Fitness clubs, fashion and parcel lockers

Hugo Boss, Basic-Fit, Inditex, Eramet, Aurubis, Wavestone, Pierre & Vacances, STMicroelectronics, Zumtobel, Quadient, Airbus, Bilfinger

At Lux Opes, we break down the latest company news into quick takes that get straight to the point - what happened, why it matters, and what to watch next.

We publish 2-4 times per week, depending on the news flow.

If you want to make sure you always receive Lux Opes in your main inbox, please drag this email into your Primary tab or add this address to your contacts.

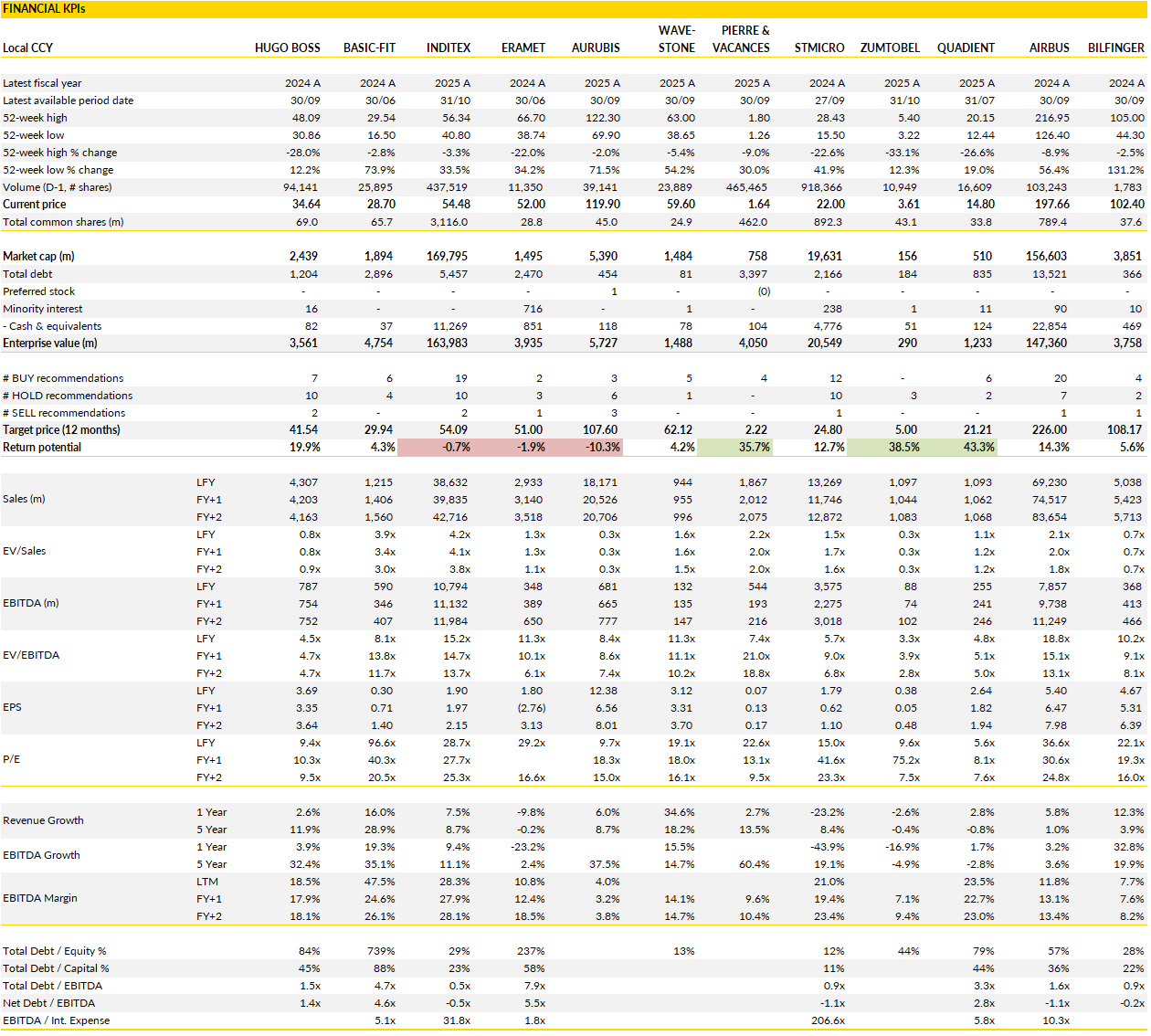

Financial KPIs

Hugo Boss AG (BOSS Germany): a step back

Hugo Boss is treating 2026 as a reset as the company takes a deliberate step back to fix what it broke during its rapid post-pandemic growth phase.

Management’s new strategic update calls for a year of realignment, with a sharper focus on execution, cash generation, and efficiency rather than chasing headline growth. Currency-neutral sales are now expected to fall mid to high single digits next year, while EBIT will dip to around €300–350 million from roughly €380 million in 2025. It’s a reset built on discipline: lower capital spending, tighter working capital, and leaner inventories should all help free up roughly €300 million in annual free cash flow after leases.

Overall a clear message: Hugo Boss seeks to restore its operational muscle before stepping on the accelerator again in 2027 and 2028.

The plan also reflects a more granular rethink of the brand architecture. Management will split BOSS menswear and womenswear into distinct business lines, while repositioning HUGO as a more accessible, fashion-forward label. This separation is a bid to revive product clarity and creative differentiation that had blurred as the group chased scale. On the distribution side, Hugo Boss is closing around 50 standalone stores through 2028, while doubling down on strategic wholesale partnerships and selective franchise expansion. The idea here is to channel investment into fewer, stronger retail locations and rebuild brand desirability.

Meanwhile, management sees underpenetrated growth opportunities in the U.S. and China, where market shares remain a fraction of what Boss enjoys in Europe, but execution there will require patience and local adaptation.

