overall profitability, even if fee income is becoming a larger part of the story. The direct investment yield of 0.7% was softer than hoped, though the capital position remains extremely strong with an SST ratio around 210%, comfortably above management’s target range. The ongoing CHF 750m share buyback also continues as planned.

Overall, this was another quarter showing a business that is becoming steadier, more diversified and more fee-oriented over time. The issue for investors is that much of this progress is already well understood, leaving limited room for estimate revisions or multiple expansion unless earnings growth starts to accelerate more visibly.

Czechoslovak Group (CSG Netherlands): a solid Q1 and early steps toward rebuilding credibility

CSG’s Q1 update and management’s direct engagement with investor concerns mark an important shift in tone after months of pressure from short sellers and a sharp post‑IPO derating.

The company used the conference to address two of the most sensitive topics: in‑house production capacity in medium and large‑calibre ammunition, and the role of minority interests across the group. On ammunition, management reported that annualised in‑house output reached the equivalent of 800,000 units by the end of Q1, with a medium‑term target of 1.1 million supported by ongoing expansions in Slovakia and India. This matters because the M/L Ammo division’s 22% revenue growth and 32% EBIT margin in Q1 were driven primarily by the ramp‑up of internal production rather than re‑commissioning activities, which had been a point of scepticism.

The product mix also remains favourable, with long‑range ammunition accounting for roughly half of the division’s output. On minority interests, which represent around 10% of the group, management emphasised that financial and governance risks are limited, with no commitments that directly involve the parent company. The minority share of profit is expected to be around €150m in 2026.

Operationally, Q1 was solid. Group revenue rose 13.8% to €1.54bn, driven by a strong performance in defence systems, which grew 26.5% year on year. Ammo+ remained the weak spot, with revenue down 20.5% due to the ongoing softness in the US civil market. Pre‑PPA EBIT increased 8.7% to €372m, corresponding to a margin of 24.1%, down 120bp year on year. The margin pressure came almost entirely from Ammo+, where profitability fell to 4.3% from 10.9% in Q1 2025. Free cash flow was slightly positive at €6m, which is a respectable outcome given the working‑capital intensity of the business.

CSG confirmed its 2026 guidance, with revenue expected between €7.4bn and €7.6bn and an EBIT margin of 24% to 25%. Visibility appears satisfactory, supported by a 15% sequential increase in the order book to €17bn and a book‑to‑bill ratio expected to exceed 1.5x for the year.

The company also expressed confidence in a recovery in Ammo+. After a very weak start to Q1, order volumes rebounded by 50% from late February, and two price increases are planned to offset input inflation, particularly in copper. For 2026, CSG is targeting incremental revenue of €250m to bring the division back to 2024 levels, with a return to double‑digit post‑PPA margins. This is expected to be supported by normalising US civil demand and the ramp‑up of defence and law‑enforcement contracts. Even so, visibility remains limited, and a cautious stance on Ammo+ still feels appropriate. For now, assuming only marginal revenue growth in 2026 remains prudent.

The conference was a meaningful step in restoring investor confidence after a share price decline of more than 40% since the IPO. Management’s willingness to address concerns directly, combined with solid operational delivery and a growing order book, helps rebuild credibility. At the same time, further proof points are needed: consistent execution on the ammunition ramp‑up, conversion of the pipeline into firm orders, and resolution of recent controversies involving subsidiaries or contract negotiations.

The valuation remains undemanding relative to peers, and the medium‑term growth profile is supported by structural defence demand, but the equity story still requires disciplined delivery over the coming quarters.

Euronext (ENX France): volatility cycle meets a stronger structural story

Euronext delivered one of its strongest quarterly prints in recent years, with the key point being that the beat was not dependent on a single trading spike or one-off event.

Revenue increased 15.3% year on year and came in 3% ahead of expectations, marking the eighth consecutive quarter of double-digit growth. The quality of that growth also stood out. Trading activity was obviously strong as volatility returned across European markets, but the non-volume businesses also contributed meaningfully. Equity trading, ETFs and derivatives all benefited from elevated market activity, while Securities Services, market data and custody-related activities continued to grow steadily in the background. The Greek exchange again performed particularly well and continues to become a more relevant contributor inside the group.

What investors increasingly seem to appreciate is that Euronext no longer behaves purely like a cyclical exchange operator tied to cash equity volumes. The business mix has become broader, more diversified and structurally more predictable over time through post-trade, data, fixed income and clearing activities.

The operational leverage in the model was again fully visible in Q1. Underlying operating costs came in below expectations while adjusted EBITDA margins expanded to almost 65%, a record level for the company. Exchanges naturally benefit from fixed-cost infrastructure, so periods of elevated market activity can drive profitability sharply higher without requiring significant incremental spending. Still, the cost discipline deserves attention because management continues to execute consistently against guidance while leaving room for upside. If the Q1 cost base were annualised, it would already sit below the company’s full-year guidance.

It is probably too early for analysts to materially revise forecasts after one quarter, particularly because volatility-driven activity can reverse quickly, but the setup for upgrades later this year is clearly there if volumes remain healthy into the second half. Net profit ended up 8.5% ahead of consensus expectations, which is unusually strong for a company that already entered the quarter with elevated expectations.

The broader strategic story also continues to improve. Euronext spent the last several years building scale across Europe through acquisitions and integration work, and the market is finally beginning to see the benefits show up more clearly in the numbers. The combination of structural post-trade growth, clearing expansion, stronger data revenues and periodic trading volatility creates a more attractive earnings profile than the market historically assigned to the company. Management continues to push organic investment initiatives while keeping the door open for further consolidation opportunities across European market infrastructure.

At around 18x NTM earnings, the valuation no longer looks cheap in absolute terms, but it still does not fully reflect a business now capable of delivering low-teens earnings growth with expanding margins and rising cash generation. The key difference versus earlier years is that Euronext now looks far less dependent on one specific market environment. The platform has become broader, more integrated and operationally stronger, which gives the group more resilience across cycles while still allowing it to benefit heavily when volatility returns to markets.

EFG International (EFGN Switzerland): steady business momentum, solid capital generation

EFG’s first four months of 2026 show a franchise that continues to deliver stable growth in assets, disciplined cost control and healthy capital generation despite a more volatile market backdrop.

Net new assets reached CHF 3.7bn, corresponding to an annualised growth rate of 6%, which sits at the upper end of the group’s 4–6% target range. This is fully in line with expectations and confirms that client activity remains robust. The bank also continued its push to expand its front‑line capacity, hiring 25 new client relationship officers over the period, with another 26 either signed or under offer. Even so, the total CRO count slipped slightly from 763 at year‑end to 761 at end‑April, reflecting normal attrition. Assets under management rose 2.8% to CHF 190.2bn, a touch below expectations due to a softer‑than‑anticipated market effect, but still up nearly 20% year on year.

Revenue quality remains stable. The revenue margin was 93bp, down from 97bp in the same period last year but unchanged from the second half of 2025. The year‑on‑year comparison is distorted by unusually strong interest‑rate tailwinds in early 2025. The margin also includes a roughly 2bp contribution from insurance, linked to the final settlement of outstanding claims. Costs were well managed, with a cost‑income ratio around 70%, slightly better than the same period last year and a meaningful improvement from 73.1% in the second half of 2025. This also compares favourably with consensus expectations. Net income for the first four months exceeded CHF 130m, broadly in line with the prior year, translating into an annualised return on tangible equity above 23%.

Capital generation was another highlight. CET1 rose to 14.7% at end‑April, up from 14.0% at year‑end and ahead of expectations. The increase reflects strong operational capital generation and positions the bank comfortably ahead of regulatory requirements. The acquisition of Quilvest Switzerland is expected to close in the third quarter of 2026, and on a pro forma basis would bring AuM to CHF 194bn.

Overall, a business that is executing consistently. Net new assets remain strong, revenue margins are holding up despite a normalising rate environment, and cost discipline is improving. Capital ratios continue to strengthen, giving the group strategic flexibility as it integrates Quilvest and continues to expand its front‑line capacity.

Pfisterer (PFSE Germany): strong Middle East momentum carries another quarter

Pfisterer delivered a strong first-quarter print on the surface, with revenue, EBITDA and EBIT all comfortably ahead of market expectations, though most of the upside again came from one specific part of the business.

Group revenue reached €126.9m, around 5% above forecasts, while adjusted EBITDA increased to €27.7m with margins reaching 21.8%. EBIT came in at €23.6m and EPS reached €0.98, both materially ahead of estimates. The numbers look impressive and continue to support the broader narrative around grid investment, electrification and transmission infrastructure spending. Demand for high-voltage connection technology remains healthy globally and Pfisterer continues to benefit from that structural backdrop.

Still, beneath the headline beat, the quarter was less broad-based than the top-line figures initially suggest. The largest contribution again came from the OHL division, which includes overhead line infrastructure activities and has recently been benefiting from unusually strong project momentum in the Middle East.

The underlying divisional picture was more mixed. High Voltage Applications, still one of the group’s core activities, delivered revenue broadly in line with expectations while margins were slightly softer. Medium Voltage Applications missed modestly on both sales and EBITDA. Communications and industrial applications delivered solid profitability, though without major surprises operationally. The real standout remained OHL, where revenue reached €35.6m versus expectations closer to €28m, while EBITDA surged to €10.1m with margins approaching 29%. That is exceptionally high profitability for this type of business and likely reflects a combination of project mix, execution timing and regional dynamics tied to the Middle East buildout cycle.