The tension in this plan lies between the short-term austerity and long-term ambition. Cutting capex and operating costs will certainly lift cash flow metrics, but risks starving the brand of energy at a time when fashion cycles are moving faster and competitors are aggressively investing in visibility and design. CEO Daniel Grieder’s refusal to prioritize M&A makes sense for now, given the company’s balance sheet focus, but it also underscores that the next growth leg must come from internal renewal.

After several years of volatility, Hugo Boss is choosing consolidation over growth, a sensible move for a brand that needed to catch its breath. Whether investors can stay patient through a (deliberately?) quiet 2026 will depend on how convincing the eventual rebound in 2027 proves to be.

Basic-Fit (BFIT Netherlands): flexing scale and structure with the Clever Fit deal

Basic-Fit’s acquisition of Clever Fit marks more than just a geographic expansion, it’s the company’s move from regional dominance to continental scale.

After years of organic growth and standardised rollout, the Dutch gym operator is now using M&A to accelerate its footprint in Germany, a market where it previously lacked density and brand awareness. The recently closed deal gives Basic-Fit immediate scale across the country, with hundreds of franchise locations that provide a ready-made platform for further expansion. At an analyst meeting this week, management finally filled in the details we were waiting for: the dual-brand strategy, conversion options for franchisees, and the operational synergies that make the acquisition far cheaper than it first appeared.

Rather than forcing a uniform transition, Basic-Fit will keep both brands alive for now; Clever Fit for existing franchisees who prefer to stay independent, and Basic-Fit for those willing to convert and integrate into its high-efficiency platform. The choice comes with clear incentives: a “light” conversion option for minimal branding and a “premium” version for full integration into Basic-Fit’s IT, monitoring, and national marketing network.

The latter is the real strategic play, as it creates network effects, data visibility, and scale-driven cost advantages that franchisees can’t replicate on their own. Early signs are promising: about 80% of the pipeline of soon-to-open Clever Fit gyms are already opting to switch. And because Basic-Fit’s own infrastructure replaces many of Clever Fit’s outsourced IT and service costs, the effective acquisition multiple drops sharply once synergies kick in.

What makes the Clever Fit acquisition intriguing is how it redefines Basic-Fit’s growth model. It turns Germany into a lever rather than a drag, and introduces franchising scale without the capital intensity of company-owned gyms. It also sets a precedent for similar “hybrid” expansions elsewhere, where Basic-Fit can leverage its technology and brand while leaving local ownership intact.

Management’s focus on efficiency, standardisation, and cost discipline remains intact, but now paired with a more flexible capital model that could extend its European lead. If the integration goes smoothly, and early franchisee enthusiasm is a good sign, Basic-Fit may have just found the template for its next growth cycle: lighter balance sheet, broader reach, and deeper margins.

Inditex (ITX Spain): steady margins, strong momentum, and no sign of slowing down

Inditex’s third quarter results offered exactly what investors like about the company: consistency, control, and clear dominance.

Sales rose 5% year-on-year to just under €9.8 billion, modest on the surface but underpinned by a healthy 8% constant-currency growth rate that outpaced peers once again. Margins expanded meaningfully, with gross margin climbing to 62.2% and EBIT margin up 140 basis points to 24.2%, showing how pricing discipline and operational leverage continue to work in tandem. The company’s formula remains intact: fast fashion delivered efficiently through integrated logistics, with a supply chain nimble enough to manage inventory tightly even as costs fluctuate. November’s trading update (sales up more than 10% at constant exchange rates) reinforces the view that the brief slowdown in early 2025 was more of a pause than a shift in trend.

Where most apparel retailers are grappling with bloated inventories or heavy promotions, Inditex keeps proving its ability to manage cycles from a position of strength. Its in-house production flexibility, tight inventory turns, and global pricing consistency mean that even modest topline growth translates cleanly into profit. The 8% constant-currency revenue growth came alongside improved cost ratios, the rare combo of volume resilience and margin expansion in a sector still digesting inflationary aftershocks. Behind that, the company’s online integration strategy continues to pay off: every store functions as both retail and fulfilment, feeding an ecosystem that scales globally without eroding margins.

Looking ahead, the group’s tone remains measured. Management is sticking to its guidance for 5% net space growth, an unchanged gross margin outlook, and continued efficiency gains. The company’s advantage lies in execution: strong control over sourcing and design cycles, fast feedback loops from store data, and the discipline to grow profitably while others chase volume.

November’s double-digit start to Q4 suggests that momentum will carry into year-end, keeping Inditex comfortably ahead of European peers still struggling with consumer softness.

Eramet (ERA France): housekeeping

Eramet’s long-awaited “decisive actions” turned out to be more housekeeping than headline-grabbing strategy.

The mining group announced a broad productivity and cost-cutting programme, targeting €130–170 million in EBITDA improvement by 2028, a meaningful number on paper but modest relative to the group’s current earnings base. Absent were the more dramatic options that markets had speculated about: no asset sales, no capital increase, and no restructuring that might fundamentally change the group’s financial profile. Management instead framed the plan as a multi-year operational clean-up designed to stabilise cash generation and rebuild margins after a brutal commodity downcycle. Hardly a reset that redefines the story.

The bright spot remains Argentina. The lithium project there continues to ramp up ahead of schedule, reaching 65% utilisation in November and on track to hit full nameplate capacity by late 2026. This asset is increasingly central to Eramet’s narrative, one of the few parts of the portfolio benefiting from favourable market momentum as global battery and storage demand revives. Elsewhere, however, the backdrop remains weak. Nickel and mineral sands remain in the doldrums, while manganese, still the group’s cash engine, faces structural overcapacity and geopolitical uncertainty, particularly in Gabon.

Management hinted that selective disposals could still happen, but in truth, selling cyclical assets into a soft market rarely delivers value. For now, Eramet appears committed to internal self-help.

The challenge is that self-help alone may not be enough to fix the balance sheet. With leverage hovering near 5x and limited earnings visibility in its key commodities, the group’s path to deleveraging looks slow and fragile. The Duval family’s aversion to dilution explains the absence of an equity raise, but it also leaves Eramet more exposed to volatility if markets turn again.