The issue for investors is that this part of the business may prove harder to extrapolate over multiple years at the current level. Management itself already hinted that order momentum in OHL is beginning to normalise somewhat on a year-on-year basis, even if activity remains strong overall. At the same time, free cash flow remained negative at -€8.8m, somewhat weaker than expected due mainly to operating cash-flow dynamics.

Order intake itself was broadly fine without showing major acceleration. New orders reached €131.1m, slightly above expectations and still ahead of quarterly sales, which supports the near-term growth outlook. Management reiterated guidance for at least 12% revenue growth in 2026 alongside a book-to-bill above 1x and medium-term EBITDA margins in the high teens to low twenties.

Structurally, the company remains well positioned given the ongoing investment cycle in power grids, renewable integration and transmission infrastructure. Electrification themes across Europe, the Middle East and North America continue to support long-term demand visibility.

The challenge now increasingly sits with valuation. After the recent share-price rally, Pfisterer trades at well above 20x forward EBIT, which already prices in a large portion of the expected growth and margin improvement. Investors clearly see the company as a leveraged play on grid infrastructure spending, but sustaining current multiples will likely require stronger order acceleration outside the OHL business and more evidence that profitability can remain elevated across the broader portfolio.

CFE (CFEB Belgium): a cleaner contract mix

CFE’s Q1 update shows a group that is gradually reshaping its business toward segments with better pricing power and more predictable returns.

Revenue grew 2% year on year to €266.7m, a modest headline number but one that masks meaningful differences across divisions. Real Estate Development fell 18% to €13.7m, which is not surprising given the deliberate reduction in capital employed and the focus on selling down completed units. Unsold inventory dropped to just €4m from €10m at year‑end, and capital employed in the segment remains tightly controlled at €224m. Marketing of properties under construction is progressing well, suggesting that the division is moving toward a leaner, more selective model.

Multitechnics was the clear bright spot, with revenue up 21% to €83m. VMA grew 22% to €61.2m and MOBIX, the rail business, rose 20% to €21.8m. Activity was particularly strong in electricity and HVAC, where demand remains resilient. Market conditions in industrial end‑markets, especially European automotive, remain challenging, but the division’s performance shows that CFE is gaining traction in areas where technical expertise and integrated solutions command better margins. Construction and Renovation declined 3.7% to €173m, with strong growth in Luxembourg offset by weaker activity in Belgium and Poland.

The investment portfolio continues to develop steadily. Rentel and SeaMade benefited from better wind conditions, supporting stable cash generation from offshore wind. Deep C in Vietnam is progressing with the development of its five industrial zones, although the conflict in the Middle East and the closure of the Strait of Hormuz are creating logistical and commercial headwinds. Even so, service‑related revenue is expected to continue growing at a solid pace. GreenStor reached an important milestone with the commissioning of the 50 MW D‑Stor battery park in La Louvière in April, and the 100 MW Aubange project remains on track for completion in the fourth quarter.

The balance sheet remains healthy. Net cash increased to €48.3m from €43.8m at year‑end, and the proposed dividend of €0.50 per share, representing a yield of roughly 5%, reflects confidence in the group’s cash‑flow profile. The stock goes ex‑dividend on 21 May.

The order backlog declined 4.9% to €1.55bn, driven by normal seasonality and the timing of new awards. Multitechnics’ backlog slipped slightly to €316.8m, but several major orders are expected shortly. Construction and Renovation ended the quarter with €1.23bn in backlog, supported by new wins such as the renovation and extension of the British School of Brussels and a shopping centre project in Poland.

CFE maintained its 2026 outlook, although it flagged that Deep C could face further pressure if the disruption linked to the Strait of Hormuz persists. In short, operational resilience and a more selective approach to contracting, which is beginning to translate into better returns.

EDP (EDP Portugal): Brazil exit sharpens the split between the parent and the renewables arm

The sale of EDP Renewables Brasil from EDPR to EDP is one of those intra-group transactions that says quite a lot about how both companies are now positioning themselves strategically.

EDPR agreed to sell its entire Brazilian renewable platform to EDP Brasil for roughly R$4.1bn, implying an enterprise value close to €1.5bn. The portfolio includes 1.8 GW of installed capacity split between onshore wind and solar assets. On paper, the deal mainly reflects EDPR’s decision to narrow its geographic focus and concentrate capital on the US and Europe, where management currently sees better visibility, stronger long-term returns and more supportive regulatory frameworks. Brazil had already disappeared from EDPR’s 2026-2028 growth plans, so this transaction effectively formalises a strategic retreat from a market that has become increasingly difficult for large-scale renewable development given weaker power pricing dynamics and oversupply concerns.