Eramed remains a company with high-quality resources and a credible long-term role in the energy transition, yet still weighed down by short-term financial strain and a patchy commodity mix. The new plan buys time, but not conviction.

Aurubis (NDA Germany): smelting through the noise with solid cash flow and a clear runway

Aurubis closed its fiscal year on a strong note, showing once again why it’s seen as Europe’s copper bellwether.

The Q4 numbers were steady rather than spectacular, but they underscored a company that’s executing cleanly through a volatile market. Operating earnings were in line after adjusting for one-offs tied to environmental provisions and equity write-downs, while free cash flow came in far stronger than expected, a reminder that Aurubis is moving past the peak of its capex cycle. The group generated €115 million in free cash before dividends, cutting net debt to just €222 million, and confirming its reputation for balance sheet discipline even as it continues to invest heavily in growth projects. With the dividend nudging up to €1.60 per share, management is signaling a steady, controlled step into a more profitable 2026.

The operational story is now shifting from cyclical pricing to strategic positioning. Treatment and refining charges (TC/RCs) have softened as global supply dynamics tighten, while sulfuric acid prices remain muted. But Aurubis’ diversified metal mix, with solid contributions from gold, silver, tin, and platinum group metals, continues to buffer earnings. More importantly, the Richmond smelter ramp-up is beginning to crystallize the group’s North American ambitions. That project alone opens a significant new profit pool in the U.S. copper market, where electrification and reshoring trends are intensifying demand. Alongside its European recycling hubs, Aurubis is building a footprint that could make it one of the few integrated copper recyclers operating at global scale. The timing is fortuitous: demand visibility into the green transition remains robust, while the supply response continues to lag.

What stands out most in this update is the combination of operational momentum and financial headroom. The company’s new fiscal guidance, EBITDA of €580–680 million and breakeven free cash flow, suggests the heavy investment phase is ending just as its growth assets begin to contribute.

The valuation looks stretched at first glance, trading above its historical multiple, but the premium is tied to a tangible shift in quality. Aurubis has positioned itself at the crossroads of two major themes, industrial resilience and circular metals, and is executing the handover from capital spender to cash generator with precision.

Wavestone (WAVE France): steady execution through the storm, with recovery signals flickering

Wavestone’s half-year results reinforced the impression of a consultancy that knows how to steer through turbulence. Organic revenue was essentially flat, but the firm managed to protect margins and even grow earnings slightly despite a tough market for discretionary tech spending.

EBIT margin held firm at just over 10%, helped by tighter cost discipline, less reliance on subcontractors, and a leaner overhead structure. The real standout was cash generation: free cash flow swung from near zero a year ago to roughly €20 million, giving Wavestone a positive net cash position even after the usual seasonal drain in the first half. For a sector still pressured by the slowdown in digital transformation projects, that combination of margin stability and liquidity strength looks reassuring.

The company reaffirmed full-year guidance, signaling confidence that the second half will see better momentum as deferred client projects restart. Management expects organic growth to turn positive and margins to rise toward 13%, implying a strong operational rebound in H2. There are tentative signs that demand is improving in consulting areas tied to AI, cybersecurity, and SAP transformation, all categories where Wavestone has built solid domain expertise.

Still, management remains cautious about calling it a full recovery, noting that some of the recent pick-up in demand could reflect budget flush effects at year-end rather than a structural acceleration. For now, the strategy is clear: focus on utilization, secure project pipelines early, and prepare to capture the next wave of digital investment once confidence returns.

Wavestone continues to look like one of the better-quality names in the European mid-cap IT consulting space, i.c. disciplined, diversified, and operationally nimble. The stock trades at a discount to peers despite its record of consistent profitability and a growing foothold in high-value digital niches.

The next catalyst will likely come in early 2026, when visibility on new project spending improves and the company can show whether the recovery in Q3 demand has legs.

Pierre & Vacances (VAC France): steady recovery, solid bookings, and a cleaner balance sheet

Pierre & Vacances closed its fiscal year with a modest EBITDA miss but a business that’s clearly moving in the right direction.

Tourism revenue grew almost 4% and margins held steady despite inflation and a few temporary headwinds, notably refurbishment work and the closure of one Center Parcs site. The cost-cutting plan continues to deliver, lifting underlying profitability even as reported EBITDA of €181 million came in just shy of expectations. More importantly, cash generation improved, leaving the group with €45 million in net cash at year-end, a welcome sight for a company that spent years under restructuring clouds. The model is now much leaner, and the benefits of a refreshed park network and rising average selling prices are starting to show up in the numbers.

The short-term setup looks encouraging. Early bookings for the first half of FY26 are well ahead of last year, covering more than two-thirds of the period’s budgeted revenue target and showing momentum across all brands. Both volumes and pricing are trending positively, a combination that suggests the group’s focus on local, family-oriented tourism still resonates with consumers even as broader European leisure demand cools. With a largely renovated asset base and better digital distribution, Pierre & Vacances has gained more control over pricing and occupancy; a structural shift that helps smooth seasonal swings and supports margin resilience.

Management is keeping its FY26 guidance intact, targeting EBITDA of around €185 million and longer-term ambitions of €270 million by 2030, underpinned by continued portfolio upgrades and operational discipline.

After years of painful turnaround work, the group is emerging as a much simpler, cleaner business with better visibility and capital efficiency. Inflation-linked pricing and lower capital intensity should keep cash flow healthy, while the company’s niche in local and regional tourism offers a defensive edge against macro volatility.

Valuation remains undemanding, reflecting both its cyclical past and lingering skepticism about execution, but the fundamentals now point to steady, incremental progress rather than survival. Pierre & Vacances still has work ahead on brand perception and yield optimization, but the broad direction is good; a once overleveraged leisure operator is becoming a cash-generating domestic tourism platform with room to grow.

STMicroelectronics (STMPA France): gearing up

Microchip’s recent guidance upgrade is a meaningful signal, and one that could bode particularly well for STMicroelectronics.

The U.S. peer’s stronger-than-expected order intake has historically marked early inflection points in industrial demand, given its deep exposure to general-purpose microcontrollers. STM sits right in that slipstream, with roughly a third of its sales tied to the same segment. After a sluggish year marked by destocking and muted industrial orders, any pickup here could quickly translate into leverage on both volumes and margins for STM.

While the short-term narrative will likely be dominated by the usual gross-margin jitters, the medium-term picture is getting clearer, and brighter. Management expects a soft Q1 due to seasonality and fading capacity reservation fees, but growth should reaccelerate in the second half of 2026 as orders recover and pricing stabilizes. Key growth drivers are already visible: Apple-related content gains, a large photonics contract with AWS, and new low-earth orbit satellite programs with Amazon and others beyond SpaceX. STM is also regaining lost share in general-purpose MCUs, especially in China, a market that could act as a tailwind as local inventories normalize. Behind the scenes, cost reductions are accelerating, with several hundred million dollars in targeted savings across opex and COGS, setting the stage for a return to gross margins above 35% by late 2026 and potentially higher in 2027.

This setup creates an unusual mix of value and optionality. Investors are still treating STM as if the cycle never recovers, yet the signs of an industrial upturn are increasingly hard to ignore. The company’s balance sheet remains net cash, its end-markets are broad enough to capture both industrial automation and consumer electronics tailwinds, and its 300mm transition continues to enhance structural profitability.

The risk of short-term volatility around Q1 guidance is real, but that may be precisely when the stock becomes most interesting. As Microchip’s optimism ripples through the sector, STM could easily find itself leading a year-end or early-2026 rally, powered less by surprise and more by a long-awaited normalization of one of Europe’s most cyclically misunderstood tech stories.

With the stock still trading at just 7x 2026 EBITDA, sentiment seems to have priced in too much gloom for a company that tends to rebound sharply when the cycle turns.

Zumtobel (ZAG Austria): efficiency gains light the way, but the cycle still casts a shadow

Zumtobel’s latest quarter saw revenues slipping slightly, but margins expanded sharply as the company’s lighting division benefited from lower material and personnel costs, along with a timely research subsidy.