From EDPR’s perspective, the transaction is mostly about simplification, balance-sheet flexibility and portfolio quality. Management estimates the deal should improve earnings modestly through lower debt costs and better capital allocation efficiency. The group’s EBITDA exposure to A-rated countries will also rise to roughly 95% after completion, up from around 90% previously, which fits the broader effort to improve the company’s risk profile after a difficult few years for the renewable sector.

Investors have increasingly demanded discipline from renewable developers, particularly around capital intensity, leverage and project returns. EDPR now appears more focused on recycling capital, protecting returns and avoiding regions where pricing conditions are deteriorating structurally. The valuation itself looks broadly fair depending on which metric investors prioritise. On a MW basis, the implied valuation appears somewhat conservative relative to recent transactions in wind and solar. On EBITDA multiples, however, the deal sits slightly above recent averages at around 15x expected 2027 EBITDA. That probably reflects the operational quality of the portfolio and the strategic nature of the buyer, even if growth prospects in Brazil are currently muted.

For EDP, the logic is different. The parent company is effectively consolidating more generation capacity inside Brazil at a time when the local power market is gradually liberalising and becoming more integrated across generation, distribution and supply activities. Strengthening that upstream-downstream structure gives EDP Brasil greater flexibility in managing pricing, customer relationships and power flows across the system. Brazil remains an important market for the parent despite the more challenging outlook for standalone renewable expansion projects.

The transaction also highlights the increasingly different profiles between EDP and EDPR. EDP continues to look like the steadier and more diversified utility story, supported by regulated activities, integrated operations and cash generation across multiple markets. EDPR remains more exposed to sentiment around renewable valuations, power pricing and capital markets conditions. That divergence increasingly explains why investors are showing more interest in the parent than the renewables subsidiary.

The renewable growth story still exists, particularly in the US and Europe, but the market is clearly demanding stronger returns, tighter capital discipline and better free cash flow conversion than it did during the sector’s earlier expansion phase.

Hornbach (HBH Germany): market-share gains continue but the macro backdrop still caps enthusiasm

Hornbach delivered a solid set of full-year results that largely confirmed what investors already knew from the preliminary release in March: the business is holding up well operationally despite a weak consumer and construction backdrop across much of Europe.

Revenue increased 3.8% to €6.4bn while EBIT declined slightly to €265m, leaving operating margins at 4.1%. Net income slipped modestly to €144m. None of those numbers are particularly spectacular on their own, but the more interesting point is that Hornbach continues to gain market share in several key markets even during a period where DIY spending and construction activity remain under pressure. Germany improved to 15.7% market share, while the Netherlands, Austria, Switzerland and the Czech Republic all moved higher as well. That says quite a lot about the strength of the group’s positioning. Hornbach’s combination of pricing discipline, broad assortment and integrated online-offline model continues to resonate with customers while weaker competitors struggle with traffic and margin pressure.

Operationally, the business remains fairly well controlled. Gross margins actually improved slightly to 35% thanks to stable pricing, better product mix and easing raw-material pressure. The issue sits further down the P&L where operating costs continue to rise. Wage inflation, logistics expenses and expansion-related costs, including the opening of Serbian operations, all weighed on profitability. Still, the margin decline was relatively limited considering the broader environment. Cash generation also stayed healthy. Free cash flow increased to €123m despite capex reaching €220m, helped by disciplined working-capital management. Net debt remains manageable with leverage at 2.8x EBITDA including lease liabilities.

E-commerce also continues to grow gradually and now represents 12.7% of sales. That is not transformative on its own, but it reinforces the idea that Hornbach’s hybrid retail approach is functioning effectively without damaging store productivity. Unlike some competitors, the company never overextended aggressively into online retail at the expense of profitability.

Management’s guidance for FY 2026-27 was predictably cautious. The company expects revenue growth somewhere between -2% and +6%, with EBIT potentially moving either direction by up to 5%. That wide range reflects how little visibility still exists around European consumer spending and construction activity. Housing markets remain sluggish in Germany and financing conditions are still constraining renovation and new-build demand across several regions.

Even so, Hornbach appears to be entering this phase from a relatively strong competitive position. The company continues opening new stores selectively, with locations planned in Slovakia, Austria and the Netherlands, while avoiding overly aggressive expansion. Investors probably hoped for a more optimistic tone given improving sentiment in parts of Europe during recent months, but management clearly prefers to stay conservative for now.

At roughly 9x forward EV/EBIT, the stock trades close to its historical average valuation, which probably explains why the market reaction to these results may stay relatively muted. Hornbach is executing well, taking share and protecting margins reasonably effectively, but the broader recovery in DIY and construction demand still looks gradual rather than explosive.