Adjusted EBIT jumped nearly 20% year-on-year, pushing profitability back toward pre-slowdown levels. The group’s ongoing efficiency program, launched earlier this year, is starting to deliver tangible results, targeting up to €50 million in annual savings by 2029, most of it from streamlining SG&A. Phase two, focused on operations and procurement, should further ease cost pressure and stabilize cash generation. For a company long buffeted by raw material inflation and weak non-residential construction demand, this quarter was a reminder that Zumtobel can still extract value from self-help measures even when the top line stagnates.

Yet, for all the progress on costs, the revenue picture remains cloudy. The lighting segment’s margin improvement was achieved against a 5% sales decline, and there’s still little sign of a real demand inflection. The European commercial building cycle (Zumtobel’s main exposure) continues to drag, leaving order visibility thin and price competition fierce.

Management reaffirmed its full-year guidance of slightly lower sales and an EBIT margin between 1% and 4%, implicitly signaling that the company remains in “margin defense” mode rather than gearing up for growth. Structural headwinds persist: sluggish retrofit demand, delayed projects, and the absence of large public-sector lighting tenders are all keeping utilization rates suboptimal. Without a rebound in new construction or a stronger retrofit cycle driven by energy-efficiency upgrades, top-line growth will remain elusive despite all the internal tightening.

Still, there’s a silver lining. Zumtobel’s financial discipline and balance sheet strength position it well to ride out the downturn and capture operating leverage once the building cycle eventually turns. The company has proven it can protect profitability even as volumes fall, a hard-earned shift from earlier, more volatile years. With free cash flow improving and efficiency savings ramping up, the group is quietly building a foundation for future resilience.

But for now, the stock remains a value recovery story waiting for a cyclical trigger. Until demand for architectural and industrial lighting turns a corner, Zumtobel’s focus will remain inward.

Quadient (QDT France): digital tailwinds gather pace as legacy mail fades more gently

Quadient’s third quarter was a familiar mix of slow erosion in its legacy mail business and solid double-digit progress in its digital and locker divisions.

Revenue came in slightly below expectations at €248 million, held back by another near-10% drop in mail-related equipment sales and a weaker dollar, but the composition of growth continues to shift in the right direction. Digital solutions (now roughly a quarter of the group) posted organic growth above 9%, driven by subscription renewals and higher recurring software revenue, while parcel lockers grew 6%, bringing the installed base past 27,000 units. Both divisions are showing the kind of visibility and margin expansion that should begin to offset mail’s steady decline. The group reaffirmed its full-year targets despite FX headwinds, pointing to stable execution and good momentum heading into year-end.

What’s notable is how the business mix is quietly becoming more resilient. Digital’s growth rate is accelerating, boosted by cloud-based document automation, while locker revenue is increasingly subscription-driven, providing a more predictable recurring base. The recent acquisition of CDP Communications, a small but high-margin Canadian player in document accessibility software, fits neatly into this strategy, plugging into the digital platform with immediate accretion to margins.

Meanwhile, management’s 2026 targets remain intact: mid-single-digit organic growth and operating margins above 13%, underpinned by cost control and a recovery in U.S. postal renewals. The focus now is on maintaining momentum in Digital and Lockers while managing the long fade of physical mail, where profitability is still respectable at over 25% and provides cash to fund the transition.

The market seems to be overlooking this evolution. With the shares trading at barely 5x 2026 EBITDA, a steep 30% discount to historical levels, the stock screens like a value trap but behaves increasingly like a self-help story. The continued accumulation by VESA (now over 26%) adds another layer of interest, suggesting longer-term confidence in the group’s repositioning.

Execution risk remains, particularly if the mail decline reaccelerates or locker adoption slows, but the inflection toward software and services is real. Quadient is not transforming overnight, but the company is gradually turning a shrinking postal legacy into a growing digital infrastructure business.

Airbus Group (AIR France): some turbulence in deliveries

Airbus’s latest update brought another small bout of turbulence, but little to suggest the flight path has changed. The group trimmed its 2025 delivery target to 790 aircraft from 820, citing a quality issue with a supplier of fuselage panels.

At first glance, it’s a setback in what was already a tight year-end schedule, but the financial guidance was left untouched; EBIT and free cash flow targets are intact, implying that the operational hiccup is manageable. In practice, Airbus seems to be absorbing the impact through slower hiring, better cost control, and perhaps a touch of prudence on R&D timing. The company reassured that the issue is isolated to a single supplier batch, with dual sourcing in place and most aircraft needing only light rework. Deliveries should therefore catch up early in 2026, a familiar rhythm for an industry where December crunches have become routine.

The bigger story remains one of steady industrial normalization. Supply chains are finally healing, particularly around engines and cabin components, allowing Airbus to focus again on its multi-year ramp-up plan rather than firefighting. The A320neo family continues to anchor margins, while widebody programs like the A350 are quietly improving profitability as utilization picks up across long-haul routes. Cash generation remains the key differentiator: the company expects roughly €4.5 billion in free cash flow this year, a figure that underlines just how much internal efficiency has improved even amid lingering bottlenecks. While the A321XLR certification and production cadence still depend on regulatory timing, management’s confidence in medium-term growth signals that the structural ramp to 75 narrowbody aircraft per month is back on track.

The near-term narrative may revolve around execution noise, but strategically, Airbus sits in the sweet spot of a multi-year aviation upcycle. Airline demand remains robust, with order books stretching well beyond the decade, and pricing discipline is holding even as suppliers regain footing. The recent panel issue is more of a procedural stumble than a strategic threat, and the company’s ability to hold its earnings guidance despite lower deliveries speaks volumes about underlying resilience.

The setup is straightforward: Airbus remains one of Europe’s clearest compounders in industrials, with a cleaner balance sheet, compounding free cash flow, and an improving operational backbone that makes short-term disruptions feel increasingly like white noise on a long-haul flight.

Bilfinger (GBF Germany): operational discipline meets growth ambition

Bilfinger’s Capital Markets Day in Frankfurt outlined a company no longer trying to prove its recovery, but instead defining what a mature, steadily compounding version of itself should look like.

The new 2030 plan targets annual revenue growth of 8–10%, an EBITA margin of 8–9%, and cash conversion above 90%; figures that might once have seemed aspirational, but now rest on solid operational progress. The strategy leans on two familiar levers: operational excellence and market expansion. The first is about pushing further on what’s already working — standardising processes, tightening contract discipline, and digitising workflows to squeeze another 1–2 points of margin improvement out of the base business. The second broadens the playing field, focusing on deeper penetration of core European regions while scaling up the US and Middle East operations where industrial outsourcing demand is rising fastest.

There’s a clear sense that Bilfinger is finally turning its structural strengths into durable advantages. The mix of recurring maintenance contracts, exposure to energy transition infrastructure, and the integration of AI-driven process monitoring make the company less cyclical than the “old Bilfinger” many still remember. The group is now increasingly talking like a platform — one that can bolt on local acquisitions and fold them efficiently into a standardised operating model. M&A remains a lever, but not the central story: management’s tone on capital allocation was measured, promising 40–60% of net income returned to shareholders via dividends, with organic reinvestment and disciplined dealmaking as the priority.

A new reporting structure, grouping the business into Western Europe, Central Europe, and International, will bring more transparency to profitability by region, a small but meaningful governance upgrade for investors tracking where the growth is actually coming from.

In many ways, Bilfinger’s reinvention mirrors the industrial clients it serves: leaner, digitally enabled, and better capitalised after years of restructuring. The company isn’t promising fireworks; steady organic growth, high cash conversion, and a tightening valuation gap with peers like Spie already make the story compelling.

With the current buyback adding a modest yield on top of an improving margin trajectory, Bilfinger now looks like a business entering its next phase with realistic ambition and operational confidence.

If you appreciate this post, feel free to share and subscribe below!